Property Investment Tax Benefits Explained

- Sarah Porter

- Oct 15, 2025

- 16 min read

Updated: Oct 16, 2025

When people talk about investing in rental properties, the conversation often centers on monthly rent checks and long-term appreciation. But there's a third, equally powerful element that often gets overlooked: tax benefits. These are essentially government-approved strategies and deductions that can seriously lower your taxable income.

The big players here are deducting everyday expenses like mortgage interest and property taxes, but the real game-changer is depreciation—a non-cash deduction that accounts for the wear and tear on your property. Tapping into these benefits puts more money back in your pocket each year, directly boosting your cash flow and helping you build wealth faster.

Why Tax Benefits Are a Cornerstone of Real Estate Investing

Let's pull back the curtain on what really drives wealth in real estate. It's not just about collecting rent. The tax code itself can become your silent business partner, supercharging your returns in ways that many new investors miss completely.

Think of your rental property as a small business. Just like any other business, the IRS lets you write off the legitimate costs of keeping it up and running. This guide is all about cutting through the jargon and giving you a clear, practical roadmap to do just that.

Your Path to Tax-Efficient Investing

We're going to walk through the core concepts that every savvy investor needs to know. We’ll build your understanding one step at a time, covering the essentials:

Depreciation: You'll learn how this powerful "paper loss" can shrink your tax bill even when your bank account is growing.

Deductible Expenses: We’ll show you how to turn ordinary costs—from a simple repair to your annual insurance premium—into valuable tax savings.

Capital Gains Management: Selling a property can trigger a big tax event. We'll explore smart ways to defer or even minimize those taxes.

Advanced Strategies: Ready to level up? We'll introduce more complex tactics like cost segregation and what it takes to achieve Real Estate Professional Status.

Consider this your playbook for making the tax code work for you, not against you. The goal is to leave you with real, actionable steps to make your investments more efficient.

Of course, before you can optimize your taxes, you need a solid grasp of your income. A great starting point is understanding what cash flow is in real estate and how it works. Once you master these principles together, you'll be well on your way to building lasting wealth.

How Depreciation Slashes Your Taxable Income

Of all the tax breaks available to property investors, depreciation is easily the most powerful—and often the most misunderstood.

Think about it this way: the IRS lets you deduct an annual expense for the wear and tear on your building, even while your property is likely gaining value in the market. This is the magic of depreciation. It’s a "paper loss" that lowers your taxable income without you actually having to spend a dime.

This non-cash deduction is a direct boost to your bottom line. By reducing your taxable income on paper, you owe less in taxes each year, which means more real cash stays in your pocket. Getting a handle on how to calculate and claim it is fundamental to smart real estate investing.

The Core Idea Behind Depreciation

At its heart, depreciation is simply the process of spreading out a property's cost over its lifespan. The tax code recognizes that buildings, roofs, HVAC systems, and appliances don’t last forever. So, it allows you to write off a slice of their value each year to account for this gradual decline.

Here’s the most important rule to remember: land does not depreciate. When you buy a property, you're buying the land and the building sitting on it. For tax purposes, you have to split the value between the two, because only the building's value is eligible for this deduction.

Calculating Your Annual Depreciation Deduction

Once you have the right numbers, the math is actually pretty simple. The IRS defines the "useful life" for residential rental properties at 27.5 years. To figure out your annual deduction, you just divide the building's value by that number.

Let's walk through a quick example to make it crystal clear.

Step 1: Purchase Price: You buy a single-family rental for $500,000.

Step 2: Separate Land and Building Value: A common split, often found on your tax assessment or an appraisal, is 20% for the land and 80% for the building. * Land Value: $500,000 x 20% = $100,000 (This part can't be depreciated) * Building Value (Your Depreciable Basis): $500,000 x 80% = $400,000

Step 3: Calculate the Annual Deduction: Divide the building's value by its IRS-mandated useful life. * $400,000 / 27.5 years = $14,545 per year

This $14,545 annual deduction is a game-changer. If your property generated $20,000 in net rental income for the year, you’d only pay taxes on $5,455 of it ($20,000 - $14,545). That's a massive tax saving.

To help you see how this works, here’s a quick table breaking down the calculation from our example.

Sample Annual Depreciation Deduction Calculation

This table illustrates how to calculate the annual depreciation deduction for a typical residential rental property in the US.

Metric | Value | Explanation |

|---|---|---|

Total Purchase Price | $500,000 | The total amount paid for the property. |

Land Value (20%) | $100,000 | The non-depreciable portion of the purchase price. |

Building Value (80%) | $400,000 | This is your depreciable basis. |

Useful Life (IRS) | 27.5 years | The standard recovery period for residential rentals. |

Annual Deduction | $14,545 | The amount you can deduct each year ($400,000 / 27.5). |

As you can see, a few straightforward steps turn a large asset purchase into a significant, ongoing tax deduction that improves your cash flow every single year.

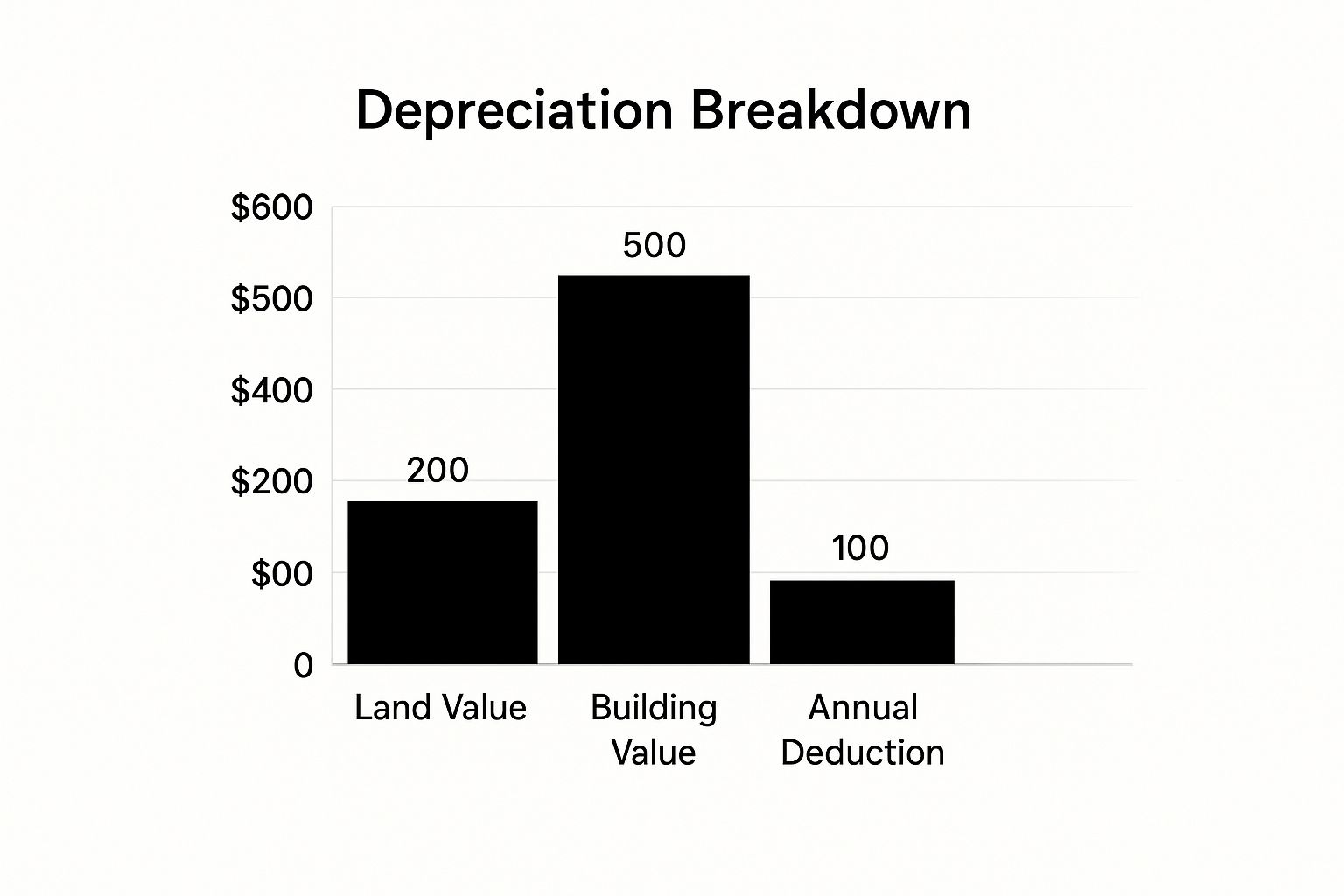

This simple chart visualizes the breakdown of the property's value and how it leads to that powerful annual deduction.

The graphic really drives home the point: the bulk of your property's value (the building) becomes a powerful engine for generating tax savings year after year.

A Globally Recognized Investment Benefit

This isn't just a U.S. perk; depreciation is one of the most common tax benefits for property investors all over the world. Whether you own real estate in the United States, Australia, or the UK, tax laws generally let you deduct the building's value over its useful life, which can be anywhere from 27.5 to 40 years.

For example, the IRS sets the schedule at 27.5 years for residential properties and 39 years for commercial buildings, giving investors a consistent way to lower their tax bill without spending any extra cash. You can find more great information about real estate investing on incompassfp.com.

Turning Rental Expenses into Tax Deductions

While depreciation is a fantastic non-cash deduction, let's not forget about the real money you spend every day to run your rental property. Every dollar you spend keeping your property operating and in good shape is a potential tax write-off.

Think of your rental property as a small business. The costs of doing business—from mortgage interest to marketing a vacant unit—chip away at your taxable income. This is a core principle for smart investors: you only want to pay tax on your actual profit, not your gross rent.

Meticulous record-keeping isn't just good practice; it's one of the most fundamental habits that separates successful investors from the rest.

The Most Common and Powerful Deductions

Nearly every cent you spend on your investment property can likely be deducted. These aren't sneaky loopholes; they're standard business expenses recognized by the IRS.

Here are the heavy hitters you absolutely need to be tracking:

Mortgage Interest: This is almost always the single biggest deduction for landlords. The interest portion of your monthly payment is fully deductible, which adds up to massive savings each year.

Property Taxes: Those annual state and local property tax bills are fully deductible against your rental income.

Insurance Premiums: Your landlord insurance policy—including coverage for hazards, fire, and liability—is a necessary cost of doing business, and therefore, it's deductible.

Utilities: If you cover any utility bills for your tenants, like water, trash, or gas, you can write off those costs.

These "big four" are just the beginning.

Operational and Professional Service Costs

Beyond the foundational expenses, a whole host of other operational costs are also on the table. These are the fees and services that keep your rental running smoothly and professionally.

A few key examples include:

Property Management Fees: Hire a pro to manage your property? Their fees are 100% deductible.

Legal and Professional Fees: The money you pay to your lawyer for a lease review or your accountant for tax prep is a deductible expense.

Advertising Costs: Whether you're running a Facebook ad or a listing on Zillow, the cost to find a new tenant is a write-off.

Key Takeaway: The IRS has a simple rule of thumb. If an expense is both "ordinary and necessary" for running your rental business, it's almost always deductible. Keep that phrase in mind as you spend money throughout the year.

The Crucial Difference Between Repairs and Improvements

Now for one of the most critical distinctions in rental property taxes: the difference between a repair and an improvement. Getting this wrong is a common and costly mistake, as the IRS treats them very differently.

A repair is something that keeps your property in good working order. Think of it as maintenance—fixing what's already there. Repairs are great because you can deduct the full cost in the year you pay for them.

An improvement, on the other hand, is an expense that adds substantial value, extends the property's life, or adapts it for a new use. You can't deduct these costs immediately. Instead, they must be capitalized and depreciated over 27.5 years, just like the property itself.

Here's a simple way to look at it:

Type of Work | Classification | Tax Treatment |

|---|---|---|

Fixing a leaky pipe under the sink | Repair | Deduct the full cost this year |

Replacing all the old plumbing in the house | Improvement | Depreciate the cost over 27.5 years |

Replacing a single broken window pane | Repair | Deduct the full cost this year |

Installing all new, energy-efficient windows | Improvement | Depreciate the cost over 27.5 years |

Getting this right is non-negotiable for accurate tax filing. For a much deeper look into managing these costs effectively, check out our guide on mastering rental property maintenance costs.

This powerful principle—deducting your operational costs—is a cornerstone of real estate investing. If you own a property in New York that brings in $50,000 in rent but costs $30,000 to run, you're only taxed on the $20,000 difference. It's so vital that a 2025 Deloitte survey found 14% of global real estate executives see tax benefits as a top reason to increase their investments. You can find more of their insights into commercial real estate trends on deloitte.com.

Managing Capital Gains Tax When You Sell

Your tax strategy doesn’t just end with yearly deductions. The biggest tax event of your investment journey often happens on the very last day—the day you sell. This is when capital gains tax enters the picture, and it’s a big one. It's the tax you owe on the profit you’ve made from the sale.

Figuring out how to handle this tax is absolutely crucial for maximizing your total return. A smart exit strategy can literally save you tens of thousands of dollars, making sure the wealth you’ve built over the years doesn't get whittled away by an unnecessarily large tax bill.

Thankfully, the tax code gives savvy investors some powerful tools to shrink or even postpone this liability. The secret is knowing your options and planning your exit long before you even think about listing the property.

Short-Term vs. Long-Term Capital Gains

First things first, you need to understand the critical difference between short-term and long-term capital gains. How long you’ve owned the property directly impacts the tax rate on your profit, and the difference is night and day.

Short-Term Capital Gains: This applies if you sell a property you've held for one year or less. Any profit is taxed at your ordinary income rate, which could be as high as 37%. It’s the same steep rate you pay on your regular paycheck.

Long-Term Capital Gains: This is the goal. If you sell a property you’ve owned for more than one year, your profit gets taxed at much friendlier rates—typically 0%, 15%, or 20%, depending on your income bracket.

This isn’t a minor detail; it’s a massive one. Holding a property for just one extra day past the one-year mark can dramatically slash your tax bill on the exact same profit. It’s one of the most fundamental property investment tax benefits you can get.

Think about it: For a high-income investor, selling a property with a $100,000 profit after 11 months could mean a tax bill of up to $37,000. By waiting just over a month longer, that bill could drop to $20,000 or even $15,000. That's the power of patience.

Deferring Taxes with a 1031 Exchange

So, what if you want to sell your property and reinvest in another, but you don't want to pay any capital gains tax right now? For experienced investors, the 1031 Exchange is the ultimate tool. This incredible provision in the tax code lets you postpone paying capital gains tax, potentially forever.

Imagine you’re trading up cars. Instead of selling your old car, pocketing the cash (and paying taxes on it), and then buying a new one, a 1031 Exchange lets you roll the entire value of your old property directly into a new one.

As long as you play by the rules, you pay zero capital gains tax at the time of the swap. You're simply "deferring" the tax, which only comes due when you finally cash out and sell a property for good down the road.

How a 1031 Exchange Works

Be warned: this process is tightly regulated and demands precision. To pull off a successful 1031 Exchange, you have to follow a few non-negotiable rules:

Like-Kind Property: You must exchange your property for another "like-kind" property. The good news for real estate investors is that this rule is incredibly flexible. You can swap a single-family rental for an apartment building, a piece of raw land, or even a commercial storefront.

Strict Timelines: You have exactly 45 days from the day you sell your property to officially identify potential replacement properties. This deadline is firm.

Closing Deadline: You must close on the purchase of your new property within 180 days of selling the original one.

Equal or Greater Value: To defer all of your tax, the new property's value must be equal to or greater than the one you sold. You also need to reinvest all the cash proceeds from the sale.

This strategy isn't about dodging taxes—it’s about tax deferral. It lets you keep your capital working for you, growing your portfolio without getting hit with a tax bill every time you level up. This is exactly how many real estate moguls build incredible wealth, by rolling one investment into the next, and then the next.

Advanced Tax Strategies for Serious Investors

Once you’ve got a solid handle on the basics like depreciation and writing off expenses, you can step up to a whole new level of tax savings. These next-level strategies are for investors who are serious about optimizing their portfolio and using real estate as a powerful tool to build wealth.

These aren't your typical, run-of-the-mill deductions. They demand careful planning, a deeper commitment, and usually the guidance of a good CPA. But if you’re willing to go the extra mile, the payoff can be huge, turning your rental portfolio into a finely-tuned, tax-saving machine.

Unlocking Unlimited Deductions with Real Estate Professional Status

To the IRS, most rental income is considered "passive." This creates a frustrating problem for many investors: if your property shows a loss on paper (which often happens thanks to depreciation), you can only use that loss to offset other passive income. You can't use it to reduce the taxes on your day job's salary.

But there’s a way to break through that barrier: achieving Real Estate Professional Status (REPS). Earning this designation completely changes how the IRS views your rental activities, shifting them from passive to active.

The Game-Changing Benefit: With REPS, the cap on your rental losses disappears. You can deduct an unlimited amount of these paper losses directly against your active income—like your W-2 salary—which can slash your tax bill by thousands.

Getting this status isn't easy, though. You have to meet two strict tests:

The 750-Hour Test: You must spend more than 750 hours a year working in real estate trades or businesses.

The More-Than-Half Test: The time you spend on real estate has to be more than half of the total time you spend working at all your jobs.

This is a perfect fit for full-time real estate agents, developers, or property managers. It's also a great strategy for a high-income household where one spouse can dedicate their time to meeting the REPS requirements and managing the portfolio.

Supercharging Depreciation with Cost Segregation

We've already talked about how standard depreciation lets you write off a building's value over 27.5 years. Think of a cost segregation study as depreciation on steroids. It's a highly detailed engineering analysis that dissects your property into all its different parts and re-categorizes them for much faster tax write-offs.

Instead of seeing the property as one big chunk depreciating slowly, a cost segregation study identifies all the components that wear out much faster.

Carpet and flooring: Depreciated over 5 years.

Appliances and cabinetry: Depreciated over 5 years.

Fences and landscaping: Depreciated over 15 years.

The building structure itself: Stays on the 27.5-year schedule.

By accelerating the depreciation for these shorter-lived assets, you can generate enormous deductions in the first few years of ownership. This front-loads your tax savings, giving you a major cash flow boost when you need it most. It's easily one of the most powerful tax benefits for rental property investors who are actively acquiring new properties.

The Qualified Business Income Deduction

Another fantastic tool in the investor's tax kit is the Qualified Business Income (QBI) deduction, also known as the Section 199A deduction. It allows owners of certain businesses—which can include a rental real estate operation—to deduct up to 20% of their qualified business income.

To get this deduction, your rental activities need to be significant enough to be considered a "trade or business." The IRS rules can get complicated, but there's a helpful safe harbor: you can generally qualify if you spend at least 250 hours per year on your rental business. This includes time spent by you, your employees, and even your contractors, so keep meticulous records.

For landlords with a few properties, hitting this threshold is often very achievable, making the QBI a substantial tax break that directly reduces the income you pay taxes on.

The journey from a casual landlord to a savvy investor involves mastering both foundational and advanced tax strategies. The table below helps clarify who these different approaches are for and what they entail.

Comparing Standard vs. Advanced Tax Strategies

Strategy | Primary Benefit | Who It's For | Key Requirement |

|---|---|---|---|

Standard Depreciation | Reduces taxable income by writing off the property's value over time. | All rental property owners. | Owning a residential rental property placed in service. |

Expense Deductions | Lowers net rental income by subtracting all ordinary and necessary costs. | All rental property owners. | Meticulous tracking and documentation of all expenses. |

Real Estate Pro Status | Allows for unlimited rental loss deductions against any type of income. | Full-time real estate pros or investors dedicating significant time. | Passing the IRS's 750-hour and "more-than-half" time tests. |

Cost Segregation | Massively accelerates depreciation deductions into the early years of ownership. | Investors buying larger properties or commercial real estate. | Commissioning a formal engineering-based study. |

Ultimately, choosing the right strategy depends on your portfolio size, income level, and how much time you can dedicate to your real estate activities. While standard deductions are the bedrock of any investor's tax plan, embracing advanced strategies is what truly separates the serious players and accelerates wealth creation.

Your Action Plan for Tax-Efficient Investing

Knowing about these tax breaks is one thing, but actually using them to your advantage is where the real work—and the real reward—lies. Let's build a game plan to make sure you're capturing every last dollar you're entitled to. This isn't just about a smaller tax bill in April; it's about fundamentally building long-term wealth through your properties.

The bedrock of any solid tax strategy is simple but non-negotiable: meticulous record-keeping. Without it, the most powerful deductions simply vanish. Every receipt, every bank statement, every invoice is a piece of evidence that justifies the savings you claim.

Creating Your Documentation System

First things first, you need a system to track everything. It doesn't need to be fancy, but it absolutely must be consistent. Whether you prefer dedicated software, a detailed spreadsheet, or even just a set of clearly labeled folders, the mission is the same: make tax time a simple exercise in reporting, not a mad scramble for lost paperwork.

For a more detailed look, our guide on the importance of meticulous record-keeping for landlords walks you through setting up a bulletproof system.

At a minimum, your documentation checklist needs to cover:

All Income Received: Keep a running log of every rent payment, late fee, and even security deposits collected.

Every Single Expense: From the annual mortgage interest statement down to a $5 box of screws for a quick fix, no expense is too small to track. It all adds up.

Clear Repair vs. Improvement Notes: When you spend money on the property, make a quick note: Was this to maintain it (a repair) or to upgrade it (an improvement)? That distinction is crucial for how you file your taxes.

The real shift happens when you stop thinking like someone who just owns a property and start acting like someone running a tax-efficient business. A proactive approach turns tax season from a dreaded chore into a powerful strategic advantage.

Partner with a Professional

Finally, the single most important step you can take is to get a qualified tax professional on your team—specifically, one who knows real estate inside and out. They are your most valuable player. A great CPA doesn’t just file your return; they help you strategize throughout the year, spot opportunities you’d otherwise miss, and keep you safely on the right side of the IRS.

By combining your own diligent record-keeping with expert guidance, you'll be in the perfect position to optimize your portfolio and make sure your investments are truly working for you.

Frequently Asked Questions

It's completely normal to have questions when you're digging into the tax side of property investing. Let's clear up a few of the most common points that trip up investors, so you can move forward with confidence.

Can I Deduct My Mortgage Principal Payments?

The short answer is no. You can't deduct the principal portion of your mortgage payment. The IRS views this as you simply paying off a loan to build your own equity—it's not considered an operating expense.

But here's the good news: the interest you pay on that loan is a different beast entirely. Every single dollar of mortgage interest is 100% deductible, and for most investors, it’s one of the biggest and most powerful write-offs available each year.

What Is the Difference Between a Repair and an Improvement?

This is a crucial distinction, and one the IRS pays close attention to. Getting it wrong can lead to headaches down the road.

A repair is something you do to keep the property in its current good condition. Think of things like fixing a running toilet, patching a small hole in the drywall, or replacing a broken window pane. These are necessary maintenance tasks, and you can deduct the full cost in the same year you pay for them.

An improvement, however, is a major upgrade that adds significant value, extends the property's life, or adapts it for a new use. We're talking about big-ticket items like a full kitchen remodel, adding a new bathroom, or putting on an entirely new roof. You don't deduct these costs all at once. Instead, they are "capitalized" and depreciated over 27.5 years, just like the property itself.

Here’s a simple way to think about it: A repair is like getting an oil change for your car to keep it running well (a current expense). An improvement is like dropping in a brand-new engine to make it last another decade (a capitalized cost).

Do I Have to Pay Back My Depreciation Deductions When I Sell?

Yes, you do—in a sense. This is called depreciation recapture, and it's a critical concept to grasp before you ever think about selling.

When you sell your rental for a profit, the IRS essentially says, "Hey, for all those years you took depreciation deductions, we want that money back." They "recapture" the total amount of depreciation you claimed over the time you owned the property.

The recaptured amount is then taxed, but not at the favorable long-term capital gains rate. Instead, it's hit with a special, higher tax rate, capped at a maximum of 25%. This is exactly why savvy investors often use a 1031 Exchange. It’s a powerful strategy that lets you defer both the capital gains tax and the depreciation recapture tax, allowing you to roll your entire profit into a new investment.

At Keshman Property Management, we handle the complexities of ownership so you can focus on the rewards. With over 20 years of experience, we treat your property with the same care and strategic insight as our own. Discover our transparent, owner-focused approach at https://mypropertymanaged.com.

Comments