What Is Cash Flow in Real Estate and How It Works

- Sarah Porter

- Oct 10, 2025

- 13 min read

When you peel back all the layers of real estate investing, one metric stands out as the true measure of an asset's health: cash flow.

In the simplest terms, real estate cash flow is the profit you have left over each month after you’ve collected the rent and paid all the bills. It’s the money that actually lands in your bank account—the financial heartbeat of your investment. This single number tells you whether you own a profitable asset or a costly liability.

What Is Real Estate Cash Flow Really

Think of your rental property as a small business. The rent you collect is your total revenue. From that income, you have to subtract all the costs of keeping the lights on—things like your mortgage payment, property taxes, insurance, and any maintenance that pops up.

What's left over? That's your cash flow. If it’s a positive number, congratulations, your property is putting money in your pocket. If it’s negative, you’re on the hook to cover the difference yourself.

The Heartbeat of Your Investment

It's easy to get caught up in the excitement of appreciation, the idea that your property's value will climb over time. But cash flow is what pays the bills today. It’s the immediate, tangible return that gives you the financial stability to hold onto an asset long enough to see that appreciation happen.

Cash flow is the net amount of money generated by a property after all operating expenses and debt service are paid. This is critical because it represents the real profit a property owner can use or reinvest.

Don't just take my word for it. Research shows that income from rent is the primary driver of returns. In fact, Deloitte’s global outlook highlights that historically, about 78% of long-term returns in commercial real estate came from rental income, not just value increases. This really drives home why understanding cash flow is non-negotiable for building sustainable wealth.

Cash Flow vs Other Metrics

New investors often get cash flow mixed up with other financial metrics, but they aren't the same. Your profit on paper, for example, might include non-cash deductions like depreciation for tax purposes. Cash flow, on the other hand, is all about the actual money you can spend.

It gives you a clear, real-world picture of your property's performance, cutting through the more abstract accounting measures. Nailing this distinction is just as fundamental as understanding other core concepts, like capitalization rates. If you want to go a step further, you can explore our complete guide on what is cap rate in real estate investing.

Understanding the Cash Flow Equation

To really get a feel for what cash flow is in real estate, you have to look at both sides of the financial coin: the money flowing in and the money flowing out. The basic math is simple, but truly understanding each part of the equation is what separates a successful investor from one who’s just getting by.

Think of it this way: first, you figure out your property's total potential earnings. This is more than just rent—it’s every dollar the property could possibly bring in. Then, you subtract all the realistic costs of keeping the place running.

The Income Side of the Equation

We start with your Gross Potential Income (GPI). This is a best-case-scenario number. It’s what your property would earn in a year if it was 100% occupied and every single tenant paid their rent on time. While rent is the biggest piece of the puzzle, smart investors know there are other ways to boost income.

These extra revenue streams can seriously pad your bottom line. Common examples include:

Pet Fees: A one-time deposit or a monthly "pet rent."

Parking Charges: Renting out assigned spots is a no-brainer, especially in dense urban areas.

Laundry Facilities: Coin-operated washers and dryers in a multifamily building can be a small but steady source of income.

Storage Units: If you have extra space in a basement or garage, you can rent it out.

But let’s be realistic—no property is full all the time. You have to account for vacancy (empty units) and credit loss (tenants who don't pay). When you subtract these anticipated losses from your GPI, you get your Effective Gross Income (EGI). This is a much more honest and practical number to work with.

The Expense Side of the Equation

Once you have a realistic income figure, it’s time to subtract your Operating Expenses. These are all the costs required to keep the property in good shape and generating revenue. We'll leave the mortgage payment out of it for just a moment.

Net Operating Income (NOI) is your property's income before you factor in loan payments and income taxes. It’s a pure measure of the property's profitability, which makes it a fantastic tool for comparing one investment opportunity against another.

Operating expenses are the nuts and bolts of running an investment property. If you want to go deeper, you can learn more about how to calculate operating expenses for your business in our other guide. Generally, they fall into two buckets:

Fixed Expenses: These are the costs you can count on, month after month, regardless of whether you have tenants. Think property taxes, insurance premiums, and maybe some HOA fees. They're predictable and easy to budget for.

Variable Expenses: These are the costs that can change based on usage, season, or just plain bad luck. This category includes utilities (if you're responsible for them), maintenance, repairs, property management fees, and those big-ticket capital expenditures like a new roof or an HVAC system.

Since variable costs are inherently unpredictable, you absolutely must build a buffer. A good rule of thumb is to set aside 5-10% of your gross rent for routine repairs and another 5-10% for major capital expenditures.

After you subtract all of these operating expenses from your EGI, you're left with your Net Operating Income (NOI). This number is the last crucial step before you can calculate your final cash flow.

How to Calculate Cash Flow for Any Property

Knowing the theory is one thing, but running the numbers yourself is how you build real confidence as an investor. Calculating cash flow isn’t some high-level financial sorcery; it’s just simple arithmetic that anyone can master.

Let's walk through a real-world example to see how it works. Imagine you're looking at a single-family home that you could rent out for $2,000 per month. This is our starting line. From here, we'll peel back the layers of expenses, one by one, to get to the number that really matters.

Step 1: Start With Total Potential Income

First things first, figure out the Gross Potential Income (GPI). This is the absolute maximum rent you could collect in a year if the property was rented out every single day.

Monthly Rent: $2,000

Annual GPI: $2,000 x 12 months = $24,000

Now for a reality check: no property is occupied 100% of the time. You need to account for vacancies. A standard rule of thumb is to budget for a 5% vacancy rate. Subtracting this gives us the Effective Gross Income (EGI).

Vacancy Loss: $24,000 x 5% = $1,200

EGI: $24,000 - $1,200 = $22,800

This EGI of $22,800 is a far more realistic number to work with, as it already anticipates the inevitable gaps between tenants.

Step 2: Subtract All Operating Expenses

Next up, we subtract all the costs of keeping the property up and running—everything except the mortgage. These are your Operating Expenses. Let’s plug in some common annual estimates:

Property Taxes: $3,000

Homeowners Insurance: $1,200

Repairs & Maintenance (5% of EGI): $1,140

Capital Expenditures (5% of EGI): $1,140

Property Management (8% of EGI): $1,824

When you add those up, your total operating expenses come to $8,304. Subtract this from your EGI to find the Net Operating Income (NOI), a crucial metric that shows how profitable the property is before the mortgage is paid.

NOI: $22,800 (EGI) - $8,304 (Expenses) = $14,496

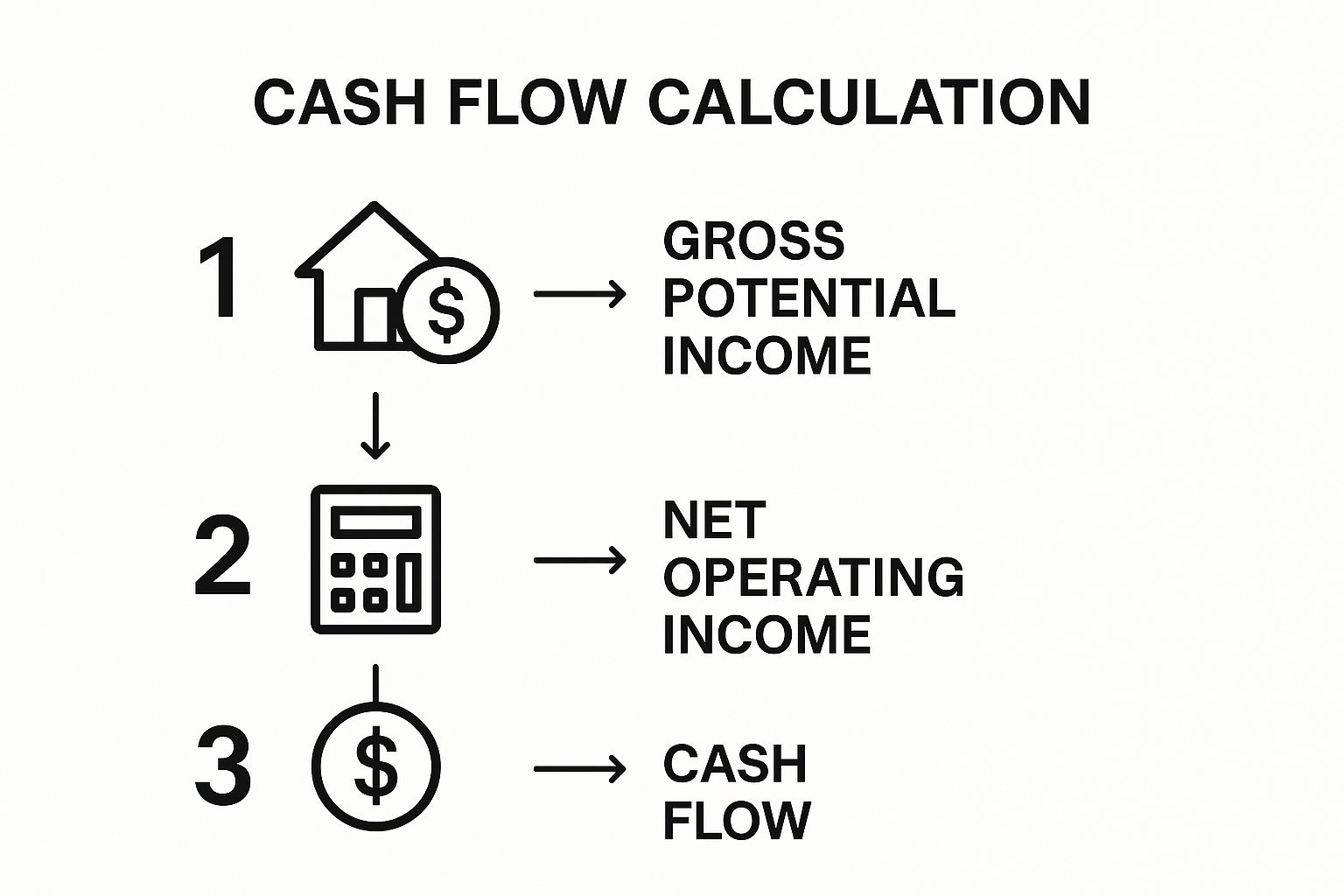

The infographic below breaks down this simple, three-step process for figuring out cash flow.

As you can see, the process flows from the biggest income number down to the final profit after every single cost is accounted for.

To make this even clearer, here’s a table that lays out the entire calculation from top to bottom.

Sample Cash Flow Calculation for a Rental Property

Calculation Step | Description | Example Amount |

|---|---|---|

Gross Potential Income | Total possible annual rent ($2,000 x 12) | $24,000 |

Less: Vacancy Loss | Estimated income lost from empty units (5%) | -$1,200 |

Effective Gross Income (EGI) | Realistic annual income after vacancies | $22,800 |

Less: Operating Expenses | All costs to run the property (taxes, insurance, etc.) | -$8,304 |

Net Operating Income (NOI) | Profit before paying the mortgage | $14,496 |

Less: Debt Service | Total annual mortgage payments ($1,000 x 12) | -$12,000 |

Final Cash Flow (Annual) | The money left in your pocket each year | $2,496 |

This step-by-step breakdown gives you a clear picture of how money flows through a rental property, from gross rents all the way to net profit.

Step 3: Deduct Your Debt Service

The last piece of the puzzle is subtracting your annual debt service—the total amount of principal and interest you pay on your mortgage each year. Let’s assume your monthly mortgage payment is $1,000.

Annual Debt Service: $1,000 x 12 = $12,000

And now, for the moment of truth. We subtract that debt service from your NOI.

Cash Flow = Net Operating Income - Debt Service$14,496 (NOI) - $12,000 (Debt) = $2,496 Annual Cash Flow

That means this property puts an extra $208 in your pocket every single month. This final number is the clearest measure of how a property is truly performing.

Running these numbers quickly and accurately is key, and using a dedicated rental property ROI calculator can help you maximize your investments. Once you have this process down, you have a reliable toolkit to analyze any deal that comes your way.

Why Cash Flow Trumps Appreciation

It’s easy for new investors to get starstruck by appreciation. The dream is to buy a property, sit back, and watch its value climb into the stratosphere. And while appreciation is a wonderful perk, any investor who’s been around the block will tell you the same thing: cash flow is king.

Relying on appreciation is just speculation. You're essentially betting on future market trends that you have absolutely no control over. Positive cash flow, on the other hand, is the steady, predictable heartbeat of your investment. It’s the real money that hits your bank account every month, giving you the stability to hold onto the asset for the long haul.

The Power of Predictable Income

When a property generates consistent positive cash flow, it pays for itself. The rent covers the mortgage, taxes, insurance, and maintenance, and there's still money left over for you. This monthly profit is your financial cushion.

Think about it. What happens when a water heater bursts or a tenant moves out unexpectedly? Without that cash flow buffer, you’re digging into your own pocket, and your "investment" suddenly becomes a liability. More importantly, cash flow helps you ride out economic downturns. When the market slumps, investors chasing appreciation are often forced to sell at a loss. But if your property is cash-flowing, you can simply hold on, keep collecting rent, and wait for the market to bounce back.

Cash flow isn't just about profit; it's about resilience. It’s what transforms a real estate purchase from a speculative gamble into a sustainable, self-funding business that grows your wealth month after month.

Why Lenders Love Cash Flow

Banks and lenders see things the same way. When they're looking at a loan application, cash flow is their proof that the property is a sound investment capable of covering its own debt. A property with a solid track record of positive income is always a lower risk than one propped up by hopeful appreciation.

This isn't just a local mindset; it's a global one. Commercial real estate transactions in Europe, for instance, recently hit €188.8 billion—a 13.7% jump driven by investors hunting for stable, income-producing assets, not just flipping properties. This shows just how foundational cash flow is to the entire market. If you're interested, you can explore more about these global real estate trends and what they signal for investors.

At the end of the day, appreciation is the icing on the cake. Cash flow is the cake itself. It provides the stability, buffers the risk, and delivers the consistent returns that are the bedrock of any smart, long-term real estate strategy. Understanding what cash flow is in real estate and making it your top priority is the surest path to building wealth that lasts.

Practical Ways to Boost Your Cash Flow

So, you’ve got a handle on how to calculate your property’s cash flow. Great. Now for the fun part: making it grow.

Think of your rental property like a business with two main controls. One lever increases your income, and the other slashes your expenses. The real magic happens when you start working both of them at the same time.

Boosting your bottom line doesn't always mean you need to sink a ton of money into a massive renovation. Sometimes, the best results come from small, smart adjustments that either bring more money in or stop it from going out. Let's dig into some proven strategies that experienced landlords use to get more out of their investments.

Strategies for Increasing Your Income

The most obvious path to better cash flow is to get your property to generate more revenue. Raising the rent is the go-to move, of course, but there are plenty of other creative ways to fatten up your top line.

A classic strategy is making value-add upgrades. I'm not talking about a full-gut remodel. Small, targeted improvements can make a huge difference. Think about installing modern light fixtures, giving the walls a fresh coat of paint, or swapping out old appliances for stainless steel. These simple changes can easily justify a higher rent, often paying for themselves in no time.

But don’t stop at rent. Look at your property and ask yourself: is every square foot working for me? That unused garage, extra parking spot, or empty basement storage unit could be rented out separately for a nice little stream of extra cash each month.

You can also add amenities that tenants are more than happy to pay for:

In-unit laundry: A washer and dryer is one of the most requested features. It’s a convenience that can easily command a higher monthly rent.

Pet-friendly policies: Allowing pets opens up your property to a much larger pool of potential tenants. Charging a monthly "pet rent" of $25 to $50 per pet is standard practice and adds up quickly.

Smart home features: Things like a smart thermostat or keyless entry aren't just cool gadgets; they're modern perks that can help your property stand out and justify a premium price.

Smart Ways to Reduce Your Expenses

Now for the other side of the coin. Trimming your operating costs has the exact same impact as increasing your income—it leaves more money in your pocket at the end of the day. A smart investor is always looking for ways to run a leaner operation.

One of the single most powerful moves you can make is to refinance your mortgage. If interest rates have fallen since you first got your loan, refinancing could potentially shave hundreds of dollars off your monthly payment. This one action can give your real estate cash flow a massive, immediate boost.

Proactively managing expenses is just as crucial as maximizing income. A dollar saved is a dollar earned, and small, consistent savings compound over time to significantly boost your net profit.

Another fantastic tactic is to appeal your property taxes. Assessments aren't set in stone, and they aren’t always right. If you can make a successful case that your property is overvalued, you could lock in substantial savings year after year.

Finally, get serious about preventative maintenance. It is always, always cheaper to fix a small leak today than it is to deal with catastrophic water damage and mold remediation down the road. Regular check-ups on your HVAC system, roof, and plumbing will save you from those heart-stopping emergency repair bills that can demolish your profits for months.

Common Questions About Real Estate Cash Flow

Even after you’ve run the numbers a dozen times, the real world of property investing has a way of throwing curveballs. Understanding the nuances of what cash flow is in real estate isn't just about the formula; it's about knowing how to handle the questions that pop up on the ground.

Think of this as a quick Q&A session to clear up the practical issues you're bound to face. Getting these details right is what separates investors who just know the theory from those who actually build wealth. Let's dig into some of the most common questions.

Is Negative Cash Flow Always a Bad Thing in Real Estate?

For most people, yes. It’s a bright red flag. A property with negative cash flow means you're feeding it money from your own pocket every single month just to keep it. It's not an asset; it's a liability that’s actively draining your bank account.

Now, you might hear about seasoned investors who occasionally buy a negative cash flow property on purpose. This is a high-stakes gamble. They're betting that the property is in an area poised for explosive growth, and that the future appreciation will more than cover their monthly losses. It's a speculative play that requires very deep pockets and an iron stomach for risk.

For the vast majority of us, positive cash flow is the golden rule. It’s your financial buffer, the thing that lets your investment survive a surprise vacancy, a busted water heater, or a market dip without bleeding you dry.

Unless you have a very specific, well-funded appreciation strategy, you should make positive cash flow a non-negotiable part of any deal you even consider.

What Is a Good Cash Flow for a Rental Property?

This is the million-dollar question, and the honest answer is: it depends. There’s no single number that works for every market, every property, or every investor. Your goals and your local market conditions are what really matter.

That said, a few rules of thumb can help you quickly size up a deal. A lot of investors start with the $100 Rule, which suggests aiming for at least $100 in positive cash flow per door, per month. So, for a single-family home, that’s $100. For a duplex, you'd want $200.

For a more precise measure, look at your Cash-on-Cash (CoC) Return. This tells you how hard your actual invested money is working for you.

Formula: Annual Cash Flow / Total Cash Invested = CoC Return

Target: Many investors won't look at a deal unless it projects a CoC return of 8% to 12% or higher.

Ultimately, "good" cash flow is whatever meets your personal financial targets and gives you enough of a cushion to sleep well at night, knowing a surprise repair bill won’t sink you.

How Does Depreciation Affect Real Estate Cash Flow?

This is a fantastic question because it bridges the gap between your monthly bank statement and your annual tax return. Depreciation is a huge tax advantage for property owners that boosts your after-tax profit, even though it doesn't touch your basic cash flow calculation.

Here's how it works: the IRS lets you deduct a portion of your property's value from your taxable income each year to account for "wear and tear." The magic is that this is a "phantom expense." You get the tax deduction, but no actual money ever leaves your wallet for it.

Because this non-cash expense lowers your taxable income, you end up paying less in taxes. This means more of the cash your property generates actually stays in your pocket. So while depreciation won't show up in the simple cash flow formula we've been using, it's a critical piece of the puzzle for your real-world returns.

Navigating the complexities of rental property ownership can be challenging, but you don't have to do it alone. At Keshman Property Management, we use our 20 years of hands-on experience as landlords to make your investment journey less daunting and more profitable. Learn how our transparent, owner-focused services can maximize your cash flow today.

Comments