How to Calculate Rental Yield for Your Investment

- Sarah Porter

- Oct 4, 2025

- 10 min read

Figuring out your rental yield is like taking your property’s financial pulse. It’s a simple but powerful health check that tells you how much money your investment is actually generating from rent, relative to its value.

In simple terms, it's the percentage return you're getting from the rent alone.

Why Rental Yield Is a Metric You Can't Ignore

Before we jump into the formulas, let's get one thing straight: rental yield is the great equalizer for property investors. It lets you compare totally different properties—say, a downtown studio versus a three-bedroom house in the suburbs—on a level playing field. It cuts through the hype and shows you the raw income-generating power of an asset.

This single number is your go-to for evaluating a potential deal or checking up on a property you already own. It's the foundation for forecasting your cash flow and making sure you’re putting your money in the right place. To get a feel for what’s typical, it’s worth checking out the average rental yields across the U.S. to see how different markets stack up.

Gross vs. Net: The Two Sides of Yield

To really understand your investment's performance, you need to look at yield from two different angles.

Gross Rental Yield: Think of this as your quick-and-dirty calculation. It’s a fast look at your total annual rent against the property’s value, completely ignoring expenses. It's perfect for when you're first scanning listings and need a way to quickly sift the promising from the pointless.

Net Rental Yield: This is where the rubber meets the road. Net yield factors in all the real-world operating costs you'll actually pay—things like property taxes, insurance, maintenance, and management fees. This is the number that reveals your true profit margin.

Understanding both gross and net yield is non-negotiable. One gives you a quick snapshot for initial screening, while the other provides the detailed financial truth needed to make a sound investment decision.

Getting a handle on these calculations is what separates a casual landlord from a strategic investor. It’s the skill that helps you spot the truly good deals and avoid the ones that just look good on paper.

Core Components of a Rental Yield Calculation

To run the numbers correctly, you need to have a few key pieces of information handy. This table breaks down exactly what you'll need for both gross and net calculations.

Component | Description | Used In |

|---|---|---|

Annual Rental Income | The total rent collected over a 12-month period. | Gross & Net |

Property Value | The purchase price or current market value of the property. | Gross & Net |

Annual Operating Costs | All recurring expenses, such as taxes, insurance, and repairs. | Net Only |

These are the fundamental building blocks. Once you have these figures, you have everything you need to accurately assess your property's financial performance.

Calculating Gross Rental Yield for a Quick Snapshot

When you're first sizing up a potential investment property, you need a quick way to gauge its earning potential. That's where gross rental yield comes in.

Think of it as a back-of-the-napkin calculation. It's perfect for when you're scrolling through dozens of listings and need a fast, high-level comparison to see which properties are even worth a closer look. It gives you a raw look at performance by putting the annual rent up against the property's price tag.

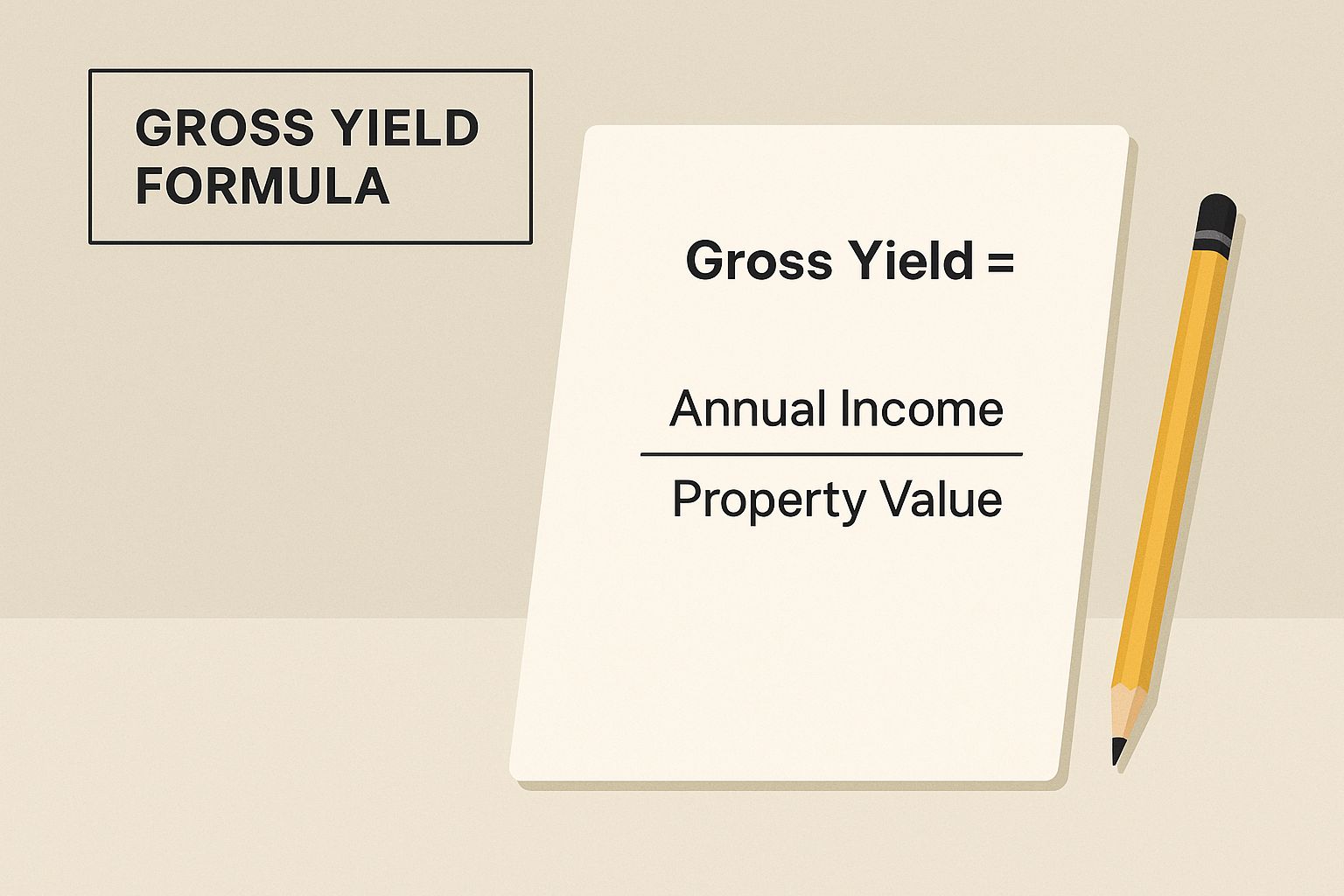

The Gross Yield Formula

The beauty of this formula is its simplicity. All you need are two numbers: how much rent you'll collect over a year and what you paid for the property (or its current market value).

Formula: (Annual Rental Income / Property Value) x 100 = Gross Rental Yield %

This calculation gives you a straightforward percentage, making it easy to compare different properties at a glance.

Let's put this into practice. Say you're looking at a house listed for $300,000. Based on comparable rentals in the area, you're confident you can get $2,000 a month in rent.

Here's how the math breaks down:

First, get your annual rental income: $2,000 per month x 12 months = $24,000

Next, plug it into the formula: ($24,000 / $300,000) x 100 = 8%

So, the gross rental yield for this property is 8%. It's a solid starting point, but remember what this number doesn't tell you. Gross yield completely ignores every single expense that comes with being a landlord—from taxes and insurance to repairs and property management fees.

This is why it’s just the first step. For a truer understanding of your bottom line, you'll need to dig deeper, and using a detailed rental property ROI calculator to maximize your investments can provide a more complete financial picture. Consider gross yield your initial filter before moving on to the more telling net yield calculation.

Calculating Net Rental Yield to See Your True Profit

Gross yield is a great starting point, a quick-and-dirty number to see if a property is even worth a second look. But net rental yield is where the rubber meets the road. This is the figure that shows you what you’ll actually put in your pocket after all the bills are paid.

Think of it this way: gross yield is your property's top-line revenue, but net yield is your bottom-line profit. It's the number that tells the true story of your investment’s health by factoring in the unavoidable costs of being a landlord.

This infographic lays out the simple gross yield formula, which we'll use as our foundation before digging into the details.

To get from that basic calculation to your true net yield, you need a clear picture of all your operating expenses.

Identifying Your Key Operating Expenses

Getting an accurate net yield means tallying up every recurring cost tied to the property. These aren't just one-off surprises; they're the predictable, ongoing expenses of owning an investment property.

Here are the most common operating costs you’ll need to track:

Property Taxes: An unavoidable annual expense from your local government.

Homeowners Insurance: Essential protection for your asset against damage and liability.

Routine Maintenance and Repairs: A smart landlord budgets for this. A good rule of thumb is to set aside 5-10% of your rental income for everything from a leaky faucet to a new dishwasher.

Property Management Fees: If you hire a pro to manage the property, their fee (usually 8-12% of the monthly rent) is a significant operating cost.

Vacancy Buffer: Properties don't stay occupied 100% of the time. It's wise to budget for turnover by setting aside a reserve, like 5% of your annual rent, to cover those empty months.

The good news is that many of these expenses can work in your favor at tax time. For a closer look at what you can write off, check out our landlord's guide to rental property tax deductions.

Net Yield Calculation in Action

Let’s go back to our $300,000 property that brings in $24,000 in annual rent. Now, we'll factor in some realistic annual expenses to see the real picture.

Property Taxes: $4,000

Insurance: $1,200

Maintenance & Repairs (5% of rent): $1,200

Vacancy Buffer (5% of rent): $1,200

Total Annual Expenses: $7,600

First, we need to calculate the net income:

$24,000 (Gross Rent) - $7,600 (Expenses) = $16,400 (Net Income)

Now, we can plug this much more accurate number into the yield formula:

(Net Annual Income / Property Value) x 100 = Net Rental Yield($16,400 / $300,000) x 100 = 5.47%

The difference is stark. The yield plummeted from a strong 8% (gross) to a much more sober 5.47% (net).

Gross Yield vs. Net Yield Worked Example

This side-by-side comparison clearly shows why you can't stop at the gross calculation.

Metric | Gross Yield Calculation | Net Yield Calculation |

|---|---|---|

Annual Rental Income | $24,000 | $24,000 |

Annual Operating Expenses | Not Included | $7,600 |

Net Operating Income | $24,000 | $16,400 |

Property Purchase Price | $300,000 | $300,000 |

Formula | ($24,000 / $300,000) x 100 | ($16,400 / $300,000) x 100 |

Final Yield | 8.00% | 5.47% |

This example perfectly illustrates a crucial point: failing to account for operating costs gives you a dangerously inflated sense of your return. In fact, it’s common for the net rental yield to be 30-35% lower than the gross figure, as noted by industry sources like AmericaMortgages.com. This is precisely why experienced investors always run the numbers for both.

So, What's a "Good" Rental Yield, Anyway?

You’ve run the numbers and now you have a percentage. But what does that little number actually mean for your investment? Honestly, there’s no magic answer. A “good” rental yield is completely dependent on your personal strategy, the market you're in, and the kind of property you own.

Think of it this way: an investor hunting for steady cash flow in a place like Cleveland might be looking for a higher yield, something around 7% or more. On the flip side, someone buying in a booming city like Austin might be perfectly happy with a 4% yield. Why? Because they're banking on the property's value skyrocketing over time. It's the classic tug-of-war between monthly income and long-term appreciation.

Setting Your Sights: What to Aim For

As a general rule of thumb, most seasoned investors find that a net rental yield between 5% and 8% hits the sweet spot. A yield in this range usually means the property is pulling in enough rent to cover all its expenses and still leave you with a decent profit. If your numbers are coming in lower, it could be a red flag that the property is overpriced or your operating costs are eating up too much of the income.

Remember, location is everything. A great yield in one city might be mediocre in another. The numbers can vary wildly not just between countries, but even between neighborhoods.

Looking globally, the differences are stark. As of the early 2020s, markets in Germany saw average gross yields around 3.4%. Meanwhile, in high-demand areas like the UAE, yields were soaring over 12%. You can see a full breakdown of global rental yields on Americamortgages.com to get a better sense of how different markets stack up.

Ultimately, interpreting your yield is all about context. It’s not about chasing a specific number, but about making sure the result fits your own financial goals. For another angle on measuring profitability, you might want to read our guide that explains what cap rate is in real estate investing, as it provides a different lens for evaluating a property's performance.

Common Mistakes Investors Make When Calculating Yield

Knowing the formulas is just the start. The real trick is avoiding the common pitfalls that can make a great-looking deal on paper turn into a money pit. I've seen it happen time and again—a simple oversight in the calculations completely tanks an investment.

Getting your numbers right from the beginning is what protects your capital and puts you on the path to real, long-term returns.

One of the most common mistakes? Forgetting about vacancies. It's so tempting to assume your property will be occupied 100% of the time, but that's just not realistic. Tenant turnover is a fact of life for landlords, so you absolutely have to account for at least a few weeks of lost rent between tenants.

Underestimating Your True Costs

Another classic blunder is lowballing the costs for maintenance and repairs. You might walk through a pristine-looking property and think, "What could possibly go wrong?" But trust me, something always does. A water heater fails, a faucet starts dripping, or an appliance gives up the ghost—these things add up fast.

Seasoned investors get ahead of this by setting aside a percentage of the monthly rent specifically for these surprises. A good rule of thumb is to earmark 5% to 10% for a dedicated repair fund. It’s a simple discipline that prevents a sudden expense from wrecking your cash flow.

A rental yield calculation is only as reliable as the data you put into it. Relying on overly optimistic numbers or ignoring likely expenses is a recipe for a poor investment decision.

Finally, a huge mistake is taking the seller's advertised rent at face value. A seller or their agent will often present a "pro forma" rent—an optimistic figure of what the property could rent for, not necessarily what it does or will rent for.

Don't fall for it. Always do your own homework. Jump on Zillow or talk to a local property manager to see what comparable units in the neighborhood are actually renting for. This simple step grounds your income projections in reality, not salesmanship, and gives you a much clearer picture of the property's true potential.

Common Questions About Rental Yield

Once you’ve got the hang of the basic formulas, you'll find that a few other questions naturally come up. These are the details that separate a spreadsheet investor from someone who truly understands the moving parts of their rental property's financial health. Let's dig into the most common ones I hear.

Should My Mortgage Payment Go Into the Net Yield Calculation?

This is a big one, and the answer is no. The standard net rental yield formula deliberately leaves out mortgage payments.

Why? Because net yield is meant to measure the performance of the property itself—its ability to generate income versus its direct operating costs. It’s a pure metric of the asset's efficiency, completely separate from how you chose to finance it.

The metric you're thinking of is cash-on-cash return. That calculation absolutely includes your mortgage, as it focuses on the return you get on the actual cash you pulled out of your pocket. Keeping these two calculations separate gives you a clearer picture: one tells you if the property is a good investment, and the other tells you if your financing deal was a good one.

What About Capital Appreciation?

Rental yield and capital appreciation are the two engines that drive your investment's total return, but they measure completely different things. You have to track them separately.

Rental Yield is all about the cash flow—the money the property puts in your pocket right now from rent.

Capital Appreciation is the long game. It’s the increase in your property’s value over time, which you only realize when you sell or refinance.

A killer investment usually has a solid mix of both. But in some hot markets, you might accept a lower yield because the potential for appreciation is just too good to pass up. They are two distinct, but equally vital, parts of your overall return on investment.

Think of it this way: rental yield is what pays the bills month-to-month, while appreciation is what builds your long-term wealth. Grasping this difference is key to building a balanced portfolio.

How Often Should I Re-Run the Numbers?

Things change, so your calculations should too. I strongly recommend recalculating your property's yield at least once a year. Think of it as an annual financial health check-up for your investment.

Beyond that, you should definitely recalculate anytime a major financial piece of the puzzle changes. Did you just raise the rent? Did a surprise roof repair blow up your maintenance budget for the year? Did property taxes go up? These events directly impact your bottom line and, therefore, your yield. Staying current with this number means you’re actively managing your investment, not just passively owning it.

Are Online Rental Yield Calculators Reliable?

Absolutely, as long as you use them correctly. Online calculators are fantastic for a quick gut-check, especially when you're in the early stages of comparing a dozen different listings and need to see which ones are even worth a closer look.

The catch is that they are only as good as the numbers you feed them. Never, ever rely on the default or estimated expenses they might provide. Do your own homework to find accurate figures for property taxes, insurance, and a realistic maintenance buffer. Use the calculator for the math, but use your own research for the inputs.

Are you looking for a partner to help you maximize your property's performance and boost your returns? Keshman Property Management uses over 20 years of hands-on experience to make owning rental properties more profitable and less stressful. We provide transparent, expert management to help you get the most from your investment. Learn more about our services.

Comments