A Landlord's Guide to Rental Property Tax Deductions

- Sarah Porter

- Sep 16, 2025

- 13 min read

When you own a rental property, you’re not just a landlord—you’re a business owner. And just like any other business, you have expenses. The good news is that the IRS allows you to subtract many of these expenses from your rental income, which lowers your taxable profit and, ultimately, your tax bill.

Think of it this way: every dollar you spend to keep your rental property running is a potential tax write-off. Learning how to identify and track these deductions is one of the most powerful skills you can develop as a real estate investor. It's the key to boosting your cash flow and getting the best possible return on your investment.

You're Running a Business—Act Like It

The single most important shift in mindset for a new landlord is to stop thinking of your property as just a passive asset and start treating it like a full-fledged business. A coffee shop owner wouldn't dream of paying for coffee beans out of their own pocket without writing it off. You should view the costs of running your rental property in the exact same way.

The IRS has a simple test for what you can deduct: any expense that is both "ordinary and necessary" for managing your rental property is fair game. "Ordinary" just means it’s a common expense for landlords, and "necessary" means it’s helpful for your business. It doesn’t have to be indispensable, just appropriate.

By stepping into the role of a business operator, you unlock a whole new level of financial strategy. Every legitimate expense you claim is a direct reduction of your taxable income, which means more money stays with you at the end of the year.

This guide is your roadmap. We’re going to walk through the world of rental property tax deductions step-by-step, breaking down each category with clear explanations and real-world examples. The goal is to give you the confidence to manage your property's finances like a pro and legally slash your tax burden.

To give you a bird's-eye view of what's possible, here’s a quick look at the most common types of deductions available to rental property owners.

Key Rental Deduction Categories at a Glance

Deduction Category | What It Covers | Common Examples |

|---|---|---|

Financing & Taxes | Costs associated with buying, owning, and paying taxes on the property. | Mortgage Interest, Property Taxes, Mortgage Insurance Premiums |

Insurance | Premiums paid for policies that protect your investment. | Landlord Insurance, Fire, Flood, and Liability Insurance |

Repairs & Maintenance | The cost of keeping the property in good working condition. | Plumbing repairs, painting, fixing broken appliances, landscaping |

Professional Services | Fees paid to professionals who help you manage or maintain your property. | Property Manager Fees, Legal Fees, Accountant/CPA Fees |

Depreciation | A non-cash deduction for the wear and tear on the property itself. | Depreciation of the building's value over 27.5 years |

Operational Costs | Day-to-day expenses required to run your rental business. | Advertising for tenants, tenant screening fees, utilities you pay |

This table is just the starting point. Now, let’s dive into each of these categories to make sure you’re not leaving any money on the table.

The Big Three Deductions: Mortgage Interest, Property Taxes, and Insurance

When you look at all the possible tax deductions for a rental property, a few heavy hitters almost always rise to the top. These are the ones that can make the biggest dent in your taxable income: mortgage interest, property taxes, and insurance.

Think of them as the bedrock of your tax-saving strategy. While you'll have dozens of smaller expenses, getting these three right is your first and most important step. They represent the core costs of owning and protecting your asset, and the IRS fully expects you to write them off as necessary business expenses. Let's dig into each one.

Deducting Your Mortgage Interest

For any landlord who financed their property, the mortgage interest payment is usually the single largest expense you can deduct. It's simply the cost of borrowing the money to buy the place in the first place.

Every year, your lender makes this easy by sending you Form 1098, the Mortgage Interest Statement. This form spells out exactly how much interest you paid over the last 12 months, and that's the number you'll report. Don't forget about other borrowing costs, too. Any "points" or loan origination fees you paid to get the loan can also be deducted, though you typically have to spread that deduction out over the life of the mortgage.

Claiming Property Tax Deductions

Property taxes are another major expense that you can—and should—deduct every single year. These are the taxes your local city or county government charges you to fund things like schools, roads, and emergency services.

The key here is that you deduct these taxes in the year you actually pay them. Your property tax bill or the year-end statement from your mortgage escrow account will give you the precise amount. For most landlords, these first two expenses—mortgage interest and property taxes—are the most powerful deductions in their toolkit. You can find more practical advice on how rental property taxes work on Rentastic.io to really get a handle on the numbers.

Important Note: You might have heard about the $10,000 cap on state and local tax (SALT) deductions. That limit is for your personal residence. It does not apply to your rental properties, which are considered a business. You can fully deduct all property taxes against your rental income.

Writing Off Insurance Premiums

Properly insuring your rental isn't just a good idea; it's a necessary cost of doing business. Thankfully, the IRS lets you deduct the premiums you pay for any insurance policies related to your rental property.

This goes beyond just your basic homeowner's policy. Make sure you're tracking and deducting all relevant insurance costs, which often include:

Landlord or Hazard Insurance: This is your main policy covering fire, theft, and other physical damage.

Liability Insurance: Absolutely crucial coverage in case a tenant or visitor gets hurt on your property.

Flood or Earthquake Insurance: If you're in an area prone to natural disasters, these separate policies are fully deductible.

Mortgage Insurance Premiums: If your lender required you to get PMI, that's a deductible expense as well.

By staying on top of these "big three," you’re laying a solid foundation for keeping more of your rental income in your pocket come tax time.

Deducting Operating Expenses and Maintenance Costs

Beyond the "big three" deductions, the everyday costs of keeping your rental property running are where you can find some serious tax savings. These are your operating expenses—every ordinary and necessary cost that comes with managing and maintaining your investment.

Think of your rental property like a car. The mortgage interest and property taxes are like the car payment and registration. The operating expenses? That’s the gas, oil changes, and new tires you need to keep it safely on the road.

One of the trickiest parts, though, is knowing the difference between a deductible repair and a capital improvement. In the eyes of the IRS, they are not the same. A repair keeps your property in good, working condition. A capital improvement, on the other hand, adds significant value, adapts the property to a new use, or extends its life.

Fixing a leaky faucet is a repair, and you can deduct that cost this year. But if you replace the entire plumbing system in the house, that's a capital improvement you'll have to depreciate over time.

The Repair vs. Improvement Test

Here’s a simple question to ask yourself: "Did this work restore the property to its previous condition, or did it make it fundamentally better?" Restoring is a repair. Making it better is an improvement.

The IRS is a stickler for this rule because it dramatically changes when you get to take the deduction. Getting this right is crucial for accurate bookkeeping and maximizing your write-offs without raising red flags. For a deeper dive into this, check out our guide on how to best manage property maintenance and repairs.

A repair is an immediate, fully deductible expense you can claim in the current tax year. An improvement becomes part of your property's cost basis and is deducted gradually through depreciation, often over many years.

Common Deductible Operating Expenses

To make sure you're not leaving money on the table, it helps to have a running list of the common expenses you can write off. These are the costs that keep your rental business humming and your tenants happy. Every single one is a valuable tax deduction you can claim in the year you paid for it.

Here are some of the most frequent operating costs you should be tracking meticulously:

Advertising: Any costs you incur to find tenants. This could be anything from Zillow listings to a "For Rent" sign in the yard.

Cleaning and Maintenance: The cost of getting the unit professionally cleaned between tenants, janitorial services for common areas, or any other routine upkeep.

Landscaping: Paying for lawn mowing, seasonal clean-ups, or gardening services to keep the property looking sharp.

Pest Control: The fees you pay for routine treatments to keep bugs, rodents, and other pests at bay.

Utilities: If you cover any utilities for the property, like water and sewer for a duplex or electricity for a common hallway, those bills are deductible.

Supplies: This covers all the small stuff that adds up, from lightbulbs and air filters to smoke detector batteries and cleaning products.

By diligently tracking these smaller, recurring expenses, you can make a huge dent in your taxable rental income. Every receipt you save is a piece of your profit that you get to keep.

The Power of Depreciation: Your Biggest Non-Cash Deduction

So far, we've talked about expenses you actually pay for out of pocket. But now we get to what is arguably the most powerful tax break in a real estate investor's toolkit: depreciation. This is a non-cash deduction, which means you get to claim it without spending a single dollar that year.

Think of it as an allowance the IRS gives you for the slow, steady wear and tear on your property. Every building, no matter how well-maintained, theoretically breaks down over time. Even if your property is skyrocketing in market value, the government lets you deduct a portion of its cost each year to account for this physical decline. It's a huge benefit.

How Depreciation Works: A Simple Example

Under current IRS rules, residential rental properties are depreciated over a period of 27.5 years. To figure out your annual deduction, you first need to determine the property's "cost basis." This is essentially the purchase price, plus some of your closing costs, but—and this is a key step—minus the value of the land itself. Why? Because land doesn't wear out.

Let's walk through an example. Imagine you bought a rental house for $350,000. Through an appraisal, you determine the land it sits on is worth $75,000. That leaves the building's value at $275,000.

Cost Basis of Building: $275,000

Depreciable Lifespan: 27.5 years

Annual Depreciation Deduction: $275,000 / 27.5 = $10,000

Just like that, you have a $10,000 deduction you can take against your rental income every single year for the next two and a half decades. It’s a massive reduction in your taxable income, all without spending any more money.

Unlocking Accelerated Savings with Bonus Depreciation

While the standard 27.5-year schedule is great, sometimes you can supercharge your savings with bonus depreciation. This special provision lets you deduct the entire cost of certain property components in the very first year you put them into service, as long as they have a useful life of 20 years or less.

We're talking about things like new appliances, landscaping, or carpeting. You can even uncover these opportunities through a cost segregation study, which breaks down a building into its various components. A major update reinstated 100% bonus depreciation for specific assets acquired after January 19, 2025, which can drastically lower your tax bill in the year you buy. You can learn more about the new bonus depreciation rules on wipfli.com.

By taking full advantage of depreciation, you're tapping into the engine that transforms a good real estate investment into a great, tax-efficient one.

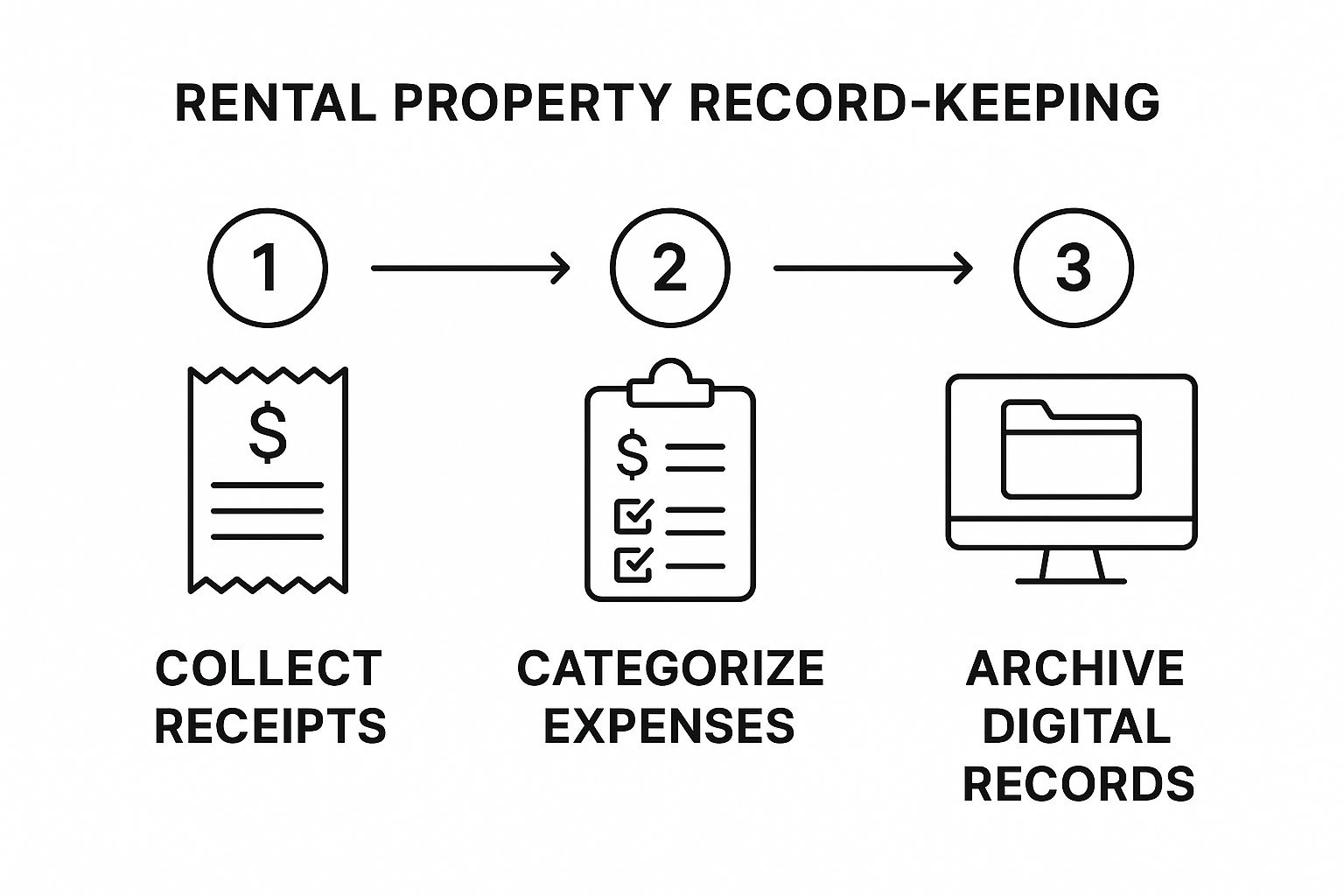

Of course, to properly claim depreciation and all the other deductions we've discussed, keeping meticulous records isn't just a good idea—it's absolutely essential. You need the documentation to back up every number on your tax return.

Advanced Deductions: Travel, Professional Services, and QBI

Once you've got a handle on the everyday deductions, you can start digging into some of the more advanced strategies to really minimize your tax bill. Think of these as the pro-level moves for serious investors—things like travel costs and professional fees that can make a huge difference.

If the basic write-offs are the foundation of your rental business, these advanced ones are the smart upgrades that boost your efficiency and profitability. They demand a bit more attention to detail, especially with record-keeping, but the payoff is well worth the effort.

Deducting Business-Related Travel Costs

Every trip you take for your rental business is a potential tax deduction. The IRS has specific rules, and it’s important to know the difference between your local jaunts and long-haul travel.

Local Transportation: This is all about the driving you do close to home. Think trips to your rental property, runs to the hardware store for supplies, or drives to meet a new tenant. You have two ways to claim this: the standard mileage rate (a simple cents-per-mile calculation) or the actual expense method, where you add up what you really spent on gas, oil, maintenance, and so on.

Long-Distance Travel: Have a property in another city or state? You can deduct what it costs to get there and back to manage it. This includes your flights, hotel stays, and even meals. The key here is that the main reason for your trip must be your rental business.

I can't stress this enough: for travel deductions, your records have to be rock-solid. Keep a mileage log in your car for local trips and save every single receipt from overnight travel. If you ever face an audit, this is the proof you'll need to back up your claims.

Writing Off Professional and Legal Fees

Good news—you don't have to be a one-person show. The money you spend on experts to help run your rental business is almost always fully deductible in the year you pay for it.

We're talking about fees for your accountant who handles your taxes, the lawyer who drafts your lease agreements or helps with an eviction, and definitely the property manager who handles the day-to-day operations. These are all considered standard, necessary costs of doing business.

The Qualified Business Income (QBI) Deduction

This one is a real game-changer, but it's surprising how many landlords miss it. The Qualified Business Income (QBI) deduction, also known as Section 199A, can be a massive tax saver. The QBI deduction lets eligible landlords write off up to 20% of their net rental income.

Let’s put that into perspective. If your property brings in $20,000 in net income for the year, the QBI deduction could knock $4,000 right off your taxable income. You can find more details about investment property taxes on Rentastic.io.

The catch? To qualify, your rental operation needs to be treated like a real trade or business, not just a passive hobby. This means you need to be regularly and consistently involved. Keeping detailed logs of the time you spend and the tasks you perform is the best way to show the IRS you mean business and deserve this powerful deduction.

Smart Record Keeping for an Audit-Proof Business

Claiming every tax deduction you're entitled to is only half the battle. The other, and arguably more important, half is being able to prove it if the IRS ever comes knocking.

Without solid records, even legitimate expenses can get thrown out during an audit. This can turn all those tax savings you worked so hard for into a massive, unexpected tax bill. The solution is simple: treat your rental property like the business it is, and that starts with business-quality bookkeeping.

This doesn't mean you need an accounting degree. A fantastic first step is to open a dedicated bank account and credit card just for your rental activity. This one move creates a clean financial trail, making it incredibly easy to separate your property's income and expenses from your personal finances. Trust me, your future self will thank you at tax time.

Your Document Retention Checklist

Once your accounts are separate, it’s all about systematically tracking and saving the right documents. Whether you prefer a simple spreadsheet or decide to use specialized software, consistency is key. Our guide on bookkeeping for rental properties made simple can walk you through setting up a system that you'll actually stick with.

To stay prepared, you'll want to keep a well-organized file (digital or physical) with these essential documents:

Lease Agreements: These are your proof of rental periods and income.

Proof of Income: Bank statements showing every rent deposit.

Expense Receipts: Keep everything! This includes receipts for repairs, supplies, professional services, and anything else you spend money on for the property.

Closing Documents & Mortgage Statements: You'll need these to figure out your property's cost basis and to deduct your mortgage interest.

Travel Logs: If you drive for your rental, keep a mileage log. Every trip to the hardware store or to meet a tenant adds up.

Insurance Policies: Hold onto these to document your premium payments.

Think of your records as your business's ultimate line of defense. Meticulous organization isn't just about staying compliant; it's about protecting your profits and giving you complete peace of mind.

Ultimately, this diligence is what elevates your rental from a casual side project to a professional, audit-proof business, paving the way for long-term financial success.

Frequently Asked Questions About Rental Tax Deductions

Diving into rental property tax deductions always brings up a few common "what if" scenarios. Getting these right is the key to both saving money and staying on the right side of the IRS. Let's walk through some of the questions I hear most often from landlords.

Handling Vacancy and Partial-Year Rentals

What happens when your property sits empty? Good news: you can still deduct expenses, but with one major string attached. The property must be genuinely available for rent.

This means you’re actively trying to fill it—running ads, showing the unit, and making it ready for a new tenant. As long as you're doing that, you can continue to deduct ordinary and necessary expenses like utilities, insurance, property taxes, and advertising costs during the vacancy.

The rules are a little different if you're converting your personal home into a rental partway through the year. You have to draw a clear line in the sand. You can only deduct expenses from the date the property was officially put on the market for rent. So, if you lived there until June and listed it for rent on July 1st, you can only deduct the mortgage interest, insurance, and other costs for the second half of the year.

Repairs vs. Improvements Explained

This is probably the most confusing—and most important—distinction for landlords to master. Getting it wrong can lead to serious headaches.

Here’s a simple way to think about it:

Repairs are all about keeping the property in its current working condition. Think of things like fixing a leaky faucet, patching a hole in the wall, or replacing a single broken window. These are fully deductible in the year you pay for them.

Improvements, on the other hand, add value, adapt the property to a new use, or significantly extend its life. Putting on a brand-new roof or completely remodeling a kitchen are classic improvements. These costs are handled differently; you have to "capitalize" them and deduct a portion of the cost each year through depreciation.

The core difference really comes down to restore vs. enhance. A repair brings something back to its original state, while an improvement makes it better than it was before. Misclassifying a major renovation as a simple repair is a red flag for the IRS.

And one last point that often trips people up: you cannot deduct the value of your own labor. While you can absolutely write off the cost of the paint, lumber, and other materials you buy for a project, the IRS doesn't let you pay yourself for your time and then deduct it.

Knowing what you can and can't claim is crucial, and that principle applies to security deposits, too. For a closer look at that, our guide explains what a landlord can deduct from a security deposit.

At Keshman Property Management, we handle the complexities so you can enjoy the rewards of ownership. With over 20 years of experience, we make owning rental properties less daunting and more gratifying. https://mypropertymanaged.com

Comments