What Is a Property Management Agreement?

- Sarah Porter

- Nov 26, 2025

- 18 min read

Think of the property management agreement as the rulebook that governs the entire relationship between you and your management company. It’s a legally binding contract that essentially acts as a business prenuptial—it gets everything out on the table before the partnership officially starts, protecting both of you by defining responsibilities, expectations, and how the money works. Honestly, it's the single most important document for safeguarding your real estate investment.

Why This Contract Is the Foundation of Your Investment

Imagine handing over the keys to your valuable asset based on nothing more than a handshake. It sounds risky because it is. Without a solid agreement in place, you’re opening yourself up to miscommunication, arguments over money, and tasks that fall through the cracks. It's a recipe for disaster.

This contract is what turns a casual arrangement into a professional partnership with clearly defined boundaries. It makes sure everyone is on the same page about how your property will be run day-to-day.

A well-crafted agreement doesn't just list a bunch of services; it builds a true framework for accountability. It defines what success looks like, establishes how you'll communicate, and gives you a roadmap for handling issues before they blow up.

The Core Purpose and Protections

At its heart, the agreement is all about clarity. It protects both you and the manager by spelling out the exact terms of your professional relationship, which is the key to making it a healthy and lasting one. It typically locks down several critical areas:

Defines Authority: The contract clearly states what decisions the manager can make on their own—like approving a small repair under a certain dollar amount—and when they need to pick up the phone and get your approval first.

Outlines Responsibilities: It gets into the nitty-gritty of all the duties, from marketing your vacancy and screening applicants to collecting rent and coordinating maintenance. You can learn more by checking out our guide on what to expect from a property management company.

Establishes Financial Terms: It provides a complete breakdown of the fee structure—the monthly management percentage, leasing fees, and any other charges you might encounter. No financial surprises.

The need for these clear, formal agreements is only growing. To get a better sense of how these documents are structured and their legal weight, it helps to understand the fundamentals of Texas real estate contracts. As more owners seek out professional help, the global property management market is expected to hit USD 52.99 billion by 2033, growing at a robust 10.4% each year. You can explore more insights on property management market trends on Precedence Research.

Breaking Down the Key Clauses in Your Agreement

A property management agreement can look like a wall of text filled with confusing legal jargon. I get it. But think of it less like a legal maze and more like a blueprint for a successful partnership. It’s the rulebook you and your manager agree to play by, and understanding those rules is the best way to protect your investment.

When you know what to look for, the whole document becomes much less intimidating. You can spot a good partnership from a mile away—and avoid the bad ones. Let’s walk through the five most important sections you'll find in any solid agreement.

The Scope of Services Clause

This is the "what are you actually going to do for me?" part of the contract. Honestly, it might be the most important section of all because it spells out exactly what you're paying for. If this part is vague, it’s a huge red flag and a recipe for future headaches.

A good agreement won't just say "property management." It will get into the nitty-gritty.

A strong clause will give you clear answers to questions like:

Marketing & Advertising: Where will you list my property? Will I have to pay extra for premium ads on sites like Zillow or Apartments.com?

Tenant Screening: What’s your screening process? Does it include a credit check, criminal background, and eviction history?

Rent Collection: How do you collect rent? What’s your process for chasing down late payments?

Property Inspections: How often are you stepping foot on my property? Just at move-in and move-out, or will you do periodic checks?

Financial Reporting: What reports will I get each month? A simple income statement or a more detailed profit and loss report?

Without this level of detail, it’s easy to assume a service is included when it isn’t. That’s how you get hit with surprise fees or find out a critical task has been overlooked.

Fee Structures and Compensation

Okay, let's talk about the money. This clause breaks down exactly how your manager gets paid. Transparency here is absolutely non-negotiable. Hidden fees can eat into your profits faster than anything else, so you need to understand every single charge. As you review this section, pay close attention to the details on residential property management costs—they will make or break your bottom line.

The demand for professional property management is growing for a reason. In Europe, the market was valued at USD 8.07 billion in 2025, and the United Kingdom's slice of that was a hefty USD 1.36 billion. This isn't just because there are more rental properties; it's because navigating regulations and tenant laws is getting more complex. A clear agreement protects everyone involved.

Here are the most common fees you'll see:

Monthly Management Fee: This is the big one, usually 8-12% of the monthly rent that's actually collected.

Leasing Fee: A one-time fee for the work of finding and placing a new tenant. It’s often equal to one month's rent.

Lease Renewal Fee: A much smaller fee for getting a great existing tenant to sign a new lease.

Maintenance Markup: Some companies add a small percentage (around 10%) to vendor invoices to cover the cost of coordinating repairs.

Vacancy Fee: Some managers charge a flat fee to look after your property while it's empty. Be sure to ask about this one.

Getting a handle on these different models is key to choosing the right partner. For a more detailed breakdown, check out our guide to property management fee structures.

Common Property Management Fee Structures Explained

This table breaks down the most common fee models you'll encounter in an agreement, helping you understand how managers are compensated.

Fee Type | Typical Range | What It Covers | Best For Owners Who... |

|---|---|---|---|

Percentage of Rent | 8-12% of collected rent | Day-to-day management, rent collection, tenant communication. | Prefer a fee structure directly tied to their property's performance. |

Flat-Fee | $100 - $200 per month | A fixed set of core management services, regardless of rent amount. | Own multiple similar properties and want predictable monthly costs. |

Leasing Fee | 50-100% of first month's rent | Marketing, showings, tenant screening, and lease signing. | Want to ensure the manager is motivated to find quality tenants quickly. |

À La Carte Fees | Varies | Specific, one-off services like eviction processing or property inspections. | Are more hands-on and only need help with certain management tasks. |

No single structure is "best"—it all comes down to what makes the most sense for your property and your personal management style.

Term and Termination Clause

Think of this as the prenup for your business relationship. It defines how long the agreement lasts and, more importantly, how either of you can end it if things go south.

Most contracts run for an initial term of one year and often include a clause for automatic renewal. The termination section should be crystal clear on a few points:

Notice Period: How much of a heads-up do you have to give to end the contract? 30 to 60 days is pretty standard.

Early Termination Fees: What’s the penalty if you need to leave before the year is up? It might be a flat fee or require you to pay out the remaining management fees.

Termination for Cause: What happens if one party just isn't holding up their end of the bargain? This lets you terminate immediately for things like negligence or fraud.

A fair termination clause is your safety net. If a company makes it incredibly difficult or expensive to leave, you have to ask yourself why. Good managers are confident they can keep your business with great service, not by trapping you in a contract.

Manager's Authority and Spending Limits

This clause draws a line in the sand, defining how much money your manager can spend on your behalf without calling you first. It's a critical boundary that protects you from surprise bills.

A typical agreement will require you to maintain a "maintenance reserve"—a small amount of cash, maybe a few hundred dollars, that the manager can use for minor repairs. The contract will also set a spending limit, often $300 or $500, for any single, non-emergency repair.

Here's how it plays out in the real world:A pipe bursts at 2 AM on a Saturday. You want your manager to have the authority to call an emergency plumber right away without needing your sleepy approval. But if the HVAC system dies and needs a $5,000 replacement, this clause ensures the manager has to get your explicit permission (and probably a few quotes) before moving forward.

This clause is all about balancing efficiency with your financial control. Small problems get solved fast, but you stay in the driver's seat for big decisions.

Maintenance and Repair Protocols

Building on the previous clause, this section lays out the "how" of maintenance. It defines the step-by-step process for handling repairs, which, if not clearly defined, can quickly become a point of frustration for everyone.

A good maintenance clause will cover all the bases:

Routine Upkeep: How are things like lawn care, snow removal, or pest control handled?

Repair Requests: What's the system for tenants to report an issue? How quickly is the manager expected to respond?

Vendor Selection: Does the manager have their own network of trusted vendors, or can you provide a list of your preferred contractors?

Emergency Procedures: What officially counts as an "emergency"? What's the plan of action when one happens?

By spelling all this out from the start, the agreement makes sure your property stays in great shape, your tenants feel taken care of, and you know exactly how things will be handled when something inevitably breaks.

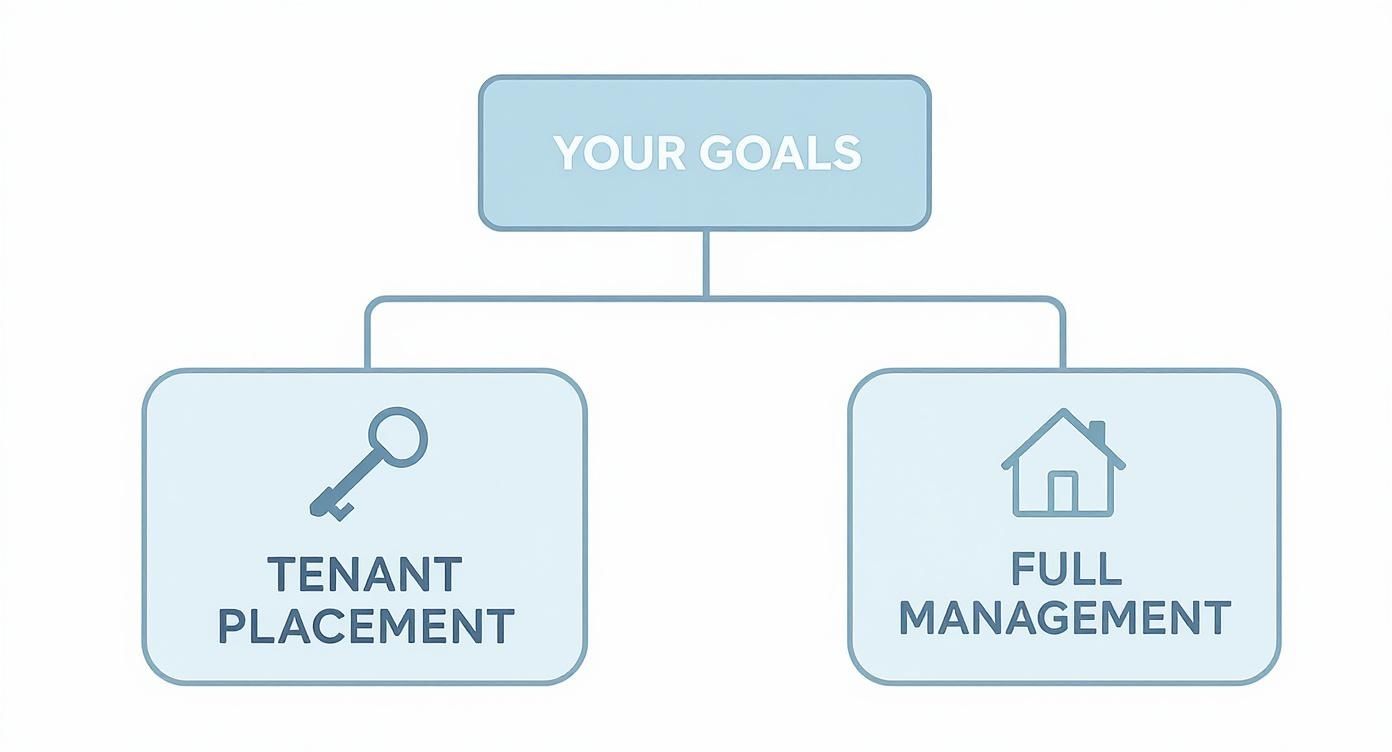

Finding the Right Agreement Type for Your Goals

Property management agreements aren’t a one-size-fits-all deal, and they shouldn't be. The right one for you hinges entirely on your goals, how involved you want to be, and the kind of property you own. Think of it like this: you wouldn't use a sledgehammer to hang a picture frame. Choosing the wrong agreement can be just as clumsy and frustrating.

The real aim here is to find a partnership that supports the lifestyle you want as an owner. Are you looking for a truly passive investment where you barely lift a finger? Or do you just need a professional to handle the most draining parts of being a landlord? Nailing down that answer is the first step toward a great relationship with your property manager.

This decision tree helps visualize the two main paths owners typically take, making it easier to see which agreement aligns with your end game.

As you can see, your core objective—whether it's just getting a great tenant in the door or achieving total freedom from day-to-day operations—points you directly to the right kind of contract.

Let's break down the most common models you'll encounter.

Full-Service Management Agreements

This is the all-inclusive, "set it and forget it" package. A Full-Service Management Agreement is exactly what it sounds like: you're handing over the keys to the entire operation. Your property manager takes care of everything from marketing vacant units and screening applicants to collecting rent, coordinating maintenance, and even handling the tough stuff like evictions.

This approach is built from the ground up for your peace of mind.

Who is this for? It’s the perfect fit for out-of-state investors, busy professionals, or anyone who wants their rental income to be truly passive. If you'd rather spend your time doing anything other than dealing with landlord duties, this is your agreement.

Leasing-Only Agreements

Maybe you don't mind managing the property day-to-day, but you absolutely dread the endless cycle of advertising, showing, and vetting potential tenants. In that case, a Leasing-Only Agreement (often called a Tenant Placement Agreement) is a game-changer. The property manager basically acts as a specialized recruiter for your rental.

Their job is laser-focused on a few key tasks:

Marketing your property to attract a deep pool of qualified applicants.

Handling all showings and answering questions from prospective tenants.

Running comprehensive background checks—credit, criminal history, and past evictions.

Preparing and executing a solid, legally compliant lease agreement.

Once the tenant signs the lease and gets the keys, the manager’s work is done. You take it from there, handling all future communication and management.

Who is this for? This is a fantastic option for local, hands-on owners who have the time and know-how for daily management but want to tap into professional resources to find a reliable, long-term tenant.

A Leasing-Only contract lets you use a manager’s powerful marketing reach and rigorous screening process without locking into a long-term, full-management relationship. It solves what is often the single biggest headache of landlording.

À La Carte or Custom Service Agreements

Sometimes your needs don't fit neatly into a standard package. That’s where À La Carte Agreements come into play. This flexible model lets you pick and choose individual services to create a custom plan. Maybe you only need help with rent collection, or perhaps you just want a pro to handle biannual property inspections.

With this approach, you build your own service package. You only pay for what you need, making it a smart, cost-effective choice for owners who have a very specific gap to fill.

Who is this for? This is tailor-made for experienced landlords who have a good handle on most things but want to outsource one or two tasks that are particularly time-consuming or fall outside their wheelhouse.

Negotiating Your Agreement and Spotting Red Flags

Think of a property management agreement less like a set of terms and conditions you click "agree" to and more like the constitution for your investment. This isn't just a formality; it's the rulebook for a critical business relationship that governs how your most valuable asset is handled.

The goal here isn't to be confrontational. It's about achieving crystal-clear alignment. A truly professional property manager will welcome your questions because they understand that a transparent, fair agreement is the bedrock of a long-term partnership. This negotiation is your first—and best—chance to shape that relationship from the ground up.

Red Flags That Should Make You Pause

Before you even think about negotiating terms, you need to develop an eye for potential trouble. Certain clauses, or sometimes a conspicuous lack of detail, can be early warning signs of future headaches. If you see any of the following, it’s time to slow down and ask some hard questions.

Vague Service Descriptions: Be wary of phrases like "standard maintenance" or "aggressive marketing." What does that actually mean? If the contract doesn't spell out exactly what's included, you could find yourself paying extra for services you assumed were part of the deal.

Excessive Manager Authority: Look for language that gives the manager free rein to approve major repairs or sign leases well below market rate without your explicit consent. You should always hold the final say on big decisions.

Punitive Termination Clauses: Some termination fees are normal to cover a manager's costs, but they shouldn't feel like a punishment. If the penalty for ending the contract early is exorbitant, it can effectively trap you in an underperforming partnership.

No Performance Guarantees: A confident management company often backs up their promises with guarantees, like promising to place a qualified tenant within a certain timeframe. A total absence of any performance standards might signal a lack of confidence in their own services.

A property management agreement that is difficult to understand is often difficult to enforce. Ambiguity rarely benefits the property owner; it creates loopholes that can lead to unexpected costs and diminished control over your investment.

A Practical Checklist for Review

To make this easier, we’ve put together a quick-reference table. Use this checklist as you read through any proposed agreement to help you identify common problem areas and understand what a fairer alternative looks like.

Property Management Agreement Red Flag Checklist

Red Flag Clause | Potential Risk to Owner | What to Negotiate Instead |

|---|---|---|

Management fee based on rent due, not rent collected. | You pay the manager even when the tenant doesn't pay you. | The fee should be a percentage of "rent collected" or "monies collected" only. |

Automatic renewal with no clear opt-out window. | You could be locked into another full year of service unintentionally. | Request a month-to-month term after the initial period or a generous 60-day notice window for non-renewal. |

Manager has sole authority over tenant selection. | You lose control over who lives in your property, potentially accepting a risky applicant. | The contract should state that the owner gives final approval on all tenant applications. |

Undefined spending limit for maintenance. | The manager can authorize expensive repairs without your knowledge or approval. | A specific dollar amount (e.g., $300 or $500) that requires your written authorization before being exceeded. |

The manager can use affiliated maintenance companies. | Potential for inflated repair costs or conflicts of interest. | A clause requiring competitive bids for repairs over a certain amount or full disclosure of any affiliate relationships. |

Treat this table as your first line of defense. If you spot any of these clauses, it doesn't necessarily mean you should walk away, but it absolutely means you need to start a conversation.

Actionable Negotiation Tactics

Once you’ve spotted the areas that need work, it's time to negotiate. Don't be shy. Most terms in a standard agreement are more flexible than they appear. The key is to approach the conversation with specific, reasonable requests.

Focus on the clauses that have the biggest impact on your bottom line and your peace of mind.

Set Firm Spending Limits

One of the easiest and most powerful things you can negotiate is the maintenance spending limit. If the contract allows the manager to spend up to $500 on a repair without calling you, but you'd feel better at $250, say so. This simple change ensures you stay in the loop on all but the most minor fixes.

Propose a Shorter Initial Term

Instead of a standard one-year contract, ask for an initial term of six months with a clause to review and renew. This gives both sides a low-risk trial period. A manager who is confident in their service quality will often agree, knowing their performance will earn your long-term business.

Clarify Fee Structures Down to the Penny

Get granular with the fee schedule. Ambiguity here will always cost you money. Ask pointed questions like:

"Is your management fee calculated on rent collected or rent due?" You only want to pay for income you’ve actually received.

"Do you add any markups or surcharges to vendor invoices for repairs?" If so, what is the exact percentage?

"What specific actions does the tenant placement fee cover?" Does it include professional photography, listing syndication to top sites, or tenant screening costs?

Finally, get everything in writing. Any changes, clarifications, or verbal agreements you make must be documented in the final contract or as a formal addendum. This protects you from future "misunderstandings" and solidifies a strong foundation for a profitable, stress-free partnership.

How Keshman Delivers Transparent Agreements

Knowing what to look for in a property management agreement is one thing. Finding a partner who actually lives up to those standards is another challenge entirely. At Keshman Property Management, we see the contract as more than just a legal formality—it's the blueprint for a partnership built on trust and mutual respect.

We've been in this business long enough to see how vague clauses and surprise fees can sour a relationship and turn a great investment into a source of constant stress. That’s why we built our agreements from the ground up to be the antidote to those common industry problems. Our approach is simple: create owner-focused contracts that are fair, transparent, and designed for a healthy, long-term partnership.

Our Commitment to Clear Fee Structures

Let's be honest: most conflicts between owners and managers come down to money. Ambiguous fee structures are a huge red flag, which is precisely why we’ve gotten rid of them.

With Keshman, what you see is what you get. Our agreements spell out every potential cost in plain English, so you’re never caught off guard by a surprise line item on your statement. We operate on a simple, powerful principle: we only get paid when you get paid. Our management fee is based on rent collected, not just what's due, which means our success is directly tied to yours.

We’ve built our business on the idea that transparency isn’t just a nice-to-have—it's a non-negotiable. A great partnership can't survive on financial surprises, so we make sure our agreements provide total clarity from day one.

Well-Defined Communication and Maintenance Protocols

Feeling out of the loop is a major frustration for property owners, especially when it comes to repairs and maintenance. Our agreements tackle this head-on by setting up crystal-clear protocols for how and when we communicate with you.

We establish a pre-approved spending limit, usually around $300, that allows us to resolve minor issues quickly without needing to bother you for every little thing. For any repair that costs more, you get a detailed request with vendor quotes for your approval. This system strikes the perfect balance, giving us the efficiency to keep your property in great shape while ensuring you always have control over major expenses.

Here's how our process gives you peace of mind:

Clear Authority Limits: We handle the small stuff right away, keeping tenants happy and preventing minor problems from becoming major ones.

Owner Approval on Major Costs: You always have the final say on any significant spending. No exceptions.

Proactive Updates: You’ll stay informed on maintenance progress through your dedicated owner portal.

Technology That Drives Real-Time Insight

A modern management agreement is only as good as the technology that backs it up. We give every Keshman client access to a powerful owner portal that brings the financial clauses in your contract to life.

Instead of waiting around for a monthly statement to arrive in the mail, you can log in any time and see exactly what's happening with your investment.

Up-to-the-minute rent payment statuses

Detailed expense reports with attached vendor invoices

Lease documents and important notices

Comprehensive financial reports on your property’s performance

This technology turns our agreement into a living document. It’s not some piece of paper you sign and file away; it’s a dynamic tool giving you on-demand insight into the health of your investment. By pairing our clear, fair contract terms with robust technology, we turn the management agreement from a potential source of conflict into the very foundation of a successful and profitable partnership.

Your Final Checklist Before You Sign

We've covered a lot of ground—from dissecting clauses to spotting red flags and learning how to negotiate. Now it's time to bring it all together. Before you even think about signing, one final, thorough review of the property management agreement is your most important safeguard. This isn’t just about ticking boxes; it’s about making absolutely sure the contract reflects the fair and transparent partnership you’re signing up for.

Think of it like a pilot's pre-flight check. A few minutes of focused attention now can save you from a world of headaches and turbulence later on. This last look ensures you’re stepping into the relationship with your eyes wide open, leaving no room for those costly "I thought that meant..." misunderstandings.

Core Questions for Your Final Review

To get the most out of this final pass, approach it like an audit. Go through the document with a specific list of questions that get right to the point. You shouldn't move forward until you can give a confident "yes" to every single one.

Financial Clarity: Have I verified every single management fee, leasing fee, and potential add-on charge? Do I know precisely how and when I’ll receive my money?

Defined Responsibilities: Is the scope of services laid out in plain English? Are my duties as the owner and the manager's responsibilities clearly distinguished?

Termination Terms: Is the exit strategy fair and easy to understand? Do I know the exact notice period and any costs associated with ending the contract early?

Authority and Control: Is there a specific spending limit for maintenance that triggers the need for my approval? Do I have the final say on who rents my property?

Legal and Compliance: Does the agreement confirm the manager will follow all local, state, and federal laws, especially fair housing regulations?

Getting clear answers here covers the major friction points where owner-manager relationships tend to break down.

This final checklist is your last chance to turn the concepts in this guide into real-world protection for your investment. It’s where due diligence stops being a buzzword and becomes a tangible shield for your asset.

By double-checking these key areas, you confirm that the agreement is more than just a boilerplate template—it’s a document customized to protect your interests. This level of detail should carry through to all your operations; for instance, using a solid rental lease agreement template for your tenants creates consistency. Taking this moment to pause and verify builds the strongest possible foundation for your new business partnership.

A Few Common Questions, Answered

When you're about to hand over the keys to your investment property, it's natural to have questions. You're not just signing a document; you're starting a business relationship. Let's tackle some of the most common "what if" scenarios that owners ask about before, during, and after signing on the dotted line.

Can I Get Out of a Property Management Agreement Early?

The short answer is yes, but it’s rarely as simple as just walking away. Your contract's termination clause is the rulebook here, and it will lay out the exact steps you need to follow.

Most agreements require you to give written notice, usually somewhere between 30 and 60 days, before you can officially end things. If you're trying to break the contract before the initial term is up, you'll likely face an early termination fee. This could be a flat penalty of a few hundred dollars or, in some cases, you might be on the hook for all the management fees that would have been paid through the end of the contract term.

However, if you're firing your manager for failing to do their job (this is called terminating "for cause"), you can often avoid those fees—but you'll need a solid paper trail to prove they dropped the ball.

What If My Property Manager Isn't Doing Their Job?

This is a landlord's nightmare. Maybe they've failed to find a tenant, let a leaky roof go for weeks, or aren't accounting for expenses properly. This is legally considered a breach of contract, and your agreement should give you a path forward.

If you find yourself in this situation, here’s the game plan:

Document Everything. Create a detailed log of every issue. Note the dates, take pictures, and save all emails and text messages. Proof is your best friend.

Send a Formal Notice. Don't just make an angry phone call. Draft a professional letter or email that clearly states how they've violated the agreement, pointing to the specific clauses if you can.

Give Them a Chance to Fix It. Most contracts include a "cure period," which is a reasonable window of time for the manager to correct the problem.

Terminate for Cause. If they still don't resolve the issues after the notice and cure period, you can move forward with termination according to the steps laid out in your contract.

Think of your property management agreement as a two-way street. It holds both you and your manager accountable. When one side doesn't live up to their promises, the agreement provides the framework to either fix the problem or dissolve the partnership while protecting your asset.

Is It Okay to Negotiate the Agreement?

Absolutely—in fact, you should. A property management agreement is not a non-negotiable slab of stone. It’s the blueprint for a long-term partnership, and you should feel comfortable with every single term before you sign.

Everything from the management fee percentage and maintenance spending limits to the contract length and termination penalties can be on the table. If a clause seems vague or one-sided, ask for it to be clarified or changed. A good property manager won't be offended; they'll welcome the conversation because it sets the stage for a transparent and healthy relationship from day one.

At Keshman Property Management, we believe a strong partnership starts with a clear and fair agreement. Our contracts are designed to align our success directly with yours, no confusing jargon included. If you’re looking for a property management team that prioritizes your profitability and peace of mind, visit our website to learn more about our services.