How to Set Up an LLC for Rental Property: A Quick Starter Guide

- Sarah Porter

- Feb 6

- 17 min read

Updated: Feb 14

When you decide to set up an LLC for your rental property, you're essentially building a financial fortress. The process involves a few key steps—choosing a state and a unique name, filing the official paperwork (called Articles of Organization), and drafting an Operating Agreement. This structure is what separates your personal finances from your business liabilities, protecting your home and savings from any issues that might pop up at your rental. It's the first real step toward running your property like a secure, professional business.

Why an LLC Is Your First Line of Defense

Being a landlord is about more than just collecting rent checks; it’s about managing risk. An LLC isn't just a piece of paper or a business formality—it's your financial shield.

Think about this real-world scenario: a tenant slips on an icy walkway one winter morning and decides to sue. If you own the property in your own name, that lawsuit could come after everything you own—your family home, your car, even your retirement accounts. It’s a terrifying thought.

Now, let’s replay that scene, but this time your property is held inside an LLC. The lawsuit is filed against the business, not you personally. That legal separation, often called the corporate veil, is the number one reason landlords and investors flock to LLCs. It contains the financial damage from business disputes, making sure a problem at your rental doesn't spiral into a full-blown crisis in your personal life.

The trend speaks for itself. We're seeing that over 70% of new landlords are now choosing to form an LLC for their rental properties. This isn't a coincidence; it's a strategic move driven by the need for smarter asset protection and tax flexibility.

The Core Benefits of an LLC for Your Rental

Beyond just protecting you from lawsuits, forming an LLC fundamentally changes how you operate. It elevates your rental from a casual side hustle into a legitimate business, and that shift comes with some powerful advantages.

Ironclad Asset Protection: This is the big one. An LLC creates a totally separate legal entity. Your business assets (the rental property) are walled off from your personal assets (your home, savings, and other investments). This is absolutely critical for your long-term financial security.

Enhanced Credibility and Professionalism: Let’s be honest, "Oak Street Properties, LLC" sounds a lot more official than just your personal name. This professional polish makes a real difference when you're dealing with tenants, contractors, and especially lenders. They tend to view a formal business structure as more stable and serious.

Flexible Tax Strategies: One of the best parts about an LLC is its tax flexibility. By default, a single-member LLC is a "pass-through" entity. This means all the profits and losses are reported on your personal tax return, so you avoid the dreaded double taxation that corporations face. It keeps tax time simple while giving you the legal protection of a much more complex entity.

The real power of an LLC is that it allows you to take calculated risks in real estate investing without betting your entire personal financial future. It's the difference between being a hobbyist and a strategic business owner.

Here’s a quick comparison to see how an LLC stacks up against simply owning the property in your own name.

Landlord Structure At a Glance: LLC vs. Sole Proprietorship

Feature | Sole Proprietorship (No LLC) | Limited Liability Company (LLC) |

|---|---|---|

Liability | Unlimited personal liability. Your personal assets are at risk. | Limited liability. Protects personal assets from business debts and lawsuits. |

Legal Entity | You and the business are legally the same. | Creates a separate legal entity from the owner(s). |

Credibility | Lower perceived professionalism. May be seen as a side project. | Higher professional credibility with tenants, banks, and vendors. |

Taxes | Simple pass-through taxation on your personal return. | Flexible taxation. Can be taxed as a pass-through entity or a corporation. |

Setup & Fees | No formal setup required. No state filing fees. | Requires filing with the state and paying initial and annual fees. |

While a sole proprietorship is free and easy, the lack of a liability shield is a risk most experienced investors aren't willing to take. The LLC offers the best of both worlds: robust protection with simple management.

This structure also just makes it easier to keep clean financial records and breeze through tax season. But remember, while an LLC is your primary shield, it doesn't replace good insurance. You can explore our guide on landlord liability insurance to understand how to layer your protections for maximum peace of mind.

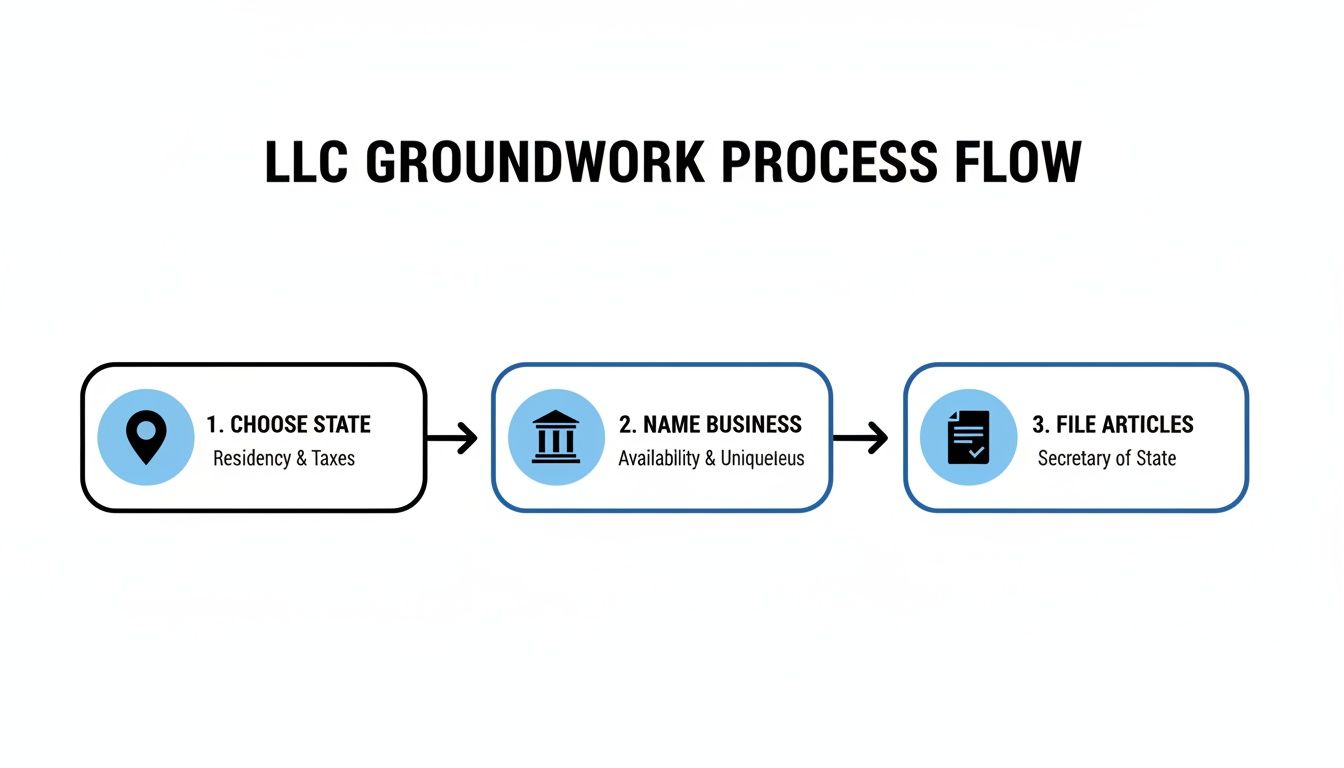

Laying the Groundwork Before You File

Before you even touch a single piece of official paperwork, there are a couple of big-picture decisions you need to nail down. I’ve seen countless new investors rush this part, and it almost always leads to a mess of extra costs and headaches later. Think of this as pouring the concrete foundation for your investment—get it right, and everything you build on top of it will be solid.

The first, and most critical, question you need to answer is where to form your LLC. This is far more than a simple matter of convenience; it has major legal and financial consequences.

Choosing the Right State for Your LLC

It’s easy to get lured in by the hype around states like Wyoming, Delaware, or Nevada. You hear about their low fees, strong privacy protections, and lack of state income tax, and it all sounds incredibly tempting.

But for most rental property owners, the golden rule is simple: form your LLC in the state where your property is physically located.

Why? Because real estate is always, without exception, governed by the laws of the state it sits in. If you own a duplex in Florida but set up a Wyoming LLC to hold it, you haven't cleverly sidestepped Florida’s laws. You’ve just made your life more complicated.

Your Wyoming LLC will have to register as a "foreign entity" to legally do business in Florida—you know, little things like collecting rent and signing leases. Suddenly, you're on the hook for fees and annual reports in two states. You've just doubled your admin work and your costs, all for little to no actual benefit.

For the vast majority of landlords, especially if you have just one or a few properties in the same state, keeping it local is the most direct, cost-effective, and legally sound move you can make.

The local real estate market itself matters, too. If you're in a landlord-friendly state like Texas or Wyoming, having an in-state LLC keeps your entire operation aligned with those favorable local laws. Even with nearly 500,000 new rental units hitting the market across the country, the underlying demand is strong. An LLC gives you the agility to adapt, and keeping it local just makes that easier. You can read more about the current long-term rental housing demand on RealPage.com.

Naming Your Rental Property LLC

Okay, so you've picked your state. The next step is giving your LLC a name. This isn't just about branding; it’s a legal checkpoint. The name you choose has to be unique in that state—it can't be the same as, or too similar to, any other registered business.

Almost every Secretary of State website has a free online business name search tool. Use it. In fact, use it a lot. Brainstorm a handful of options before you get too attached to one.

Here are a few practical tips from my own experience:

Add the Official Designator: Your business name has to end with "Limited Liability Company," "LLC," or "L.L.C." This is a non-negotiable legal requirement that tells the world about your liability protection.

Go for Professional but Anonymous: Try to avoid using your own name, like "John Smith Rentals LLC." Something a bit more generic, like "123 Elm Street Properties LLC" or "Blue Ridge Holdings LLC," adds a layer of privacy and sounds more established.

Check for Availability First: Seriously, run that search before you do anything else. If your name is taken, the state will reject your filing, and you'll be back to square one. It's a frustrating and totally avoidable delay.

Think About the Future: Choose a name that can grow with you. "Elm Street Properties" might feel a bit awkward if you sell that property and buy one on Oak Avenue. A broader name gives you more flexibility down the road.

Getting these two things—your state of formation and your business name—locked in first makes the actual filing process a breeze. It’s the necessary prep work that paves the way for a well-protected and successful rental business.

The Nuts and Bolts of LLC Formation

Alright, you’ve picked your state and locked in a great name. Now it’s time to take that idea and turn it into a real, legal entity. This is the part that seems intimidating, with all the official forms and government filings, but it really just boils down to a few straightforward steps to get your rental property LLC off the ground.

Think of it as laying the foundation. It's a clear, linear path from idea to reality.

Let's break down exactly what you need to do to make it official.

Filing Your Articles of Organization

The very first piece of paperwork you'll tackle is the Articles of Organization. The best way to think of this document is as your LLC's birth certificate. It’s the public document you file with your state's Secretary of State that officially puts your business on the map.

While the specifics can vary a little from one state to the next, you'll pretty much always need to provide some core details:

Your LLC's Name: The unique, approved name you already picked out.

Business Address: This needs to be a physical street address, as most states won't let you use a P.O. Box.

Registered Agent Information: You have to designate a person or a service that will accept official legal and tax mail on your LLC's behalf. This ensures there's always a reliable point of contact.

Management Structure: You'll state whether the LLC is member-managed (run by the owners themselves) or manager-managed (run by an appointed manager).

The filing fees are usually manageable, but they can vary wildly. Some states are incredibly investor-friendly. Wyoming, for instance, charges just $100 to file and only $60 a year after that, plus it has no state income tax. Texas is another popular choice, with a $300 filing fee and no income tax.

Then you have the other end of the spectrum. California hits you with an $800 annual franchise tax and has notoriously tough tenant laws, making it one of the most challenging states for a rental LLC. For a deeper dive into these costs, you can find a great state-by-state LLC breakdown on BusinessRocket.com.

Crafting Your Operating Agreement

If the Articles of Organization are the birth certificate, the Operating Agreement is your company's internal rulebook. This document is absolutely critical, even if you're the only owner. It's a legally binding agreement that lays out how your LLC will be managed and how the finances will be handled.

This is an internal document, so you won’t be filing it with the state. Its real purpose is to head off disagreements before they start and to provide a clear roadmap for running the business. For a single-member LLC, it’s a powerful tool for proving your business is a legitimate, separate entity. For a multi-member LLC, it's simply non-negotiable.

Your agreement should clearly spell out:

Ownership Percentages: Who owns what slice of the pie.

Profit and Loss Distribution: How money will be divided up among the members.

Management Roles and Responsibilities: Who’s in charge of what on a day-to-day basis.

Voting Rights: How you'll make the big decisions.

Exit Strategy: A plan for what happens if a member wants out, sells their share, or passes away.

Never skip the Operating Agreement. It's the single most important document for protecting your business from internal disputes and proving to a court that your LLC is a legitimate, separate entity.

Securing Your Employer Identification Number (EIN)

The last piece of the foundation is getting an Employer Identification Number (EIN) from the IRS. An EIN is basically a Social Security Number for your business. It's a unique nine-digit number the IRS uses to identify your LLC for tax purposes.

Getting an EIN is completely free, and you can apply for it online in just a few minutes directly on the official IRS website.

You'll definitely need an EIN if:

Your LLC has more than one owner (it's taxed as a partnership).

You plan on hiring anyone, even part-time help.

You elect to have your LLC taxed as a corporation.

Even if you're a single-member LLC and not technically required to get one, you should do it anyway. Why? Because you'll need it to open a business bank account, which is a must-do for keeping your liability protection intact. Using an EIN for business matters instead of your personal Social Security Number adds another thick, solid wall between your personal and business finances.

Making Your LLC Real: The Financial Setup

So, you've got your Articles of Organization. Your LLC is officially a legal entity. But let's be real—a piece of paper can't collect rent or pay a plumber. Now we get to the crucial part: giving your company financial legs and formally tying it to your rental property.

If you get this part wrong, it’s like building a fortress and leaving the front gate wide open. This is where you draw a hard line in the sand between your business and personal finances, which is the entire point of this exercise.

Open a Dedicated Business Bank Account

First thing’s first. Take your EIN and your formation documents down to the bank and open a checking account in the LLC’s name. This isn't just a friendly suggestion; it's the bedrock of your liability shield. From now on, every dollar of income—rent, late fees, pet deposits—goes into this account. And every expense—the mortgage, repairs, insurance, property taxes—comes out of it.

Mixing your personal and business money is called commingling, and it's the fastest way to get your LLC’s liability protection thrown out in court. If you ever face a lawsuit, the other side's attorney will be digging for any proof that your LLC is just you operating under a different name. A shared bank account is Exhibit A for their case.

Think of it this way: your business bank account is the physical wall that enforces your corporate veil. Keeping the money separate is how you prove to a judge that your LLC is a legitimate, stand-alone business.

Transfer the Property Title into the LLC's Name

Your LLC doesn't actually own your rental property until its name is on the title. This is done by preparing and recording a new deed, which formally transfers ownership from you as an individual to your LLC. It’s a critical step that many people overlook.

You’ve got a couple of options for the deed, and the choice matters.

Quitclaim Deed: This is the go-to for most investors moving property into an LLC they own. It's simple and fast. A quitclaim deed basically says, "Whatever ownership interest I have, I'm transferring it to the LLC." It makes no warranties about the title's history.

Warranty Deed: This deed goes a step further by guaranteeing the title is free and clear of any outside claims. While essential for a normal sale to a third party, it's often more than you need when you're essentially just moving the property from your right pocket to your left.

For most landlords, a quitclaim deed gets the job done perfectly. That said, I always recommend having a real estate attorney draft and record it. They'll make sure it's done right according to your state's specific rules, helping you avoid a massive headache later on.

Tackling the Dreaded "Due-On-Sale" Clause

Alright, let's talk about the elephant in the room: the "due-on-sale" clause. Buried in the fine print of nearly every residential mortgage is a clause that says your lender can demand the entire loan balance be paid immediately if you sell or transfer the property without their permission.

And yes, transferring the title to your LLC technically triggers it. The big question is, will the bank actually call the loan?

From my experience, it's rare, especially if you have a single-member LLC and you're still the one in charge. Lenders are in the business of collecting interest, not foreclosing on performing loans. As long as the checks keep clearing, they're usually happy.

The key here is proactive communication. Don't just file the deed and cross your fingers. Call your lender. Explain you're moving the property into a personal LLC for liability protection and confirm that you remain personally on the hook for the loan. Some will send a letter giving their blessing, while others might suggest refinancing into a commercial loan.

If you're looking at different funding avenues, our guide on how to finance a rental property covers seven solid strategies that pair well with an LLC structure.

By getting the banking and title transfer right, you're not just checking boxes. You're building a solid legal and financial foundation for your rental business, making sure your personal assets stay exactly where they belong—with you.

Keeping Your Legal Shield Strong

Getting your LLC set up is a fantastic first step, but think of it as the starting line, not the finish. The legal shield you've just built is only as strong as your commitment to maintaining it. If you treat your LLC like a real business, the courts will too. But if you neglect it, that "corporate veil" you're relying on can become dangerously thin.

This all comes down to a shift in mindset. You're no longer just a property owner; you're running a business. This means adopting a few straightforward, non-negotiable annual habits that prove your LLC is a legitimate, separate entity.

Annual Compliance and Reporting

Every state has its own set of hoops to jump through to keep your LLC in "good standing." Drop the ball on these deadlines, and you could face fines, penalties, or even the administrative dissolution of your company. If that happens, your personal assets are suddenly right back in the line of fire.

Most states boil this down to two main requirements:

Annual Reports: This is usually a simple online form you file each year to confirm your business details, like your current address and registered agent. The form is easy, but the deadline is strict.

Franchise Taxes or Fees: Some states, like California and Delaware, will charge you an annual tax or fee just for the privilege of existing. This is completely separate from any income tax you owe on your rental profits.

Do yourself a huge favor: set a recurring calendar reminder for these dates right now. Forgetting to file is an amateur mistake with professional-level consequences.

An LLC is not a "set it and forget it" tool. Consistent maintenance is the only way to ensure the liability protection you worked so hard to establish remains intact when you actually need it.

The Power of Documentation

Even if you're a single-member LLC and it feels a bit silly, get into the habit of documenting major business decisions. This doesn’t have to be some stuffy, formal affair. Keeping a simple log, often called "meeting minutes," is one of the most powerful ways to strengthen your corporate veil.

Decided to take out a loan for a new roof? Write it down. Documenting decisions to buy another property or distribute profits to yourself shows you are operating as a distinct business entity, not just a personal piggy bank. Trust me, if your liability protection is ever challenged in court, these records are worth their weight in gold.

Strengthening Your Asset Protection Shield

Your LLC is your primary legal shield, but it shouldn't be your only one. Reinforce it with the right insurance. Your old homeowner's policy just won't cut it anymore—that property is now owned by a business.

You absolutely need a landlord insurance policy held in the LLC's name. These policies are designed specifically for the unique risks of rental properties, covering things like tenant injuries, loss of rental income, and property damage.

For an extra layer of peace of mind, look into an umbrella policy. This kicks in once the limits of your primary landlord policy are maxed out, giving you a much higher ceiling of liability protection.

This formal structure is especially critical for the growing number of "accidental landlords." With projections showing that 22% of landlords in 2025 will be accidental, and another 16% will be converting their primary homes into rentals, an LLC provides a clear framework. It helps turn a potentially overwhelming situation into a professional, well-managed business. You can dive deeper into the rental housing market on RealPage.com.

Tax Advantages and Diligent Record-Keeping

One of the best perks of an LLC is its pass-through taxation. By default, the company's profits and losses "pass through" directly to your personal tax return. This structure helps you avoid the double taxation that corporations get hit with and makes tax season a lot simpler.

But to really capitalize on these benefits, you have to keep clean books. This is non-negotiable. Run every single dollar of income and every expense through your dedicated LLC bank account. Keep every receipt. This creates a clean, auditable trail that makes deducting expenses like repairs, insurance, and mortgage interest both straightforward and defensible if the IRS ever comes knocking. We also have a guide on creating a solid property management agreement, which is a key document to have in your records.

Ultimately, consistent maintenance isn't just about tedious compliance work. It's about making your investment more profitable, more secure, and less stressful for years to come.

Questions I Hear All the Time About Rental Property LLCs

Stepping into the world of LLCs for your rentals is a big move, and it's only natural to have a bunch of questions. Honestly, it’s smart to get clear on the details before you dive in. I've pulled together some of the most common questions and sticking points I've heard from fellow investors over the years.

Think of this as your practical FAQ, tackling the real-world scenarios you’re actually going to face.

Can I Just Put All My Properties Into One LLC?

Yes, you absolutely can, and a lot of investors start out this way. The main draw is simplicity—you’ve got one set of books, one bank account, and just one annual report to file. It makes managing a small portfolio feel a lot less like drowning in paperwork.

But that convenience has a serious trade-off. Let's say you put five properties into a single LLC. If a tenant has a nasty slip-and-fall at Property A and decides to sue, the assets of Properties B, C, D, and E are all on the table. A single lawsuit could threaten the equity you've painstakingly built across your entire portfolio inside that LLC.

For maximum asset protection, the gold standard is creating a separate LLC for each individual property. This strategy compartmentalizes risk, ensuring that a problem at one rental can never infect the others.

Now, a popular middle-ground strategy I often see is grouping properties. You might put two similar single-family homes in one LLC and a higher-risk fourplex in its own separate LLC. This gives you a good balance of protection without multiplying your administrative headache.

What’s Going to Happen to My Mortgage?

This is the big one—the question that keeps nearly every property owner with a mortgage up at night. When you transfer your property's title to your new LLC, you could technically trigger the "due-on-sale" clause in your loan agreement. This scary-sounding clause gives your lender the right to demand you pay the entire loan balance immediately.

Here’s the reality: most lenders aren't looking to call a perfectly good loan. As long as you keep making your payments on time, they're usually happy. They're in the business of collecting interest, not foreclosing on performing loans, especially when it's just a transfer to a single-member LLC where you're still in full control.

The best move is always to be proactive. Pick up the phone and call your lender before you make the transfer. Explain that you're setting up an LLC for liability protection and that you will personally remain the guarantor on the loan. Some will give you written permission without a fuss, while others might ask you to refinance into a commercial loan under the LLC's name.

How Does a Rental Property LLC Change My Taxes?

Here’s some good news. One of the best things about an LLC is its tax flexibility. By default, the IRS treats a single-member LLC as a "disregarded entity." That’s just a fancy way of saying all the income and expenses from your rental property flow right onto your personal tax return (Schedule E), exactly like they would if you were a sole proprietor.

This "pass-through" taxation is a huge benefit because you avoid the double taxation that corporations get hit with. Plus, the LLC structure provides a formal, more defensible framework for all your business deductions—mortgage interest, property taxes, repairs, insurance, you name it. That can be incredibly valuable if the IRS ever comes knocking for an audit.

For multi-member LLCs, the default tax status is a partnership, which works similarly. In either case, I always tell people to have a good CPA on their team. They can help you figure out if electing for S-Corp tax status might offer some extra savings on self-employment taxes down the road.

Do I Really Need to Hire a Lawyer for This?

It's entirely possible to file the Articles of Organization yourself online, especially for a straightforward, single-member LLC. State websites have made the process pretty simple.

But hiring a lawyer is less about filling out a form and more about a strategic investment in your peace of mind. A good attorney does more than just file paperwork. They’ll help you draft an airtight Operating Agreement that’s actually tailored to your situation, guide you through the tricky parts like dealing with that mortgage transfer, and help you structure a multi-member LLC correctly from the start. A little money spent on professional advice upfront can save you from a catastrophic—and far more expensive—mistake later on.

At Keshman Property Management, we get the importance of a solid business structure because we're landlords, too. Our 20 years of hands-on experience helps owners like you build gratifying and profitable rental businesses. Learn more about our transparent, owner-focused services at mypropertymanaged.com.