What is landlord liability insurance: Essential Guide for Property Owners

- Sarah Porter

- Jan 24

- 14 min read

Updated: Jan 28

Let's get straight to it: what exactly is landlord liability insurance? Think of it as your financial backstop for the "what ifs" that keep property owners up at night. It's a specific type of coverage designed to protect you from the financial fallout of lawsuits if someone gets hurt on your property or if their belongings are damaged due to your oversight.

This is a crucial distinction from your standard homeowner's policy, which typically won't cover incidents related to rental activities. Landlord liability insurance is the specialized tool that steps in to handle legal bills, medical expenses, and potential settlements that could otherwise put your entire investment portfolio at risk.

Unpacking Your Financial First Responder

It helps to view your rental property as a business. And like any business, it comes with inherent risks that can lead to major financial headaches. Landlord liability insurance specifically addresses the human side of these risks—the slips, trips, and disputes that can quickly escalate into legal battles.

While a broader landlord insurance policy often combines liability with property damage coverage (for the building itself), the liability portion is what truly shields your personal assets from lawsuits. It's the part of your policy that activates when a tenant, their guest, or even a mail carrier claims you are legally responsible for an accident.

The Core Purpose of Liability Coverage

At its core, this insurance is built to defend you against two primary financial threats stemming from your role as a landlord:

Bodily Injury Claims: This is the big one. It covers medical costs and legal fees if someone is injured on your property and claims it was due to your negligence—think a loose handrail on a staircase or an icy patch of sidewalk you forgot to salt.

Property Damage Claims: This comes into play if your actions (or inaction) cause damage to someone else's property. A classic example is a slow leak from a pipe you were told about but didn't fix, which ends up destroying a tenant's high-end computer and furniture.

To give you a quick overview, here are the core protections in a nutshell:

Landlord Liability Insurance At A Glance

Coverage Area | What It Protects You From |

|---|---|

Medical Payments | A visitor's medical bills from an injury on your property, regardless of fault. |

Legal Defense Costs | Attorney fees, court costs, and other legal expenses to defend you against a lawsuit. |

Judgments & Settlements | The final amount you're ordered to pay if you're found liable for an incident. |

Pain and Suffering | Compensation for non-physical harm awarded in a lawsuit, such as emotional distress. |

This table shows how a single policy can address multiple layers of financial risk, from immediate medical needs to long-term legal battles.

A single liability lawsuit can be financially catastrophic. While these claims are less common than a broken appliance, they can result in massive payouts. Jury verdicts for serious negligence can easily top $1 million.

And remember, this coverage isn't just about paying the final bill if you lose a lawsuit. It also covers the incredibly expensive journey of getting to that point. It pays for your legal defense, including lawyers' fees and court costs, even if the claim is eventually thrown out. Without insurance, you’d be funding that fight entirely on your own, draining your resources long before a verdict is ever reached.

What Landlord Liability Insurance Actually Covers

It’s easy to think of insurance as a "financial shield," but what exactly does that shield block? In simple terms, landlord liability insurance jumps into action the moment someone accuses you of being legally responsible—or negligent—for something that happened on your rental property. It’s the policy that deals with the fallout when an unfortunate accident escalates into a lawsuit.

And this isn't just about covering a final payout if you lose in court. Your policy is designed to fund your entire legal defense from the get-go. The cost of hiring a lawyer, investigating the claim, and just navigating the legal system can be staggering, even if you’re eventually cleared of any wrongdoing.

Bodily Injury Claims

The most frequent and often most expensive claims come from bodily injury. This is when a tenant, a guest, or even a mail carrier gets hurt on your property, and you’re blamed for it. This part of your policy is built to handle the financial consequences when your oversight or failure to maintain the property is linked to the accident.

Think about these common scenarios:

A Slip and Fall: Your tenant takes a tumble on an icy patch of the driveway you forgot to salt, breaking their wrist. Suddenly, you're looking at their medical bills and lost wages.

A Faulty Handrail: A guest visiting your tenant leans on a wobbly handrail and falls down the stairs, resulting in a serious injury and an inevitable lawsuit.

A Cracked Sidewalk: A delivery driver trips over a badly cracked sidewalk on your property line, injuring their ankle and looking to you for compensation.

In every one of these situations, your landlord liability coverage would be what you lean on to cover everything from medical bills to the hefty legal fees.

The global landlord insurance market was valued at a massive $21,030 million back in 2023, which really shows how essential it is for property owners everywhere. Experts predict that market will swell to $38.58 billion by 2033, proving this coverage is a non-negotiable part of any serious real estate investment strategy. You can find more details about these market trends and what they mean for landlords.

Property Damage and Legal Defense

Beyond someone getting hurt, your policy also covers you if your negligence causes damage to someone else’s property. For example, if you knew about a dead tree on your rental property and a branch finally snaps off, crushing your tenant’s car, your liability insurance could pay for the vehicle repairs.

When you boil it down, your policy is there to shoulder three main financial burdens:

Medical Bills: It pays for the immediate and ongoing medical care for people injured on your property because of an issue you should have addressed.

Legal Defense Costs: It covers your lawyer's fees, court costs, and all the other expenses that come with defending yourself in a lawsuit.

Settlements and Judgments: If you’re found legally responsible, the policy pays the damages awarded by the court, right up to your coverage limit. This is what keeps your personal savings, home, and other assets safe.

Common Exclusions Your Policy Likely Will Not Cover

Knowing what your landlord liability insurance covers is only half the story. The other, arguably more important, half is understanding what it doesn't cover.

It’s easy to get a false sense of security, thinking your policy is a catch-all safety net. But every insurance policy has its limits, and misunderstanding those boundaries can leave you dangerously exposed right when you thought you were protected.

Think of it like a warranty on a new car. It covers unexpected mechanical failures, but it's not going to pay for oil changes, new tires, or damage you cause by driving recklessly. Your insurance works the same way—it's there for unforeseen accidents, not predictable problems or intentional acts.

Let's walk through the big-ticket items that your standard policy will almost certainly exclude.

Intentional Acts and Property Neglect

This one is pretty straightforward: insurance won't protect you from deliberate, wrongful, or illegal acts. If you get frustrated and change the locks on a tenant illegally, your liability policy won't cover the resulting lawsuit. It’s designed to be a shield against accidents and honest mistakes, not a get-out-of-jail-free card for bad behavior.

Another major exclusion is any problem that stems from neglect. Your policy is not a maintenance savings account.

Key Takeaway: An insurer operates on the assumption that you are a responsible property owner. If a tenant gets hurt because of a rickety staircase you’ve ignored for months, the insurance company will likely deny the claim. Why? Because the incident was preventable, not accidental.

Staying on top of your duties is non-negotiable. To get a better handle on this, check out our guide on landlord responsibilities for repairs to see how preventative maintenance is your best first defense.

Gaps in Coverage You Need to Fill

Beyond outright neglect, there are specific types of risk that standard liability policies just aren't built to handle. For these, you'll need to look at separate, specialized policies to be fully protected.

Here are the most common gaps you'll find:

Tenant's Personal Property: This is a huge point of confusion for new landlords. To be crystal clear: your insurance covers your liability and your building. It never covers your tenant's furniture, electronics, clothing, or other personal belongings. If a pipe bursts and floods their apartment, their losses are on them. This is exactly why smart landlords require every tenant to carry their own renters insurance.

Natural Disasters: Don't assume you're covered for every act of God. Standard policies almost universally exclude damage from floods, earthquakes, and sinkholes. If you own property in an area where these are a real threat, you absolutely need to purchase separate flood or earthquake insurance.

Your Personal Property: If you keep your own things at the rental—think lawnmowers, tools, or extra building materials—they probably aren't covered. Your landlord policy is for the structure itself, not the personal items you happen to store there, unless you add a special add-on, called an endorsement, to your policy.

Understanding Policy Costs And Coverage Limits

Choosing the right landlord liability insurance is a classic balancing act. You need enough coverage to truly protect your assets, but you don't want to hemorrhage cash on a premium that's overkill for your situation. It's about finding that sweet spot where you can sleep at night, knowing you're protected from a worst-case scenario.

First, let's talk about coverage limits. This is simply the maximum amount your insurance company will pay out if a claim is filed against you. Policies typically range from $300,000 to $1 million.

It can be tempting to go for a lower limit to save a few bucks on the premium, but that can be a dangerously shortsighted move. Imagine a tenant wins a lawsuit for $750,000, but your policy only covers up to $500,000. You’re now on the hook, personally, for that $250,000 difference. That’s the kind of financial hit that can wipe out a portfolio.

For most landlords, a $1 million liability limit is a solid, responsible starting point. This level of coverage is generally enough to handle the hefty legal fees, medical bills, and potential settlements that come with a serious lawsuit, creating a strong financial firewall around your assets.

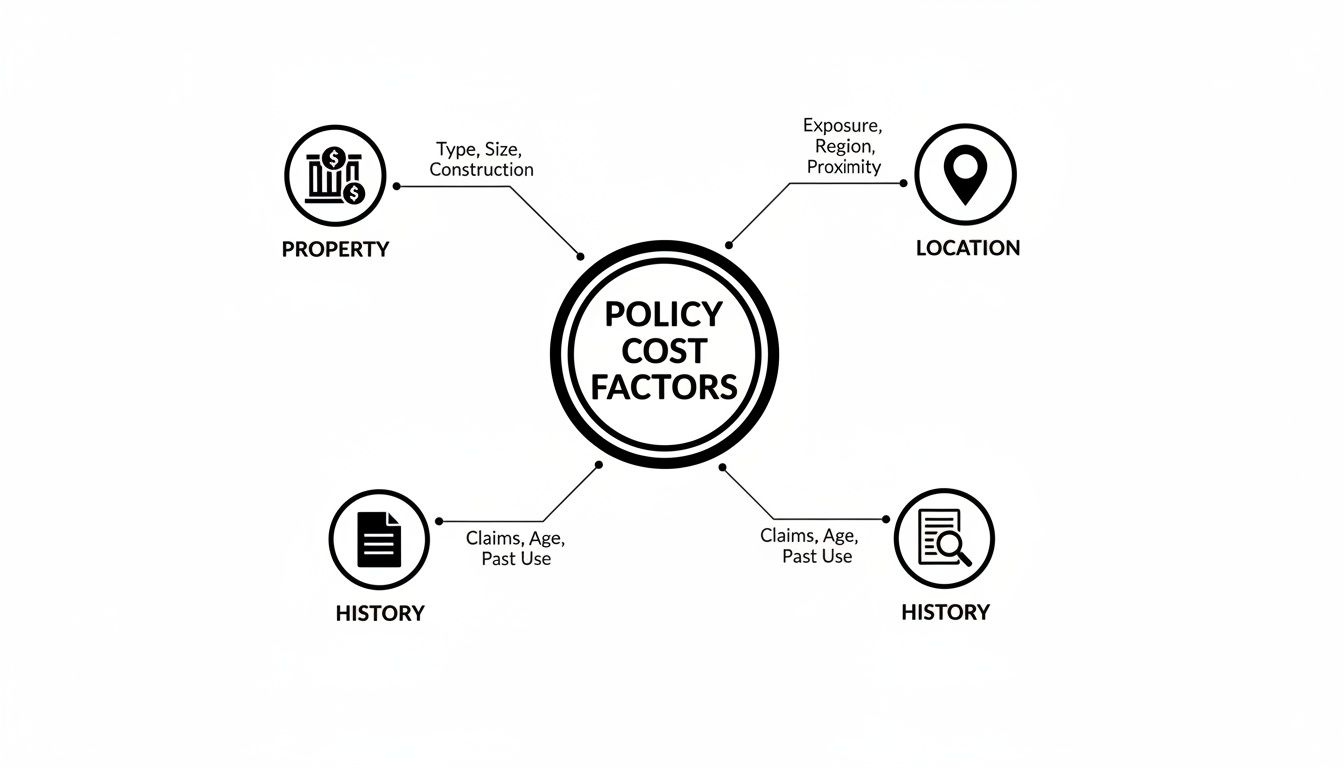

Key Factors That Determine Your Premium

Insurance companies aren't just guessing when they quote you a price. Their calculations are based on a careful risk assessment of your specific property. If you know what they're looking for, you can get a better handle on your potential costs—and maybe even find ways to reduce them.

Here’s what they’re looking at:

Property Location: Where your property is located matters—a lot. Premiums can swing wildly from one state or city to another. A rental in an area with higher crime statistics or a history of natural disasters will almost always cost more to insure.

Property Type and Age: Insuring a new, single-family home is usually cheaper than covering an older, four-plex apartment building. Older buildings can have hidden risks like aging electrical systems, while multi-unit properties mean more tenants, which naturally increases the potential for a claim.

Safety and Security Features: Insurers love to see that you’re being proactive about safety. Things like security cameras, centrally-monitored smoke detectors, fire sprinklers, and sturdy deadbolt locks can often earn you a nice little discount.

Your Claims History: This one is straightforward. If you have a history of filing claims, insurance companies will see you as a higher risk and will price your policy accordingly. A clean record pays off.

It's no secret that insurance costs are climbing, but landlord policies have been hit particularly hard. Recent figures show that the average annual premium for a single-family rental is now between $1,895 and $2,100. That's a full 25% more than a standard homeowner's policy for a similar house. The numbers get even bigger for multifamily properties.

At the end of the day, your goal is to have enough coverage to protect your entire net worth. A great way to get a feel for the market is to look at a detailed landlord insurance comparison and see what different providers offer. This will help you make a smart, informed decision that fits your budget and risk tolerance, keeping your hard-earned investment safe.

Landlord Insurance Vs Homeowners Insurance Key Differences

One of the biggest—and potentially most expensive—mistakes a new landlord can make is thinking their homeowners insurance will cover a rental property. It’s like using a car meant for city streets to go off-roading; it just wasn’t built for that kind of terrain and is bound to fail when things get rough.

Homeowners and landlord policies might look similar on the surface, but they're designed for completely different scenarios and risks.

Occupancy Is The Deciding Factor

The most fundamental difference comes down to a simple question: who lives in the house?

A standard homeowners policy is written specifically for an owner-occupied property. It's built on the assumption that you, the owner, are living there. In fact, most policies have clauses that could void your coverage entirely if the insurer finds out you've been renting the property to tenants long-term without telling them.

Landlord insurance, on the other hand, is built for a business. It protects you from the unique risks that come with having tenants and generating rental income.

Crucial Distinction: A homeowners policy covers your personal liability and your personal belongings. A landlord policy covers your business liability and the physical structure you rent out to others. Trying to use homeowners insurance for a rental is a gamble that rarely ends well.

Understanding what homeowners insurance typically covers—including its common limitations—really highlights why a dedicated landlord policy is an absolute must-have.

Comparing Core Protections

The real differences pop up when you look at the specific coverages each policy provides. While both will likely cover the physical building from disasters like a fire or a storm, their liability protections are miles apart.

Landlord insurance has several key features you just won't find in a homeowners policy:

Homeowners Insurance: This is all about protecting your personal stuff—your furniture, electronics, and clothing. The liability portion covers you if a guest is injured at your home.

Landlord Insurance: This is focused on the business of being a landlord. It includes landlord liability insurance for lawsuits brought by tenants, coverage for lost rent if the property becomes uninhabitable during repairs, and protection for any property you own but the tenant uses, like kitchen appliances.

To make this clearer, let's break down how these policies stack up against a comprehensive landlord policy, which often bundles property and liability coverage together.

Comparing Insurance Policies For Property Owners

Feature | Homeowners Insurance | Landlord Liability Insurance | Comprehensive Landlord Policy |

|---|---|---|---|

Primary Purpose | Protects owner's residence & personal belongings | Protects landlord from tenant-related lawsuits | Protects rental property structure & business income |

Who It's For | Person living in their own home | Landlord needing liability-only coverage | Landlord wanting full property & liability protection |

Covers Structure | Yes | No | Yes |

Covers Liability | Personal liability (e.g., guest slips and falls) | Business liability (e.g., tenant injury claim) | Business liability (often bundled with property) |

Covers Personal Items | Yes (owner's belongings) | No | No (tenant needs their own renter's insurance) |

Loss of Use/Rent | Covers owner's temporary living costs | No | Covers lost rental income during repairs |

This table shows that each policy serves a distinct purpose. Choosing the right one isn't about which is "better," but which one correctly matches your situation as a property owner.

As you can see, insurers weigh a combination of factors to determine your policy's cost. They look at the property itself, its location and associated risks, and even your own history as a property owner to calculate your premium.

Reducing Your Risk Before A Claim Occurs

While having the right landlord liability insurance is your safety net, the best-case scenario is never having to use it. The smartest landlords move from a reactive mindset—dealing with problems as they arise—to a proactive one focused on preventing claims from happening in the first place.

Think of it as preventative medicine for your investment property. Small, consistent efforts to keep your property safe don't just protect your tenants; they protect your bottom line. It all starts with being obsessive about property upkeep and documenting everything. A quick response to a leaky faucet or a wobbly handrail isn't just good service, it’s your first line of defense against a negligence lawsuit.

Creating A Safer Environment

Your mission is to hunt down and eliminate potential hazards before anyone gets hurt. A systematic approach always beats waiting for a tenant to report a problem. You need to be on the lookout for the common trouble spots that lead to claims, especially slip-and-fall accidents, which are a landlord's nightmare.

Here are a few practical things you can start doing right away:

Regular Safety Inspections: Get in the habit of walking the property at least quarterly. Look specifically for loose railings, cracked sidewalks, poor lighting in stairwells, or anything else that looks like an accident waiting to happen. To really dial this in, check out these helpful rental property inspection tips.

Clear and Safe Walkways: Keep sidewalks, pathways, and stairs clear of debris. In the winter, this means being on top of snow and ice removal. Make sure your property has proper drainage to stop dangerous, slippery puddles from forming.

Code Compliance: You absolutely have to stay up-to-date on local and state housing codes. Things like functional smoke and carbon monoxide detectors aren't optional—they're legal requirements and critical safety devices.

A key aspect of responsible property ownership and mitigating potential liabilities is effective property management, which encompasses all operational aspects of rental properties.

At the end of the day, a well-maintained property is a safer property. Taking these proactive steps shows your insurer that you're a responsible owner, which can even help your premiums over the long haul. A great property manager can put these systems in place for you, making sure nothing ever falls through the cracks.

Your Questions, Answered

When you start digging into landlord liability insurance, a few key questions always seem to pop up, especially around things like LLCs and how much coverage is really enough. Let's tackle some of the most common ones I hear from property owners.

I Put My Property in an LLC. Do I Still Need Liability Insurance?

Yes, you absolutely do. This is a huge point of confusion for so many investors, and getting it wrong can be a catastrophic mistake.

An LLC is great for building a legal wall between your business assets and your personal assets. If someone sues the LLC, they can't come after your family home or your personal savings. But here's what the LLC doesn't do: it doesn't protect the assets inside the business.

If a tenant has a serious slip-and-fall and sues your LLC for damages, everything the business owns is fair game. That means the rental property itself, the LLC's bank account, and any other properties you've placed in that LLC are all on the line.

A simple way to think about it is this: Your LLC is the fortress wall protecting your personal life. Your liability insurance is the army defending the fortress itself. You need both to be truly secure.

Without an insurance policy, your LLC will be stuck paying for expensive lawyers and any potential settlement out of its own pocket. That's a fast track to having to sell the very asset you were trying to protect.

How Much Liability Coverage Is Enough?

There's no single magic number, but a great rule of thumb is to have enough liability coverage to protect your entire net worth. For most landlords, a policy with a $1 million limit is a responsible and common starting place.

But you really need to tailor this to your specific situation. Think about:

The total value of all your assets (both personal and business).

How many rental units you own—more doors mean more potential risk.

The type of properties you have and their unique risks.

If you have a growing portfolio or substantial personal assets, getting an umbrella policy is one of the smartest, most cost-effective moves you can make. For a surprisingly small premium, it kicks in after your primary landlord policy is exhausted, adding millions in extra protection.

Can I Make My Tenants Get Renters Insurance?

Not only can you, but you should. Requiring tenants to carry renters insurance isn't just a good idea; it's a standard practice for savvy landlords and is a key clause in any well-written lease today.

A renter's policy does two crucial things for you. First, it covers their personal property, which your policy never will. Second, and more importantly, it includes liability coverage.

Imagine your tenant accidentally starts a kitchen fire that causes significant damage to your building. Their renters liability insurance would be the first line of defense to pay for those repairs. This can prevent you from having to file a claim on your own policy, which helps keep your premiums from skyrocketing. It's a simple, effective way to create a shared sense of responsibility.

Putting all these best practices into place—from drafting airtight leases to performing regular safety checks—is exactly where having a professional on your team pays off. Keshman Property Management helps owners implement these strategies to protect their investments, minimize liability, and ensure their properties are running smoothly. Find out how we can help you by visiting our website at https://mypropertymanaged.com.

Comments