How to finance rental property: 7 proven strategies to start

- Sarah Porter

- Dec 3, 2025

- 16 min read

Updated: Dec 7, 2025

Securing the right financing is your first real hurdle in real estate investing. It's more than just a loan; it's the foundation of your entire deal. You're typically looking at a down payment of 20-25%, with the rest coming from a bank, a private lender, or sometimes even the seller. The best path forward really hinges on your personal financial situation, the property you're eyeing, and how fast you need to get to the closing table.

Your Starting Point for Financing Investment Properties

Before you even think about talking to a lender, you’ve got to get your house in order—your financial house, that is. This prep work is what separates seasoned investors from the hopefuls. It’s not just about finding a good deal; it’s about making yourself an investor that lenders are eager to back.

Think of it as building your investor resume. Lenders are in the business of managing risk, and they need to be convinced you can pay them back. A well-prepared investor presents a clear, compelling case that minimizes their risk and highlights the property's potential.

Define Your Investment Strategy

Your financing journey really starts with a clear vision. What are you trying to accomplish? Are you playing the long game, banking on appreciation in an up-and-coming neighborhood? Or is your primary goal to generate as much monthly cash flow as possible right now?

The answers to those questions will dictate everything. A "buy and hold" strategy for a stable duplex, for example, pairs perfectly with a traditional 30-year mortgage. On the other hand, if you're planning a "fix and flip," you’ll need something much faster and more flexible, like a hard money loan that can cover both the purchase and the rehab costs.

A well-defined strategy isn't just for your benefit; it’s a crucial part of your pitch to lenders. It proves you've done the homework and have a solid plan to make money, which builds a ton of confidence.

Strengthen Your Financial Position

Next up: a deep dive into your personal finances. Lenders will put your financial life under a microscope, so you want to make sure everything looks pristine. This comes down to a few key actions.

Boost Your Credit Score: This number is your financial report card. A score north of 740 is the magic number that unlocks the best interest rates and loan terms. Get to work paying down credit card balances and disputing any errors on your report months before you start applying.

Organize Your Documentation: Lenders love paperwork. Start a folder—digital or physical—and begin collecting everything now. You'll need at least two years of tax returns, recent pay stubs, bank statements, and a detailed breakdown of all your assets and liabilities.

Build Your Cash Reserves: This is a big one. Lenders need to see you have more than just the down payment. They want proof of cash reserves, usually enough to cover 3-6 months of the property's total expenses (mortgage, taxes, and insurance). This "rainy day" fund shows them you can handle a vacancy or a surprise repair without missing a payment.

Getting these pieces in place transforms you from just another applicant into a serious, bankable investor. It makes the whole application process smoother and shows any lender you’re a low-risk partner. Plus, a strong financial footing is essential for your own peace of mind, as it helps you truly understand what is cash flow in real estate and how it works, ensuring your investment starts off on the right foot.

Getting the Money: A Look at Your Core Financing Options

When you start looking to finance a rental property, you'll quickly discover it’s a whole different ballgame than getting a mortgage for your own home. Lenders see investment properties as a business, plain and simple. That means the rules, the requirements, and the types of loans on the table are completely different.

Figuring out these core options is your first real step toward building a successful real estate portfolio. Each financing path has its own purpose. One might be perfect for a stable, long-term rental, while another is built for speed and short-term projects. Your job is to match the right tool to the right deal.

The Workhorse: Conventional Investment Property Loans

For most new investors, the journey starts with a conventional loan from a traditional bank or mortgage lender. Think of this as the bread-and-butter of real estate financing. It feels a lot like the mortgage on your primary residence, but there are a few key differences you absolutely need to know.

Lenders see more risk in an investment property. It makes sense, right? If you hit a rough patch financially, you’re more likely to miss a payment on a rental before you let your own home go. To balance out that risk, they tighten the screws.

Bigger Down Payment: Forget about 3% down. Expect to bring at least 20-25% to the table.

Higher Credit Score: You'll typically need a credit score of 620 just to get in the door, but the best rates are reserved for scores north of 740.

Tighter DTI Ratio: Lenders will comb through your Debt-to-Income ratio to make sure you can comfortably handle another mortgage payment.

Serious Cash Reserves: You must prove you have enough cash left over after closing. We're talking 3-6 months worth of the property's total monthly payment (principal, interest, taxes, and insurance) sitting in your bank account.

This is the go-to option for buy-and-hold investors who want a stable, long-term loan—usually a 15 or 30-year fixed-rate mortgage.

Scaling Up with Portfolio Loans

Once you have a few properties under your belt, juggling multiple conventional loans gets old, fast. This is where portfolio loans become a game-changer. These are typically offered by smaller community banks and credit unions that don't sell their loans to big players like Fannie Mae or Freddie Mac. They keep the loan "in-house" on their own portfolio.

This gives them a ton of flexibility. A portfolio lender is often more interested in your track record as an investor and the health of your entire real estate portfolio than just your personal DTI on paper. They might even offer a single blanket loan that covers several of your properties at once, which simplifies your life and makes it easier to tap into your equity.

Portfolio loans are all about relationships. Building a solid connection with a local banker who gets your investment strategy can be one of the most valuable assets you’ll ever have.

When You Need Speed: Hard Money Loans

What happens when you find a killer deal that needs to close in ten days? A conventional lender will just laugh you out of their office. This is precisely when hard money loans shine. These are short-term, asset-based loans from private individuals or companies.

Frankly, they care a lot more about the property's value than your personal credit score. The loan is "hard-secured" by the real estate itself. This makes them perfect for fix-and-flip investors or anyone who needs to move lightning-fast to lock down a deal before the competition.

But that speed and convenience don’t come cheap:

High-Interest Rates: You could be looking at rates from 8% to 15%, sometimes even higher.

Upfront Points: Expect to pay 1-5 points at closing (one point equals 1% of the loan amount).

Short Timelines: These aren't 30-year mortgages. The term is usually just 6-24 months, giving you just enough time to renovate and then either sell or refinance into a long-term loan.

Hard money makes sense only when the potential profit from the deal is big enough to swallow the high cost of borrowing.

Tapping into Your Home Equity (HELOC)

One of the most powerful financing tools you have might be sitting right under your own roof. A Home Equity Line of Credit (HELOC) lets you borrow against the equity you've built up in your primary residence. It works like a credit card—you get a set credit limit and can draw funds as you need them, paying interest only on the amount you’ve used.

A HELOC is a fantastic way to come up with the down payment for a rental. Let's say you have a $150,000 HELOC. You could pull out $50,000 to use as a 25% down payment on a $200,000 rental, and then get a conventional loan for the other $150,000. This strategy lets you acquire new properties without needing to have huge piles of cash sitting around.

This creative approach reflects a larger trend where both traditional and alternative capital are shaping real estate investing. In fact, the global real estate market saw direct investment hit US$213 billion in just one recent quarter, a jump of 17% year-over-year. The U.S. is leading that charge. This market resilience, fueled by a structural housing shortage and affordability challenges, makes rental properties an incredibly attractive asset. You can dig deeper into these global real estate investment trends on JLL.com.

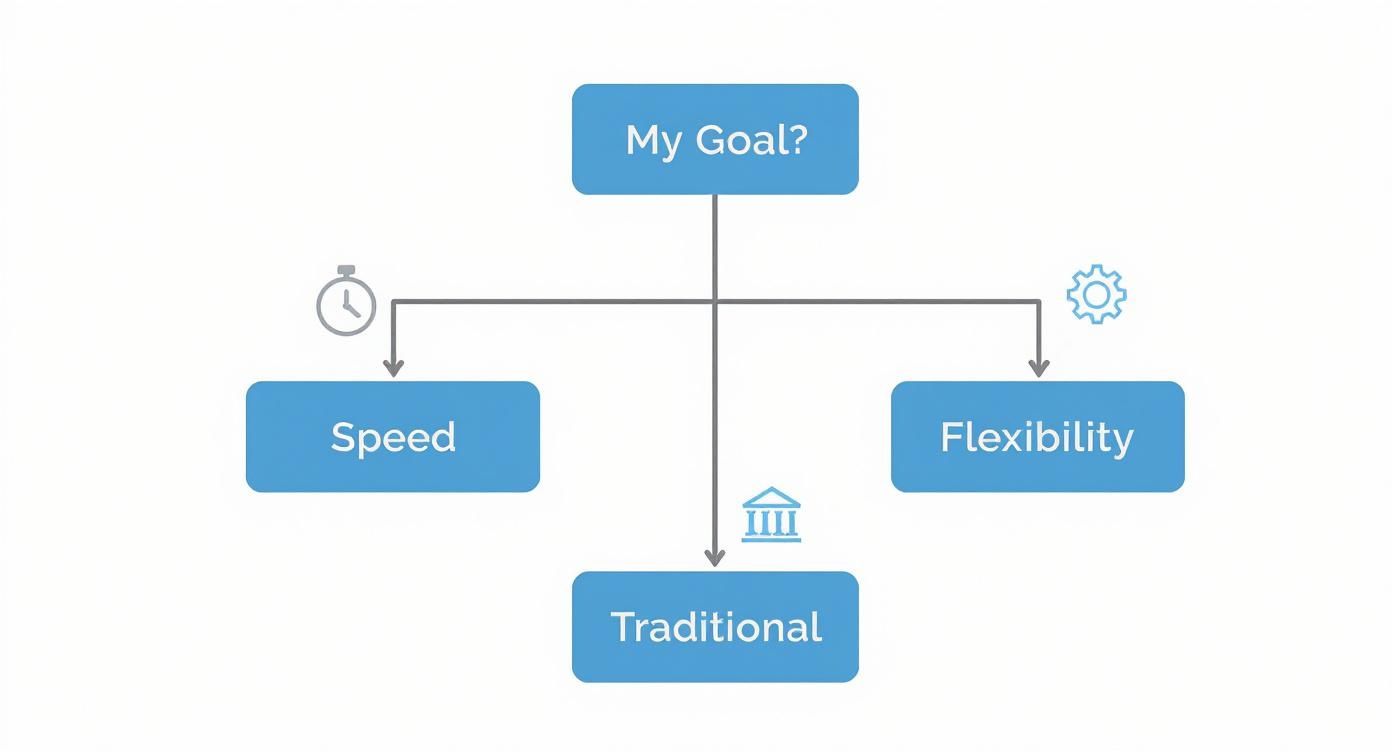

How Lenders Will Qualify Your Deal

Getting a loan for an investment property is a different ballgame than financing your own home. It’s not just about a good credit score and a down payment. Lenders are digging into the deal from every angle to protect their investment, and if you understand what they’re looking for, you’re already ahead.

At the end of the day, they’re really asking two simple questions: can you afford this loan, and can the property afford this loan?

How they answer that question splits the underwriting process into two main paths. One is the traditional approach, which is all about your personal income. The other is a more modern, asset-based method that’s become a go-to for serious investors. Knowing which path your deal is likely to follow will save you a ton of time and help you find the right lender from the get-go.

This graphic gives you a quick visual. If you need to move fast, asset-based or flexible financing is your friend. If you have time on your side and pristine personal financials, the traditional route is often more straightforward.

Your Personal Finances Under the Microscope

When you go for a conventional loan, the spotlight is squarely on you, the borrower. Lenders want to see a rock-solid financial history and feel confident you can handle another mortgage payment without breaking a sweat.

The number one metric they use to figure this out is your Debt-to-Income (DTI) ratio.

DTI is just a simple percentage showing how much of your gross monthly income is already spoken for by debt. They’ll add up all your monthly payments—your primary mortgage, car loans, student loans, credit card minimums—and divide that by your total pre-tax monthly income.

For an investment property, most lenders are looking for a DTI ratio of 43% or lower. This means that all your debts, including the new mortgage on the rental, can’t eat up more than 43% of your income.

If your DTI is a little high, you’ve got two options: make more money or owe less money. The fastest fix is often to knock out some debt. Paying off a high-balance credit card or a small personal loan before you apply can make a world of difference. Sometimes, that’s all it takes to get an approval.

When the Property Pays Its Own Way

But what if your DTI is already stretched thin? Or maybe you're self-employed, and proving your income on paper is a nightmare. This is where asset-based lending changes the game, especially for investors trying to scale their portfolio.

Instead of qualifying you, the lender qualifies the property.

The key metric here is the Debt Service Coverage Ratio (DSCR), which basically asks if the property’s income can cover its own mortgage. This has become the most common type of asset-based loan.

The formula is pretty simple:

DSCR = Net Operating Income (NOI) / Total Debt Service

Net Operating Income (NOI) is your rental income minus operating expenses (like taxes, insurance, and maintenance—but not the mortgage itself).

Total Debt Service is the full monthly mortgage payment (principal, interest, taxes, and insurance).

Lenders will typically want to see a DSCR of 1.25 or higher. In plain English, this means the property needs to bring in 25% more income than what’s needed to pay its mortgage. A DSCR of 1.0 means the property just breaks even, which is way too risky for a lender. That 1.25+ ratio shows there's a healthy cash-flow cushion to handle vacancies or a broken water heater.

The Importance of Cash Reserves

Whether you’re going the DTI or DSCR route, every lender is going to want to see cash in the bank. And no, this isn't your down payment. These are cash reserves—liquid funds you’ll have left after closing.

Lenders need to know you can float the mortgage for a few months if your tenant moves out or a big repair pops up. For investment properties, the standard ask is 3 to 6 months of the property’s full monthly payment (PITI) held in reserve.

So, if the total monthly mortgage payment is $2,000, you’ll need to show you have between $6,000 and $12,000 sitting in a checking or savings account. This little detail can make or break a deal, so don't overlook it.

Creative Financing Strategies That Actually Work

Let's be honest, not every great real estate deal fits neatly into the conventional lending box. Some of the most profitable opportunities I've seen were the ones that required thinking differently. This is where creative financing becomes your secret weapon, letting you snap up properties when a traditional loan just isn't in the cards.

These aren't just last-ditch efforts, either. For many seasoned investors, creative strategies are the preferred path. Why? More flexible terms and much, much faster closing times. Getting a handle on these techniques can open doors that are completely shut to other buyers.

Negotiating Directly with the Owner

One of the most powerful tools in the investor's belt is seller financing, sometimes called owner financing. It's exactly what it sounds like: the property owner acts as your bank. You skip the mortgage lender entirely and make your monthly payments directly to the seller.

This can be a brilliant win-win scenario. The seller gets a steady income stream and often offloads their property faster, while you can negotiate much more flexible terms. Here's what's usually on the table for discussion:

Down Payment: You can often get away with less than the rigid 20-25% a bank demands.

Interest Rate: This is completely negotiable and can land above or below current market rates.

Loan Term: A common approach is a short-term loan, like a 5-year balloon, which gives you time to improve the property and refinance into a traditional mortgage later.

Treat this just like any other loan—no handshake deals. Get a real estate attorney to draft a promissory note and a deed of trust to make it official. Beyond just this basic setup, it's a good idea to explore owner financing options to see what other structures might work for your deal.

The Power of Partnerships and Joint Ventures

You don't have to fly solo. Bringing on a partner is an incredibly effective way to get a deal done, especially when you're starting out. A classic joint venture involves one partner (the "boots on the ground") finding the deal and managing the project, while the other partner brings the capital for the down payment and closing costs.

For this to work, you absolutely need crystal-clear legal documentation from day one. A solid partnership agreement is non-negotiable and must spell out:

Roles and Responsibilities: Who is doing what? Get specific to avoid future headaches.

Equity Splits: How is ownership divided? A 50/50 split is common, but it can also reflect different contributions of time and money.

Profit Distribution: How will you split the monthly cash flow and the profits when you eventually sell?

Exit Strategy: What happens if one of you wants out? Plan the breakup before you even get started.

This approach lets you tap into other people's money and skills, helping you scale your portfolio far faster than you could on your own.

Tapping into Private Money

Private money is another fantastic alternative to the big banks. This means borrowing from individuals in your network—think friends, family, or other local investors—instead of a financial institution. These lenders are typically looking for better returns than a savings account can offer and are willing to fund real estate deals they believe in.

To land a private money loan, you need a killer pitch. Don't just show up with an idea; present them with a professional deal summary. Lay out the numbers clearly: purchase price, renovation budget, projected rental income, and the After Repair Value (ARV). You need to show them exactly how and when they'll get their money back, plus a healthy return for taking a chance on you.

The global housing shortage has completely reshaped how rental properties are financed. New research highlights a need for 6.5 million more housing units in key developed markets, which is fueling a massive trend toward renting. With over 80% of households in these areas struggling with affordability, the demand for rentals—and the financing to buy them—is stronger than ever. This structural undersupply makes rental property a defensive investment, attracting both traditional banks and creative sources of capital. You can read more about these global housing trends on Hines.com.

Preparing Your Application and Analyzing a Deal

Getting a lender to say "yes" to your rental property loan comes down to two things: a stellar application and a deal that makes financial sense. Lenders need to feel confident in both you as a borrower and the property as a performing asset before they'll cut a check.

But more importantly, a bulletproof deal analysis is what protects you. It's the only real way to know if a potential investment will build wealth or become a money pit. Honing your ability to run the numbers is a non-negotiable skill for any serious investor.

Assembling a Bulletproof Loan Application

Walking into a lender's office—or more likely, sending them an email—with a complete, perfectly organized application package is a huge power move. It saves everyone time and immediately signals that you're a professional who respects their process.

I always tell new investors to start gathering these documents before they even have a property in mind. Think of it as building your financial resume. Get everything scanned and saved in a dedicated folder on your computer so you can fire it off at a moment's notice when a great deal pops up.

Here’s a practical checklist of what you'll almost always need:

Tax Returns: Your last two years of personal tax returns, including all schedules.

Proof of Income: The most recent 30 days of pay stubs, plus W-2s or 1099s for the last two years.

Asset Statements: Two to three months of statements for all bank accounts (checking, savings) and any investment accounts (brokerage, retirement). Lenders want to see your reserves.

Identification: A crystal-clear copy of your driver’s license and Social Security card.

If you own other properties or are investing through a business, the list expands slightly.

For an LLC: Have your Articles of Organization, Operating Agreement, and Certificate of Good Standing ready. Using an LLC is a smart move for liability protection.

For Existing Rentals: You'll need copies of current lease agreements and a "schedule of real estate owned"—a simple spreadsheet listing each property's address, market value, mortgage balance, and rental income.

I can't stress this enough: having every single one of these documents ready to go before you apply is one of the easiest ways to get a lender on your side. They spend half their day chasing down missing paperwork. When you deliver a perfect package upfront, you become their favorite type of client.

How to Run the Numbers on a Rental Property

Once your personal finances are buttoned up, the spotlight turns to the property itself. This is where you put on your analyst hat and rigorously vet the deal. Gut feelings and back-of-the-napkin math have no place here.

Your goal is to accurately project the property's financial performance. A few key metrics tell the whole story: Cash Flow, Cash-on-Cash Return, and overall Return on Investment (ROI). These are the numbers that separate a hobby from a business.

Let's walk through a tangible example. Say you're looking at a duplex listed for $250,000. The plan is to put 25% down ($62,500) and finance the remaining $187,500.

Sample Rental Property Deal Analysis

The table below breaks down the essential calculations step-by-step. This is the exact process I follow to evaluate every potential deal, making sure no detail is overlooked.

Metric | Calculation | Example Value |

|---|---|---|

Gross Potential Rent | Rent per unit x Number of units | $2,800 / mo ($1,400 x 2) |

Vacancy (5%) | Gross Rent x 0.05 | ($140 / mo) |

Property Taxes | Annual tax bill / 12 | ($250 / mo) |

Insurance | Annual premium / 12 | ($100 / mo) |

Repairs & Maintenance (6%) | Gross Rent x 0.06 | ($168 / mo) |

Property Management (9%) | Gross Rent x 0.09 | ($252 / mo) |

Total Operating Expenses | Sum of all expenses above | ($910 / mo) |

Net Operating Income (NOI) | Gross Rent - Operating Expenses | $1,890 / mo |

Mortgage (P&I) | Loan payment at 7% on $187.5K | ($1,247 / mo) |

Monthly Cash Flow | NOI - Mortgage Payment | $643 / mo |

Annual Cash Flow | Monthly Cash Flow x 12 | $7,716 / yr |

Cash-on-Cash Return | (Annual Cash Flow / Down Payment) x 100 | 12.3% |

In this scenario, the deal generates a 12.3% Cash-on-Cash Return, which is a fantastic result for a buy-and-hold rental. These are the kinds of numbers that get lenders excited and help you build a profitable portfolio.

For a quicker way to compare multiple properties at a high level, you can also use simpler metrics. Our guide on what is Gross Rent Multiplier in real estate investing is a great resource for that. This rigorous analysis ensures you’re not just buying a property, but a high-performing asset.

Common Questions About Financing Rental Property

Once you start seriously looking at rental properties, the questions really start to pile up. Financing, in particular, can feel like a maze of jargon and hidden rules. Let’s clear the air and tackle some of the most frequent questions I hear from investors.

How Much Down Payment Do I Really Need?

Forget what you know about buying your own home. For a conventional investment property loan, you’re almost always looking at a down payment of at least 20-25%. Lenders see investment properties as a bigger risk, so they want more skin in the game from you.

Of course, there are workarounds. If you're buying a multi-unit and plan to live in one of the units (a strategy called "house hacking"), you might qualify for an FHA loan with a much smaller down payment. But for a straightforward rental, planning for a quarter of the purchase price is the way to go.

My Advice: Aim for a 25% down payment. It’s the magic number that satisfies most traditional lenders and shows them you're a serious, well-capitalized investor.

Can I Still Get a Loan with a Lower Credit Score?

A lower credit score makes things tougher, but it absolutely does not shut the door on financing. For a conventional loan, most lenders want to see a minimum score of 620. To get the best rates and terms, you’ll really want to be north of 740.

What if you're not there yet? Don't panic. This is where alternative financing shines.

Hard & Private Money Lenders: These lenders care far more about the deal than your FICO score. If the property has strong potential to turn a profit, they’re interested.

Seller Financing: This is a fantastic option where you negotiate terms directly with the owner. They might be more flexible on credit if you can offer them other favorable terms.

A less-than-perfect credit score just means you need to get more creative with your financing strategy.

What Is a DSCR Loan and When Should I Use It?

DSCR stands for Debt Service Coverage Ratio, and these loans are a game-changer for serious investors. Instead of poring over your personal pay stubs and tax returns, the lender qualifies the property itself.

Here's how it works: The lender looks at the property's Net Operating Income (NOI) and compares it to the total mortgage payment. As long as the property generates enough cash flow to cover its own debt—lenders typically require a DSCR of 1.25 or higher—you can get the loan.

This is the perfect tool for self-employed investors or anyone whose personal debt-to-income ratio is getting tight. It allows you to scale your portfolio based on the strength of your deals, not your W-2 income.

Should I Put My Rental Property in an LLC?

For most investors, the answer is a resounding yes. Putting your property into a Limited Liability Company (LLC) is one of the smartest ways to protect yourself. It creates a legal wall between your personal assets (like your home and savings) and your business assets. If a tenant ever sues, they sue the LLC, not you.

An LLC also makes your bookkeeping much cleaner and can open up some valuable tax advantages. For a deeper dive on this, check out our guide on a landlord’s guide to rental property tax deductions.

One crucial heads-up: If you already have a mortgage on the property, you can't just transfer it into an LLC without talking to your lender. Doing so could trigger a "due-on-sale" clause, which means you'd have to pay off the entire loan balance immediately. Always, always talk to your lender and a real estate attorney first.

Securing the financing is just the first step. Managing the property day-to-day is where the real work begins. At Keshman Property Management, we handle all the operational details so you can stay focused on finding that next great deal. Find out more about how we can help at https://mypropertymanaged.com.

Comments