How to Manage Rental Properties Like a Pro

- Sarah Porter

- Sep 6, 2025

- 16 min read

Managing a rental property really boils down to four key areas: finding great tenants, keeping the property in top shape, managing the money, and staying on the right side of the law. If you can build solid systems for each of these, you’ll have a profitable investment on your hands, not a constant headache. It’s about shifting from just reacting to problems to proactively running a business.

Your Blueprint for Profitable Property Management

Many first-time landlords fall into the trap of thinking their only job is to cash a rent check every month. But here’s the reality: when you learn how to manage rental properties the right way, you’re running a small business. You have customers (your tenants), an asset to protect (your property), and serious financial and legal obligations. Getting into that business mindset from day one is the most critical thing you can do.

This means you have to stop improvising. A proactive approach is all about creating repeatable processes for every part of the rental cycle. You need a go-to plan for marketing a vacancy, a strict, non-negotiable checklist for screening every applicant, and a clear workflow for how you handle maintenance calls. Without these systems in place, you’re just winging it, and that’s a recipe for expensive mistakes and high turnover.

The Core Management Phases

Your entire management strategy should be built around a few core operational phases. Each one logically follows the next, and if you get them right, you create a stable, predictable tenancy. Skimp on any one of these, and the whole thing can fall apart.

To give you a clearer picture, here’s a breakdown of the essential stages you’ll be cycling through as a landlord.

Essential Property Management Phases at a Glance

Phase | Key Objective | Core Activities |

|---|---|---|

Tenant Acquisition | Attract and secure a reliable, qualified tenant for your property. | Marketing vacancies, conducting showings, screening applicants, executing the lease. |

Property Maintenance | Preserve the asset's value and ensure a safe, habitable home for tenants. | Handling repair requests, performing preventative maintenance, managing vendor relationships. |

Financial Administration | Ensure profitability and maintain accurate financial records. | Collecting rent, tracking all income and expenses, budgeting for future repairs. |

Legal & Compliance | Operate within all applicable laws to avoid fines and lawsuits. | Understanding landlord-tenant laws, adhering to the Fair Housing Act, managing evictions. |

Think of these phases as the foundation of your rental business. Each one is a critical building block for a successful, long-term investment.

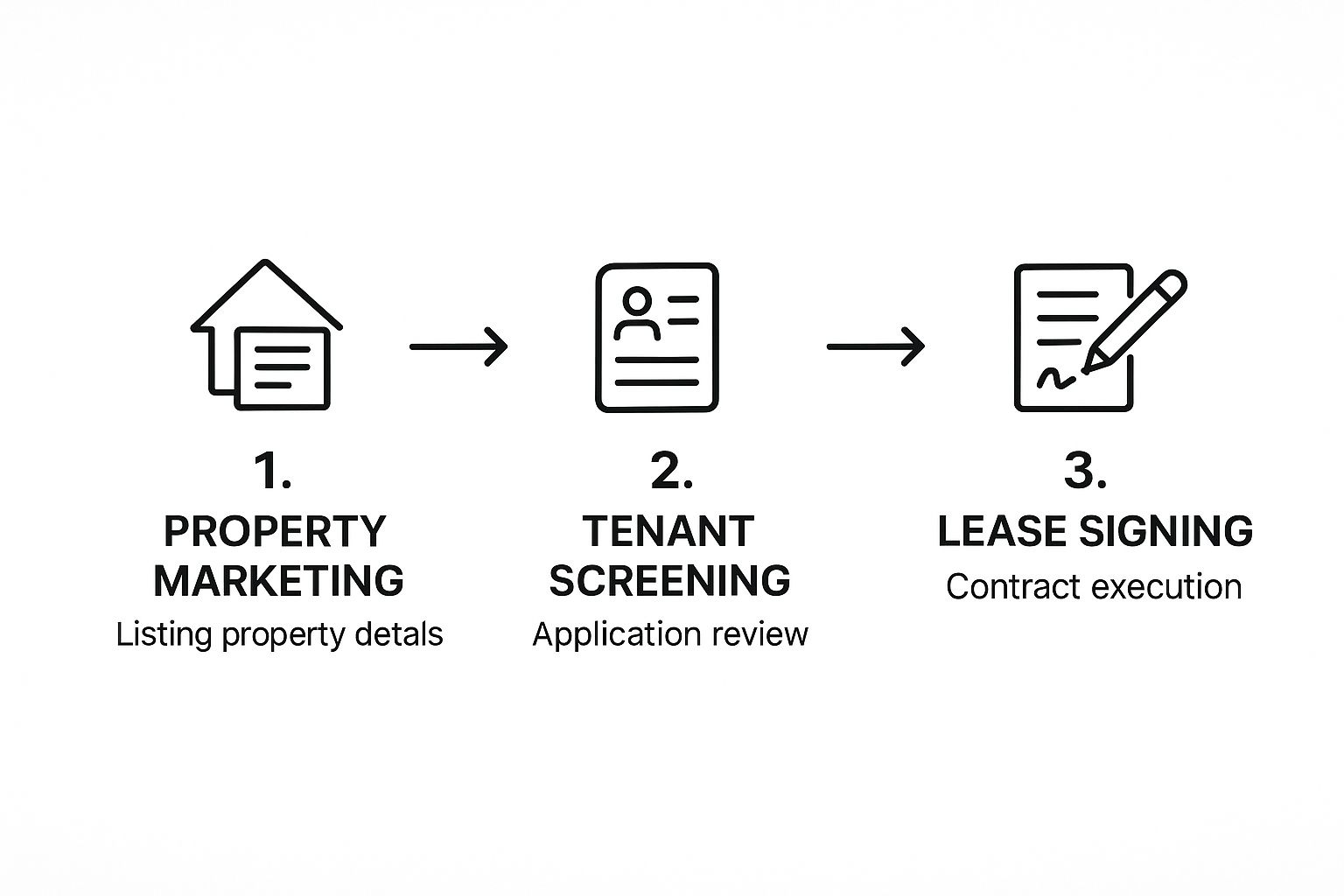

The image below zeroes in on that crucial first phase—getting the right person in the door.

As you can see, it’s a funnel. You start with marketing to a wide audience and then systematically narrow down the pool through your screening process until you’re left with the best possible applicants. Once you get these foundational pieces locked down, you're setting yourself up for a much smoother and more profitable experience as a landlord.

Finding and Keeping Five-Star Tenants

Let's get one thing straight: the single biggest factor in your success as a landlord isn't the property itself. It's the people you put inside it. A great tenant is worth their weight in gold—they pay on time, communicate clearly, and treat your property like it's their own. This makes your job infinitely easier.

But finding these five-star renters doesn't happen by accident. The process starts long before you ever see a single application. It all begins with your marketing.

Crafting a Magnetic Rental Listing

How you present your property sets the stage for the kind of applicants you’ll get. A well-crafted rental listing is your first and most effective filter.

Your ad needs to do more than just rattle off the number of bedrooms and baths. It needs to sell a lifestyle and speak directly to the kind of responsible, long-term tenant you're looking for. High-quality, bright photos are completely non-negotiable, but the description is where you can really set yourself apart.

Instead of just saying, "Spacious living room," try something like, "Sun-drenched living room with huge windows, perfect for your collection of houseplants." You're painting a picture and helping potential renters imagine themselves living there. Be upfront about the property's features and crystal clear about your expectations, like your pet policy or smoking rules.

Here are a few things every great listing should have:

A descriptive headline that grabs attention by highlighting a key feature (e.g., "Charming Bungalow with Fenced Yard, Steps from Downtown").

High-resolution photos showing every room and the exterior from multiple angles.

A detailed list of amenities, from the in-unit dishwasher to community perks.

Clear terms on rent, security deposit, and the lease duration.

This level of detail not only attracts serious inquiries but also weeds out those for whom the property isn't a good fit, saving everyone a ton of time.

Designing a Bulletproof Screening Process

Once the applications start rolling in, a consistent and thorough screening process is your best defense against future headaches. Every single applicant over the age of 18 must go through the exact same steps, without exception. This isn't just good practice; it's essential for complying with Fair Housing laws and ensuring you're making a decision based on objective criteria.

The application form is your foundation for gathering the information you need to verify.

Landlord Tip: Don't stop at the application. Once you receive it, do a quick online search for the applicant. Social media profiles or public records can sometimes reveal red flags that a standard background check might miss. Remember, consistency is your key to a fair and legal process.

Your screening checklist should methodically verify the following for every applicant:

Credit History: Look for a pattern of responsibility, not just the raw score. A low score from old medical debt tells a very different story than recent, unpaid credit card bills or utility collections.

Criminal Background: Focus on convictions that could genuinely pose a risk to the property or the community. A minor issue from a decade ago is less concerning than recent, serious offenses.

Rental History: This is arguably the most important check. Make it a rule to contact the previous two landlords, not just the current one. A current landlord might give a glowing review just to get a problem tenant out of their building.

Income Verification: The industry standard is a gross monthly income of at least three times the monthly rent. Always get copies of recent pay stubs or an offer letter, and follow up with a call to the employer to confirm they actually work there.

When you call previous landlords, ask open-ended questions. Instead of, "Did they pay rent on time?" ask, "Could you describe their payment habits?" The single most revealing question you can ask is, "Would you rent to them again?" Their answer—and any hesitation behind it—will tell you almost everything you need to know.

Building these systems takes effort upfront, but it’s the most reliable path to managing your properties for long-term stability and profit. For more strategies on this, be sure to check out our complete guide on how to attract and retain quality tenants.

Crafting a Lease That Protects Your Investment

So, you've found the perfect tenant. That's a huge win, but the work isn't over. Now comes the single most important document in your landlord toolkit: the lease agreement.

Think of the lease as the official rulebook for the tenancy. It's not just a formality to get a signature on; it’s your first line of defense and the legal foundation that will guide you through any potential bumps in the road.

A generic, one-page template you find online is asking for trouble. To truly protect your investment, you need a lease that is specific, thorough, and tailored to your property and your local laws. Getting this right from the beginning will save you from so many headaches later on.

Beyond the Basics: Essential Lease Clauses

Sure, every lease covers the basics—rent amount, due date, and the length of the tenancy. But a truly ironclad agreement anticipates the "what-ifs" that seasoned landlords know all too well. Leaving things vague is an open invitation for misunderstandings and conflict.

Your lease is your chance to clearly outline your policies before they become problems.

Here are a few clauses that I consider absolutely non-negotiable:

Security Deposit Rules: Be crystal clear. State the exact amount, where the funds will be held (check your state laws on this!), and the specific conditions for making deductions. It helps to give examples of "normal wear and tear" versus actual "damage."

Late Fee Policies: Don't just say "late fees apply." Specify the exact fee, the grace period (if you offer one), and the date the fee is triggered. This consistency is crucial for encouraging on-time payments.

Maintenance Responsibilities: Who handles what? Put it in writing. Define the tenant's duties (like replacing lightbulbs or smoke alarm batteries) versus your responsibilities (like HVAC servicing or major appliance repair). This one clause can prevent countless disputes.

Rules of Conduct: Be specific. Address noise levels and quiet hours, rules about altering the property (no painting without permission!), and guest policies. How long can a guest stay before they're considered an unauthorized resident? Spell it out.

And if you allow pets, a detailed pet addendum is a must. It should cover the specific type and size of the animal, require vaccination records, and detail any pet-related fees or deposits.

Aligning Your Lease With Local Laws

This is where many landlords, new and old, get into hot water. Landlord-tenant laws can change dramatically from one state to the next—even from one city to another. A clause that’s standard practice in one place could be completely illegal just a few miles away.

For example, many states cap the amount you can charge for a security deposit, often limiting it to one or two months' rent. Others have strict rules about how much notice you must give before entering the property. Guessing is not a strategy.

A classic mistake is mishandling the security deposit at move-out. Many states require you to send an itemized list of deductions to the former tenant within a specific timeframe, often 30 days. If you miss that deadline, you could be forced to return the entire deposit, even if the property was damaged.

Before you have a tenant sign anything, you have to do your homework on your local and state laws. Your state government’s website and local landlord associations are great places to start. For those looking for a solid framework, you can download our rental lease agreement template to see how a comprehensive agreement is structured.

The Move-In Process: Setting the Standard

The lease is signed, but your job isn't done. The move-in process is where you set the tone for the entire tenancy and establish a clear baseline for the property's condition.

The most critical piece of this process is the move-in inspection report. Don't just hand the keys over. Walk through the entire property with your new tenant and meticulously document its condition—every room, every appliance, every scuff on the wall. Take tons of photos and videos.

Have both you and the tenant sign the completed report. Now you have an agreed-upon record of the property's state from day one. This single document is your best defense against security deposit disputes when they eventually move out. It turns a potential "he said, she said" argument into a simple, fact-based comparison.

Implementing a Proactive Maintenance System

One of the biggest blunders I see landlords make is waiting for something to break before they fix it. This "if it ain't broke, don't fix it" mindset is a recipe for disaster. It doesn't just lead to panicked, late-night calls about a busted water heater; it's a surefire way to drain your bank account over time.

Think of it this way: proactive maintenance is about preventing fires, not just putting them out. A smart strategy protects your investment, sidesteps those eye-watering emergency repair bills, and, maybe most importantly, keeps your tenants happy. When people see you're actively caring for the property, they tend to treat it better and are far more likely to stick around and renew their lease.

Building Your Maintenance Playbook

The heart of any good proactive system is a schedule. Don't rely on your memory—it will fail you. Instead, create seasonal checklists that spell out exactly what needs to be done and when. This simple habit is how you catch small issues before they snowball into thousand-dollar problems.

Your checklists need to cover the whole property, inside and out. A fall checklist, for instance, is your best defense against the harsh realities of winter.

Sample Fall Maintenance Checklist:

Gutters and Downspouts: Get them cleared of all leaves and gunk. This prevents ice dams, which can lead to serious roof and water damage.

HVAC System: Have a pro service the furnace. This ensures it's running efficiently and safely before the first cold snap hits.

Plumbing: Take a look at any exposed pipes in unheated spots like crawl spaces or basements. Insulate them now to keep them from freezing and bursting later.

Safety Devices: Test every single smoke and carbon monoxide detector. And change the batteries, even if you think they’re still good.

By turning these tasks into a system, you build a predictable and manageable workflow. You’re no longer guessing what to do; you’re following a plan.

Assembling Your Team of Trusted Contractors

Let's be real: you can't be an expert in everything. A huge part of managing property well is building a go-to list of reliable, licensed, and insured contractors before an emergency strikes. You do not want to be frantically searching for a plumber at 2 a.m. while your tenant’s apartment floods.

Start by asking for referrals from other landlords or real estate agents in your area. Once you have a shortlist, do your homework.

Verify their license and insurance. This is non-negotiable.

Check online reviews and ask for a few references you can actually call.

Give them a small, non-urgent job to see how they perform. Are they responsive? Is the work high-quality?

Having a trusted electrician, plumber, and HVAC tech on speed dial transforms a potential catastrophe into a manageable inconvenience. This network isn't just a contact list; it's one of your most valuable business assets.

Streamlining Tenant Repair Requests

You need a crystal-clear process for tenants to submit repair requests. If it’s confusing, tenants will either give up on reporting small issues (which then become huge ones) or they'll blow up your phone with calls and texts at all hours.

Set up one primary channel for all non-emergency requests. This could be a dedicated email address or, even better, a tenant portal through property management software. The key is to create a documented paper trail for every single issue.

By creating efficient systems, you professionalize your operation. The property management market is growing rapidly, with projections in the United States showing an expansion from $81.52 billion in 2025 to $98.88 billion by 2029. This growth highlights the increasing reliance on streamlined processes for maintenance, tenant communication, and financial tracking to manage properties effectively. Discover more insights about the expanding property management sector and how professionalism pays off.

When a request lands in your inbox, respond right away. Even a simple, "Got it, thanks! I'll have an update for you by tomorrow," goes a long way. Good communication makes tenants feel heard and respected, which is a massive piece of the puzzle for keeping them long-term.

Getting a Handle on Your Rental Property Finances

Let's be honest: true success in rental investing comes down to treating it like a real business. And at the heart of any good business is rock-solid financial management. When you get this part right, you gain incredible clarity on your profitability and make tax season a whole lot less painful.

Trying to manage your finances with a "shoebox" method is a surefire way to lose money and create a ton of stress. A disciplined approach is the only way to accurately track performance, budget for what’s ahead, and make smart decisions for your portfolio.

First Things First: Separate Your Finances

Before you do anything else, open a dedicated bank account for your rental business. I can't stress this enough—do not skip this step. Mixing your personal and rental funds creates a bookkeeping nightmare and makes it almost impossible to know if your property is actually making money.

This simple act of separation is your foundation. All rent checks get deposited here, and every single property-related expense gets paid from this account. This creates a clean financial trail that will be your best friend come tax time.

A separate account makes tracking cash flow a breeze. You can see your income versus your expenses at a glance without having to dig through your personal grocery bills or coffee receipts. This is what separates amateur landlords from serious investors.

Find the Right Tools for the Job

Once your accounts are separate, you need a system to track every dollar. A simple spreadsheet might work when you have just one property, but it becomes a tangled mess and a recipe for errors as you start to grow.

This is where modern property management software really shines. These platforms are built for landlords, automating so many of the tedious tasks you’d otherwise be stuck doing by hand.

Think about what they can do for you:

Automated Rent Collection: Tenants can set up recurring payments, which is a huge help in cutting down on late payments.

Expense Tracking: You can categorize every expense—from a minor plumbing repair to your property taxes—often just by snapping a picture of a receipt with your phone.

Financial Reporting: Need a profit and loss statement? You can generate one, along with other key reports, in just a few clicks.

Investing in good software pays for itself in the time you save and the mistakes you avoid. You get a real-time snapshot of your financial health, which is crucial for making informed decisions. For a deeper look at getting organized, check out our guide to bookkeeping for rental properties made simple.

Master Your Income and Expenses

Knowing exactly where your money is going is the key to maximizing your profit. This isn’t just about collecting rent on time; it’s about meticulously tracking and categorizing every single expense.

Proper expense categorization is more than just good housekeeping—it directly impacts how much you owe in taxes. So many landlords leave money on the table because they just don't keep good records.

Your goal should be to run your rental with the financial precision of a well-managed business. Every expense you track correctly is a potential tax deduction. This turns a tedious chore into a direct boost to your bottom line. Don't let poor record-keeping cost you.

Start by tracking these common expense categories:

Repairs and Maintenance: The cost of fixing a leaky faucet, patching drywall, or servicing the HVAC system.

Property Taxes: Your annual tax bills from the local municipality.

Insurance: Premiums for your landlord insurance policy.

Mortgage Interest: The interest portion of your loan payment is a major deduction.

Professional Fees: Money paid to property managers, accountants, or lawyers.

Plan for the Big-Ticket Items

Finally, a truly smart financial system accounts for the major expenses that are bound to come up. That roof won’t last forever, and every water heater has a limited lifespan. These large, predictable expenses are called capital expenditures (CapEx).

A good rule of thumb is to set aside 1-3% of the property's value each year for future CapEx. So, for a $300,000 property, that means putting $3,000 to $9,000 into a separate savings account annually.

This isn’t an optional step; it’s a critical part of a long-term strategy. By building a dedicated CapEx fund, you ensure a major repair doesn’t become a financial emergency that wipes out your cash flow for months. It’s the ultimate proactive move for any savvy investor.

Navigating Landlord Laws and Fair Housing

Let’s be honest: landlord-tenant law can feel like a minefield. But understanding your legal responsibilities isn't just about avoiding trouble—it’s the bedrock of a stable, professional rental business. Getting this right protects your investment, but more importantly, it builds the kind of trust that leads to long-term, respectful tenancies.

When your tenants know you operate by the book, it sets a completely different tone for your relationship. It’s all about fairness, safety, and keeping communication clear from day one.

The Fair Housing Act is Non-Negotiable

At the top of the list is the federal Fair Housing Act. This law is crystal clear: you cannot refuse to rent to someone, or treat them differently, based on their membership in a protected class.

These protected classes cover:

Race or color

Religion

National origin

Sex (this includes gender identity and sexual orientation)

Familial status (like having kids under 18)

Disability

What does this mean in practice? Your entire process—from how you word your rental ads to the questions you ask on an application—must be based on objective business criteria. Think credit scores, income verification, and rental history. That's it.

Even something that seems innocent can get you into hot water. For instance, advertising a one-bedroom apartment as "perfect for a single professional" could be seen as discouraging families with children, which is a violation.

Expert Tip: Consistency is your best defense. Create a standard screening process with written criteria and apply it identically to every single applicant. No exceptions. This simple practice is your strongest shield against accusations of discrimination.

Key Legal Duties You Can't Ignore

Beyond fair housing, a whole host of other rules govern your day-to-day operations. While the specifics can vary wildly from state to state (and even city to city), a few key obligations are nearly universal.

Handling Security Deposits: There are strict rules for this. Most jurisdictions cap the amount you can collect—often it's one or two months' rent. They also dictate how you must store the money, sometimes requiring a separate, interest-bearing account. Critically, there's always a firm deadline for returning the deposit after a tenant moves out. Miss it by a single day, and you could be on the hook for returning the entire amount, even if there were legitimate damages.

Right to Entry: You own the property, but your tenant has the right to privacy. You can't just drop by whenever you want. For non-emergencies like routine inspections or repairs, you almost always have to provide "reasonable notice." While the definition can vary, 24 hours' written notice is the standard in most places. Always check your local laws to be sure.

The Eviction Process: This is one area where you absolutely cannot freelance. Removing a tenant is a formal legal procedure that must be followed to the letter. You can't just change the locks, shut off the power, or toss their belongings on the curb—that's called a "self-help" eviction, and it’s illegal. You must serve the correct legal notices and get a court order to proceed. Trying to take a shortcut here will only lead to serious legal and financial penalties.

Got Questions About Managing Your Rentals?

Whether you're just starting out or have been a landlord for years, the same tricky questions tend to pop up. Let's tackle some of the most common ones with practical, no-nonsense answers.

How Much Cash Should I Keep on Hand for Repairs?

Nothing sinks a rental's profitability faster than an unexpected major expense you're not ready for. The key is to plan for it.

A good starting point is the 1% rule. The idea is to save 1% of your property's total value each year just for maintenance. So, for a $300,000 property, you'd aim to put aside $3,000 a year, which breaks down to a manageable $250 per month.

Another tried-and-true method is the 50% rule. This one is a bit more comprehensive. It suggests that about half of your gross rental income will go toward operating expenses—everything but the mortgage. This includes:

Maintenance and repairs

Property taxes

Insurance

Vacancy costs

Using this as a benchmark gives you a much more realistic picture of your actual cash flow and helps you build a solid financial cushion.

What's the Best Way to Handle Late Rent Payments?

When rent is late, your response needs to be firm, fair, and immediate. Procrastination only makes the problem worse.

The moment the grace period ends, enforce the late fee specified in your lease. No exceptions. This isn't about being mean; it's about running a business and showing you're serious about the terms of the agreement.

Your next step is to send a formal written notice. This document should clearly state the overdue amount and the late fee that's been applied. If this becomes a pattern, you're dealing with a breach of the lease. At that point, you have to follow your local landlord-tenant laws to the letter, which might mean starting the formal eviction process.

Always remember to provide proper written notice before entering a property for an inspection, as required by state law. While a quick drive-by can give you a peek at the exterior, any interior check requires formal, documented communication with your tenant.

Can I Just Say "No Pets" in My Rental?

For the most part, yes, you can have a no-pet policy. But there's a huge exception you need to know about: assistance animals.

Under the Fair Housing Act, you are legally required to provide reasonable accommodation for both service animals and emotional support animals. This means you can't deny their tenancy or charge a pet deposit or "pet rent" for them.

Juggling maintenance, finances, and legal rules can feel like a full-time job. With over 20 years of experience, Keshman Property Management can handle all of it for you, making ownership more profitable and a lot less stressful. Learn more about our property management services.

Comments