Your Guide to the Rental Income Form 1099 for Landlords

- Sarah Porter

- Dec 13, 2025

- 16 min read

Updated: Dec 20, 2025

Let's get one of the biggest landlord myths out of the way first: there’s no such thing as a dedicated "rental income form 1099." That's right. Instead, you might find a Form 1099-K, 1099-MISC, or even a 1099-NEC in your mailbox, depending on how your tenants pay you.

Think of these forms as informational memos sent to both you and the IRS. They create a paper trail, showing how much money you received from a specific source throughout the year.

Cracking the Code on Rental Income Form 1099

When a Form 1099 shows up, don't panic. It’s not a tax bill you need to pay, nor is it a form you have to fill out and send back. It's simply a heads-up from the entity that paid you—whether that’s a property manager or a payment platform—confirming the total amount they sent your way.

Your only job is to make sure the income you report on your tax return lines up with what the IRS has been told. Understanding which form you're holding is the key to getting it right.

Different Forms for Different Payment Streams

Each type of 1099 has a specific trigger. As a property owner, you could easily receive more than one, especially if you use different rent collection methods or have commercial tenants. The trick is knowing why a particular form was issued, so you can account for that income properly.

Let's break down the main 1099s landlords should have on their radar:

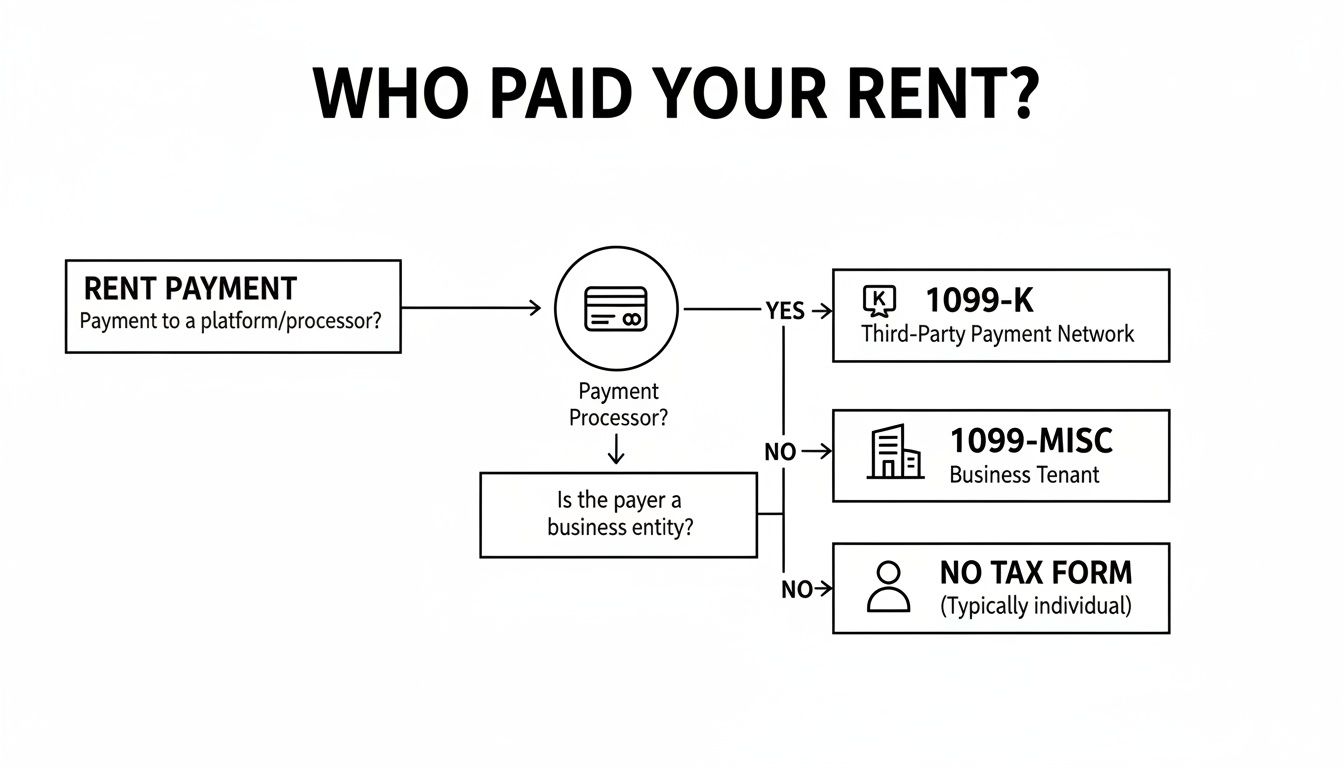

Form 1099-K: This form comes from third-party payment processors. If your tenants pay rent through platforms like Zillow, PayPal, or Venmo, the processor will send you a 1099-K once your total payments cross a certain threshold for the year.

Form 1099-MISC: The "Miscellaneous Income" form is the one you'll typically see for direct rent payments. A classic example is when you rent a property to a business; they are required to issue you a 1099-MISC for the rent they paid you directly.

Form 1099-NEC: This one is for "Nonemployee Compensation." While you’re far more likely to be the one issuing this form to contractors you hire (like a plumber or painter), a property manager might send you one under certain, less common arrangements.

To help you keep these straight, here's a quick summary.

Quick Guide to Common 1099 Forms for Landlords

This table breaks down the essential 1099 forms you might encounter as a rental property owner, clarifying who sends them and for what reason.

Form Type | Who Issues It | Reason for Issuance |

|---|---|---|

1099-K | Third-Party Payment Processors (e.g., PayPal, Stripe, Zelle) | To report rent payments processed through their platform. |

1099-MISC | Business Tenants or Property Managers | To report direct rent payments you received. |

1099-NEC | Property Managers (less common) or businesses you consult for | To report compensation for services, not typically for rent. |

This overview should give you a clearer picture of what to expect in your mailbox come tax season.

The decision tree below visualizes exactly how the payment source dictates the type of 1099 you might get. It’s a great way to see the logic in action.

As you can see, if you're using a payment app, you're in 1099-K territory. If a business tenant is paying you directly, expect a 1099-MISC.

The most critical takeaway is that a 1099 shows your gross rental income, not your final taxable profit. It's the starting line for your tax calculations, before you subtract all your valuable deductions.

Form 1099-K: The One You're Most Likely to See

In a world where almost everyone pays rent online, Form 1099-K has quickly become the most common tax form landlords run into. If you're using a third-party payment network to collect rent, you absolutely need to get familiar with this one.

Think of platforms like Zillow, Avail, PayPal, or even Venmo as your digital middlemen. They process payments from your tenants and pass the money on to you. Because they're handling these transactions, the IRS requires them to report the total amount. That report is the Form 1099-K, and a copy gets sent to you and to Uncle Sam. Using an automated rent collection service can make this whole process much smoother.

Why Did I Get a 1099-K?

You won't get a 1099-K just because a few rent payments came through an app. These platforms are only required to issue the form when your total transactions hit a certain threshold set by the IRS. For the 2023 tax year, the federal reporting threshold was $20,000 in gross payments and more than 200 transactions.

But here’s a critical heads-up: this threshold is a moving target and has been a topic of much debate and change. On top of that, several states have their own, much lower, reporting rules—some as low as just $600. This means you might get a 1099-K from a payment processor even if you’re nowhere near the federal limit.

Let me be crystal clear: whether you get a 1099-K or not, you are still legally required to report all your rental income. The form is just a reporting mechanism; it doesn't create your tax obligation.

Gross vs. Net: Don't Panic at the Big Number

The first time you open a 1099-K, you might have a moment of sheer panic. The number in Box 1a, "Gross amount of payment card/third-party network transactions," can look shockingly high. This is, without a doubt, the biggest source of confusion for landlords.

Key Takeaway: The amount on your Form 1099-K is your gross rental income. It is not your taxable profit. This number represents every dollar the platform processed for you before a single expense has been deducted.

Think of it like the total daily sales at a coffee shop. The cash register might show $2,000 in sales, but that doesn't account for the cost of coffee beans, milk, employee pay, or the shop's rent. Your rental property works the same way.

Let’s quickly look at the important parts of the form:

Box 1a: This is your gross rental income processed by the platform. It's the starting point for your tax math, not the end.

Box 3: This shows how many transactions were processed.

Boxes 5a-5l: These give you a month-by-month breakdown of the gross amount, which is incredibly useful for double-checking your own books.

Since the IRS gets a copy, they’ll be looking to see that the income you report on your tax return (on Schedule E) is at least what’s reported in Box 1a. Your job is to take that gross number and start subtracting every single legitimate business expense—repairs, mortgage interest, property taxes, insurance, you name it. This is where having immaculate records becomes your best friend.

When a 1099-MISC or 1099-NEC Comes into Play

While the 1099-K covers payments from third-party networks, two other forms—the 1099-MISC and 1099-NEC—often pop up for landlords. It's helpful to think of them as tools for different jobs, each triggered by a specific kind of payment.

Getting a handle on the difference is key. It determines whether you should be getting a tax form in the mail or if you're the one responsible for sending one out. That shift in roles is a huge part of managing your rental business the right way.

Receiving a 1099-MISC for Rents

The Form 1099-MISC (Miscellaneous Information) is the classic form for reporting rent payments, but there's a big catch: you'll almost never get one from an individual tenant. This form is typically reserved for situations where your tenant is a business.

Let's say you lease a small storefront to a local bakery or rent a condo to a corporation for a visiting executive. If that business pays you $600 or more in rent over the year, they're required to send you a Form 1099-MISC. The amount they paid you will show up in Box 1, conveniently labeled "Rents."

This is exactly why commercial landlords are so familiar with this specific rental income form 1099. The business tenant is essentially telling the IRS, "Hey, we paid this landlord this much in rent," which creates a neat paper trail for everyone.

Think of this as a one-way street. You, the landlord, are just the recipient. Your business tenant is doing the work because their rent is a deductible expense, and the 1099 is part of their proof.

If all your tenants are just regular folks or families paying you by check or Zelle, you can breathe easy. They don't have a business, so they won't be sending you a 1099-MISC.

Issuing a 1099-NEC for Services

Now, let's flip the script. The Form 1099-NEC (Nonemployee Compensation) is a form you're much more likely to send out than receive. This is your responsibility when you pay independent contractors for work done on your properties.

Think about all the people you hire to keep your rentals running smoothly. Did you pay a plumber $800 to fix a busted pipe? Or hire a painter for $2,000 to get an apartment ready for a new tenant? These folks aren't on your payroll, so you're paying them as contractors.

If you pay an unincorporated service provider $600 or more in a calendar year, you have to issue them a 1099-NEC. This applies to a wide range of professionals:

Maintenance Pros: Plumbers, electricians, and HVAC techs.

Repair Specialists: Roofers, painters, and flooring installers.

Other Service Providers: Landscapers, cleaners, and even the real estate agent you paid a commission to for finding a tenant.

Forgetting to send these can lead to IRS penalties, so keeping close track of what you pay your contractors is a non-negotiable bookkeeping task.

The Role of Your Property Manager

Here's where it can get a little tricky. If you've hired a property management company, the tax form you get from them depends entirely on how they handle the money. Their internal accounting system dictates whether you get a 1099-K or a 1099-MISC.

It usually plays out in one of two ways:

They Use a Third-Party Processor: Many modern property managers use platforms like AppFolio or Buildium to process rent. If your money flows through one of these systems, you'll likely receive a Form 1099-K from that payment processor.

They Pay You Directly: Some managers might collect rent, deposit it into their own bank account, and then cut you a check after taking out their fees and other expenses. In this scenario, they are the direct payer, so they will issue you a Form 1099-MISC for the gross rent they collected for you.

The best thing you can do is have a conversation with your property manager at the beginning of the year to ask which form to expect. Knowing ahead of time prevents headaches and ensures you don't accidentally report the same income twice.

How to Report Your 1099 Income on Your Tax Return

Getting a Form 1099-K or 1099-MISC in the mail isn't the end of the story—it's just the beginning. That form tells you the gross income figure the IRS now has on file for your rental property. Your job is to take that number and correctly report it on your tax return, which is your opportunity to tell the full story by including all your deductible expenses.

For almost every landlord out there, your primary destination is IRS Schedule E (Supplemental Income and Loss). This form is built specifically for reporting income and expenses from rental real estate. Think of it as the official ledger for your rental business, where you square up the numbers from any 1099s you received with what you actually earned and spent.

A critical goal here is to make sure the total rental income you report on Schedule E is equal to or greater than the combined totals from all your 1099s. If you report a lower amount, you're almost guaranteed to trigger an automated notice from the IRS, as their system will immediately flag the mismatch.

From Gross Income to Net Profit on Schedule E

The real power of Schedule E is in how it’s structured. You'll start by entering your gross rents on Line 3. This isn't just the amount from your 1099s; it's all the income you collected, whether it came through a payment app, a check, cash, or any other method.

Once you’ve listed your total income, you get to subtract your expenses. This is where having meticulous records throughout the year really pays off, allowing you to turn that big gross income number into a much smaller, and more accurate, taxable net profit.

The single most effective way to lower your tax bill is to claim every legitimate deduction you're entitled to. The 1099 only shows what you brought in; Schedule E is where you show what it cost to run the business.

The IRS allows for a huge range of deductions that are directly tied to managing and maintaining your rental property. Every single expense you claim chips away at your taxable income, which directly lowers the amount of tax you owe.

Maximizing Your Rental Property Deductions

This is the part that genuinely impacts your bottom line. Keeping detailed records gives you the confidence to claim all your expenses, which can add up to a substantial amount. For a deep dive into this topic, check out our complete landlord's guide to rental property tax deductions.

Here are some of the most common and valuable deductions for landlords:

Mortgage Interest: This is often one of the biggest write-offs for property owners.

Property Taxes: State and local property taxes are fully deductible.

Insurance Premiums: Landlord, homeowner's, and flood insurance policies are all deductible expenses.

Repairs and Maintenance: The cost of routine work like fixing a leaky faucet, patching drywall, or replacing a broken window can be deducted in the year it occurs.

Utilities: If you cover costs like water, gas, or electricity for your tenants, you can deduct those payments.

Professional Fees: Did you pay a property manager, accountant, or lawyer for services related to your rental? Those fees are deductible.

Depreciation: This is a powerful, non-cash deduction that lets you recover the cost of your property over its useful life.

It's also crucial to understand the tax implications of short-term rentals on Schedule E vs. Schedule C if you're in that part of the market. The rules can be quite different, so making sure your income is reported on the correct form is essential for staying compliant.

The Bigger Picture on Rental Income Reporting

Remember, the numbers you report don't exist in a vacuum—they reflect the real-world rental market. In a recent year, a staggering 85% of US landlords raised their rents in response to high demand and increasing operational costs. This trend has pushed the national median rent up by a full 32% over five years, meaning the gross income figures on 1099s and Schedule E forms are climbing for landlords everywhere.

At the end of the day, successfully reporting your 1099 income comes down to a simple formula: report all your income on Schedule E, then methodically subtract every single eligible expense. This approach not only keeps you in good standing with the IRS but also makes sure you’re maximizing the financial return on your investment.

Good Record-Keeping Is Your Best Defense

Let's be honest, meticulous records are your secret weapon against tax-time headaches and any potential questions from the IRS. While the rental income form 1099 you get shows the money coming in, it’s your records that tell the other side of the story—all the money going out.

Think of it like this: your 1099 is just the headline. Your detailed expense log provides the full story, proving every deductible cent you spent. This isn't just about stuffing receipts in a shoebox; it's a year-round business habit that helps you claim every legal deduction and keep more of your hard-earned money.

Start with a Dedicated Bank Account

The simplest and most powerful first step? Open a bank account used only for your rental business. Mixing your personal and rental finances, known as commingling funds, is the fastest way to create a bookkeeping catastrophe.

When all your rental income goes into one dedicated account and all expenses are paid from it, your bank statement essentially becomes a ready-made financial report. This clean separation makes tracking cash flow almost automatic and creates a crystal-clear audit trail if you ever need one.

Find the Right Tools for the Job

With your banking sorted, you need a system to track and categorize every transaction. This doesn't need to be overly complicated, and landlords today have some great options.

Accounting Software: Platforms like QuickBooks, Stessa, or Baselane are built with property owners in mind. They can sync with your bank account, help categorize transactions automatically, and generate reports like a profit and loss statement with just a few clicks.

Spreadsheets: If you only have one or two properties, a well-organized spreadsheet might be all you need. Just create columns for the date, property address, expense category (like repairs, insurance, or utilities), and the amount.

Whatever you choose, the key is consistency. Pick a tool you'll actually use and make a habit of updating it at least once a month. For a more detailed walkthrough, our complete guide to bookkeeping for rental property is a fantastic starting point.

Document Every Expense the Right Way

A system is only as good as the information you feed it. It's not enough to just record the dollar amount of an expense; you need to document its business purpose, too.

A receipt from Home Depot is just a piece of paper. A receipt with a handwritten note—"New faucet for 123 Main St, Unit B kitchen leak"—is audit-proof documentation.

This habit is critical for telling the difference between a simple repair and a capital improvement, which are treated very differently for tax purposes.

Repairs: These are the everyday things you do to keep the property in good working order. Fixing a leaky pipe, patching drywall, or replacing a broken doorknob all fall into this category. These expenses are 100% deductible in the year you incur them.

Capital Improvements: These are bigger projects that add significant value, extend the property's life, or adapt it for a new use. Think a full roof replacement, a complete kitchen remodel, or adding a new bathroom. You recover the cost of these over time through depreciation, not all at once.

Finally, don't overlook your mileage. Every trip you take to show a unit, meet a contractor, or collect rent is a deductible business expense. A simple app on your phone can track these miles effortlessly, potentially adding up to thousands in deductions you might otherwise miss.

Putting It All Together: Real-World Landlord Scenarios

The theory is one thing, but what happens when a 1099 actually shows up in your mailbox? Let's walk through a few common situations you might encounter. Think of these as a playbook for turning tax-time confusion into a clear plan of action.

Scenario 1: You Receive a 1099-K from Zillow

You use Zillow to collect rent for your property, and a Form 1099-K arrives showing $24,000 in gross payments. That number looks huge because it doesn't factor in your mortgage interest, property taxes, insurance, or that new water heater you had to install. So, what's next?

Your Game Plan:

Don't Panic: That $24,000 is your gross income, not your profit. The IRS knows this. It’s just the starting line for your tax calculations.

Gather Your Records: This is where good record-keeping pays off. Pull together all your expense documents for the year—receipts for repairs, your mortgage interest statement (Form 1098), property tax bills, and insurance invoices.

Fill Out Schedule E: On your tax return, you’ll report the $24,000 as your gross rental income on Schedule E. Then, you'll methodically list all those deductible expenses, which will bring that number down to your actual, much lower, net taxable income.

Scenario 2: You Get a Partial 1099-K from Venmo

You have two tenants in a duplex. One pays you $1,000 a month with a personal check, and the other pays their $1,000 through Venmo. At the end of the year, you get a 1099-K from Venmo for $12,000. How do you handle this on your tax return?

Your Game Plan:

Acknowledge All Income: The 1099-K only tells part of the story—the electronic part. You are responsible for reporting all income, no matter how it was paid.

Calculate Your Total Gross Rent: Your actual rental income for the year is $24,000 ($12,000 from checks + $12,000 from Venmo).

Report the Full Amount: On Schedule E, you must report the total $24,000 as your gross rental income. When the IRS matches its copy of the $12,000 1099-K to your return, they'll see you’ve reported that amount and more, which is exactly what they expect. No red flags here.

The core principle is simple: Your tax return must reflect all income streams. The 1099 is just one piece of the puzzle, not the whole picture. Relying solely on the forms you receive can lead to underreporting.

Scenario 3: You Have to Issue a 1099-NEC to a Roofer

A nasty storm rolls through and damages the roof of your rental. You hire an independent roofing contractor (not a big corporation) and pay them $8,000 for the repair. Since this is well over the $600 threshold for services, you need to issue them a 1099-NEC.

Your Game Plan:

Get a Form W-9 First: This is critical. Before you cut the check, have the roofer fill out and sign a Form W-9. This form gives you their legal name, address, and Taxpayer Identification Number (TIN). You can't file a 1099 without it.

Complete Form 1099-NEC: Using the information from the W-9, you'll fill out a 1099-NEC. The $8,000 you paid them goes in Box 1 for "Nonemployee Compensation."

File and Send It Out: You must send Copy B of the form to the contractor and file Copy A with the IRS by January 31 of the following year. Doing this properly documents your expense, solidifying your deduction.

Scenario 4: Your 1099-K Has the Wrong Amount

Your property manager sends you a 1099-K that says they collected $30,000, but you've tracked every payment and your records clearly show it was only $28,000. What do you do when the official form is wrong?

Your Game Plan:

Contact the Issuer Immediately: Your first call should be to the property manager or payment company that sent the form. Calmly explain the error and be ready to show them your records.

Ask for a Corrected Form: If they confirm the mistake, they can issue a corrected 1099-K. This is the ideal and cleanest solution for everyone.

Report Correctly and Explain: What if they refuse or drag their feet? You should still report the correct income ($28,000) on your Schedule E. It’s a good idea to attach a brief statement to your tax return explaining the discrepancy and why the 1099-K amount is incorrect. Having meticulous records will be your best defense if the IRS ever asks.

Got Questions About Form 1099? We've Got Answers

Even when you know the rules, real-world situations can get a little murky. Let's tackle some of the most common questions and sticking points landlords run into with Form 1099.

What if I Don't Receive a Form 1099?

This is a big one. Even if you don't get a 1099-K or 1099-MISC in the mail, you are still 100% required to report all of your rental income to the IRS.

Think of a 1099 as just a heads-up from a third party. Its absence doesn't change your fundamental responsibility as a taxpayer. You might not have received one simply because your income from that specific source didn't hit the official filing threshold, but you still need to track and report that income on your Schedule E.

Help! The Amount on My 1099-K Seems Way Too High.

Take a deep breath—this is a very common reaction, and it’s usually not an error. The figure on a Form 1099-K represents your gross rental income. It’s the total sum of money the payment platform processed for you before any of your expenses, fees, or even their own commissions were taken out.

It’s just the starting point. Your actual taxable income is that gross number minus all your legitimate business deductions—things like mortgage interest, property taxes, insurance, repairs, and maintenance.

Key Insight: Your 1099-K shows your revenue, not your profit. The entire purpose of your Schedule E is to subtract your expenses from that revenue to calculate what you actually owe tax on.

My Property Manager Sent Me a 1099. Is That Right?

Yes, that's perfectly normal. If your property manager handles rent collection, they are acting as the payer. The 1099 they send you reports the gross rent they collected on your behalf throughout the year.

You’ll take that gross income figure, report it on your Schedule E, and then list all your deductible expenses. And yes, that includes the management fees you paid to them!

I Co-Own a Property. How Does the 1099 Work?

This can get a little tricky. Usually, the Form 1099 is issued to just one person—whoever’s Social Security Number or Taxpayer ID Number is linked to the payment account. That individual is technically responsible for reporting the full amount on their tax return.

From there, you have a couple of options. The primary owner can issue a separate Form 1099-MISC to the other co-owner for their share of the income. Another common approach is for the primary owner to report the full income on their Schedule E and then subtract the co-owner's portion as a "nominee distribution," which is basically an expense line item that zeros out the portion that isn't theirs.

Navigating the tax side of rental properties can feel like a full-time job. At Keshman Property Management, we handle these financial details so you can focus on what matters: your investment's growth. With over 20 years of hands-on experience, we make owning property less daunting and more profitable. Find out more about our transparent, owner-focused approach at https://mypropertymanaged.com.

Comments