When to Sell Rental Property A Landlord's Strategic Guide

- Sarah Porter

- Jan 25

- 16 min read

Updated: Jan 28

Knowing when to sell a rental property is one of the biggest financial decisions an investor can make. It's far more than just a gut feeling or a reaction to a bad tenant. The right moment often appears when the market is hot, the property's upkeep is starting to drain your profits, or your own financial goals have changed.

It’s a strategic choice, balancing the potential for a big payday against the ongoing costs and headaches of being a landlord.

The Landlord's Crossroads: Knowing When to Sell

Every property investor eventually gets to that point where they have to ask, "Should I hold on, or is it time to cash out?" There's no single, easy answer. The key is to move past emotion and take a hard, structured look at all the moving parts.

This decision isn’t about one expensive repair or a single late rent payment. It's a calculated business move that can shape the future of your entire investment portfolio.

Thinking like a seasoned investor means looking at your property from a few different angles. It really boils down to the fundamental question posed in resources like "Is It Worth Keeping Your Wellington Property as a Rental?" The answer always lies in a mix of factors—some you can control, and some you can't.

Core Pillars of the Selling Decision

To make a smart call, you need to build a solid framework around the four pillars that hold up any good real estate investment:

Market Timing: Are you in a "seller's market"? When demand is high and inventory is low, you have the leverage to sell at a premium. Catching the market at its peak is how you maximize your return.

Property Financials: Take a close look at the numbers. Is the property still a cash-flow machine, or are rising expenses and big-ticket repairs eating away at your bottom line?

Tax Implications: Don't forget about Uncle Sam. You need to understand how capital gains tax and depreciation recapture will affect your final profit. Knowing about powerful tools like a 1031 exchange is crucial here.

Personal and Portfolio Goals: Does this specific property still fit into your bigger picture? Maybe your goal is to diversify into different assets, fund your retirement, or simply free up your time and capital for something new.

A property that was a great investment five years ago isn't automatically a great investment today. Your circumstances, the market, and the property itself are constantly changing.

Think of this guide as a practical roadmap, built from a landlord's perspective. We'll break down each of these pillars, giving you the tools to analyze your own situation with clarity. By the end, you'll be able to decide whether holding on or cashing out is the right strategic move for you.

Is the Market Right for a Profitable Sale?

Knowing when to sell your rental property feels a bit like trying to catch the perfect wave. You can sit on your board all day, but the real money is made when you see a big wave forming, paddle hard, and ride it to shore at its peak.

Sell too soon, and you leave money on the table. Sell too late, and you risk getting crushed by a market downturn. The trick is learning to spot the signs that a "seller's market" is building momentum.

A seller's market is simple supply and demand: more buyers are house-hunting than there are properties available. This imbalance puts you in the driver's seat. Homes sell quicker, bidding wars become common, and you often get offers at or above your asking price. Recognizing these conditions is the first step toward a profitable exit.

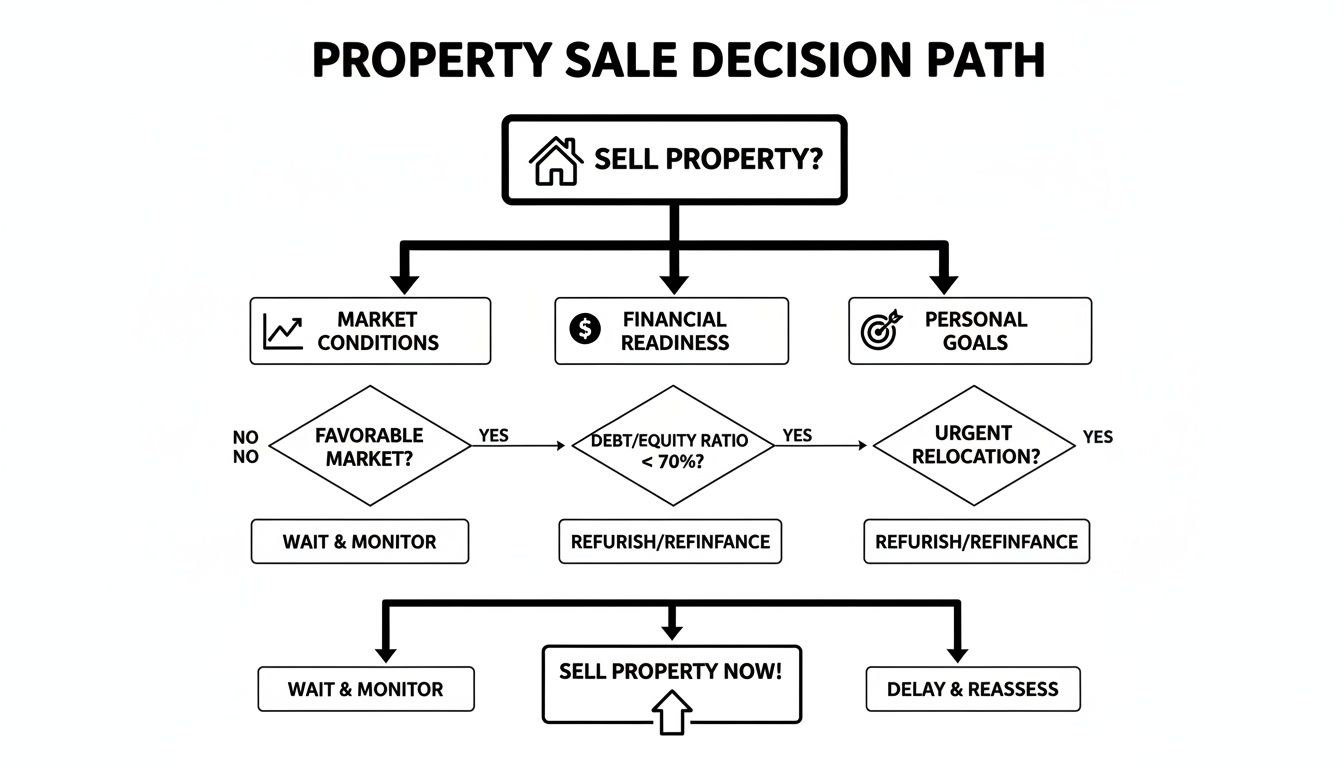

Of course, it's not just about the market. The decision has to align with your financial situation and long-term goals. This flowchart breaks down the thought process.

As you can see, the sweet spot for selling is where strong market tailwinds meet your own financial readiness and investment strategy.

Reading the Local Tea Leaves

While national headlines are interesting, real estate is a street-by-street, neighborhood-by-neighborhood game. To really nail the timing, you have to become a student of your local market. Think of yourself as a local weather forecaster, noticing the subtle shifts that signal a bigger storm of buyer activity is coming.

To help you get a clear picture, here is a quick guide to the most important market indicators.

Key Market Indicators for Selling

Indicator | Favorable Sign to Sell | What It Means for You |

|---|---|---|

Days on Market (DOM) | Consistently decreasing DOM | Homes are selling faster, meaning buyer demand is strong and your property won't sit idle. |

Sale-to-List Price Ratio | At or above 100% | Properties are selling for asking price or more, often due to bidding wars. It's a sign of intense buyer competition. |

Housing Inventory Levels | Below 4 months of supply | There are more buyers than available homes, which naturally drives up prices and gives you negotiating power. |

These metrics give you a powerful snapshot of local demand. When you see all three lining up in your favor, the market is practically shouting that it's a good time to sell.

Pro Tip: Don't just watch your own property; watch what's happening in your neighborhood. A new school, a popular grocery store, or a public transit expansion can create a micro-market boom, giving you a prime selling window even if the city-wide market is just lukewarm.

Keeping an Eye on the Bigger Picture

While local data is your primary guide, national economic trends are what create the larger market waves. Think of it this way: national trends set the ocean's tide, while local factors create the specific waves you can ride.

Things like interest rates, employment numbers, and overall economic confidence have a huge impact. For example, history shows that a great time to sell is often after a long period of appreciation, right as prices seem to be peaking. This allows you to lock in your gains before a potential correction.

Looking at recent data, the average sales price of houses sold hit $512,800 in Q2 2025, a solid jump from $502,200 in Q2 2024. When you see that kind of growth, paired with a 5.1% rise in existing home sales, it can be a strong signal that the market is hot. You can track this data yourself over at TradingEconomics.com.

By blending these big-picture economic insights with your sharp, local knowledge, you can time your sale with much greater confidence. Catching the market at the right time is crucial, but it’s only half the battle. You also need to know how to price your rental property for maximum profit to truly cash in on the opportunity.

Crunching the Numbers on Your Property's Performance

Beyond what the overall market is doing, the real decision to sell boils down to one simple question: is this specific property still pulling its weight for you? Think of it like a regular health check-up for your investment. A hot market might make everything look good on the surface, but if your property's financials are weak, you're just masking a bigger problem.

This isn't just about making sure the rent covers the mortgage each month. We need to dig deeper to see your true return on investment and pinpoint that moment when rising costs start eating away at your profits.

To do this right, you need to conduct a thorough real estate investment property analysis to get a clear picture of your property's financial health.

Key Metrics That Tell the Real Story

To get to the truth, you have to look past the surface-level numbers. There are three core metrics that will reveal if your property is still a star player or if it’s time to trade it.

Cash Flow: This is your bread and butter. It's the cash you have left over after paying every single bill—mortgage, property taxes, insurance, maintenance, management fees, you name it. If your cash flow is consistently negative or shrinking year after year, that's a huge red flag waving right in your face.

Cash-on-Cash Return: This metric gets straight to the point: how hard is your actual invested cash working for you? It measures your annual pre-tax cash flow against the total cash you put into the deal. If this percentage is dropping, it’s a sign that your money could probably be earning a better return somewhere else.

Capitalization (Cap) Rate: By dividing your Net Operating Income (NOI) by the property's current market value, the cap rate lets you compare your investment's performance against others. A low cap rate, especially in a high-value market, often signals that it’s a great time to sell and move your capital to an area with better returns.

Tracking these numbers gives you a solid, data-driven foundation for making a smart decision. You can get into the nitty-gritty by reading our practical guide to rental property cash flow analysis.

The Squeeze: When Appreciation Outpaces Rent

It’s easy to get excited when you see your property's value skyrocket, but many landlords fall into a common trap: they don't notice that their rental income is lagging far behind. This is what we call "return compression," and it puts a serious squeeze on your profitability.

As your home's value shoots up, so do your property taxes and insurance premiums. But if you can't raise the rent enough to cover those new costs, your cash flow takes a direct hit.

This is a classic trigger to sell. For instance, the median asking rent for apartments was $1,837 in 2023. Meanwhile, home prices were soaring, hitting an average of $512,800 by the second quarter of 2025. That’s a huge gap. This mismatch crushes cap rates, often pushing them below 5% in hot markets, which makes selling look a whole lot more appealing than holding.

When your property becomes more valuable on paper than it is as an income-producing asset, you've hit a crossroads. Your equity is essentially trapped, and selling is the key to unlocking its full potential.

Spotting Diminishing Returns

Every property has a lifecycle. In the early years, returns are great because the big-ticket items—the roof, HVAC, plumbing—are still in good shape. But as a property gets older, it inevitably hits a point of diminishing returns where maintenance costs start to snowball.

Here’s a simple way to think about it:

The Growth Phase (Years 1-10): Repairs are small and predictable. Your cash flow is healthy and consistent.

The Plateau Phase (Years 10-20): Bigger repairs start popping up, like a new water heater or replacing appliances. Your returns are holding steady but aren't really growing anymore.

The Decline Phase (Year 20+): This is when the monster expenses show up. A new roof ($10,000+), a full HVAC replacement ($8,000+), or foundation problems can vaporize years of profit in one fell swoop.

If you find yourself in a constant battle with five-figure repair bills, your property has likely entered its decline phase. At this stage, the money and stress needed to keep it afloat often outweigh the income it brings in. Selling before these massive costs hit lets you walk away with your profits still in your pocket.

Navigating Taxes and Strategic Wealth Moves

Making money on the sale of your rental is one thing. Actually keeping that money is a whole different ballgame. The second that sale closes, you can be sure Uncle Sam will be waiting for his cut. Understanding your tax liability isn't just a chore for your accountant—it's absolutely essential to figuring out your true profit and whether selling now even makes sense.

Ignoring taxes is like celebrating a big win before the game is over. The final score, your actual take-home cash, can be a real shock if you're not prepared. For rental property owners, two specific taxes can take a serious bite out of your proceeds: Capital Gains Tax and Depreciation Recapture.

The One-Two Punch of Real Estate Taxes

When you sell an asset for more than you paid for it, that profit is considered a capital gain, and it's taxable. How much you pay depends on your income and how long you've held the property. For properties owned more than a year, the long-term capital gains rates are typically 0%, 15%, or 20%.

But here's the tax that catches so many investors off guard: Depreciation Recapture. Every year you own a rental, the IRS lets you deduct a portion of the property's value (depreciation) from your income, which is a nice tax break. The catch? When you sell, the IRS wants that money back.

All the depreciation you've claimed over the years gets "recaptured" and is taxed at a special rate of up to 25%. For landlords who have held a property for a decade or more, this can add up to a massive, unexpected tax bill. This is just one of many reasons to review a comprehensive landlord's guide to rental property tax deductions long before you even think about listing.

Selling a rental isn't just about the sale price. Your real profit is what’s left after capital gains and depreciation recapture taxes are paid. Failing to account for both can lead to a much smaller payday than you anticipated.

The Ultimate Wealth-Building Tool: The 1031 Exchange

What if you could hit the pause button on that tax bill? What if you could take all your profits and roll them straight into your next, bigger, better investment? That's precisely what a 1031 Exchange lets you do.

This powerful provision in the tax code allows you to defer—not eliminate, but defer—paying capital gains and depreciation recapture taxes by reinvesting the proceeds into a similar "like-kind" property. It's the perfect strategy for investors who want to trade up, diversify into a new market, or consolidate several smaller properties into one larger asset. Think of it as trading in your car for a new one without having to pay tax on the profit you made on the old one.

But this incredible benefit comes with a catch: the rules are ironclad and the timelines are unforgiving.

The 45-Day Identification Window: From the day you close on your old property, you have exactly 45 days to formally identify, in writing, the properties you intend to buy. No exceptions.

The 180-Day Closing Window: You must close on one of those identified properties within 180 days of your original sale.

These deadlines run at the same time and are strictly enforced by the IRS. Messing them up can blow up the entire exchange, leaving you with a huge tax bill.

Sell vs 1031 Exchange A Simple Comparison

To really see the power of a 1031 exchange, let's look at a side-by-side comparison of a standard sale versus a tax-deferred exchange.

Financial Aspect | Standard Sale | 1031 Exchange |

|---|---|---|

Initial Sale Profit | $200,000 | $200,000 |

Taxes Due (Est.) | $45,000 (Gains & Recapture) | $0 (Taxes are deferred) |

Cash to Reinvest | $155,000 | $200,000 |

Long-Term Impact | Smaller down payment on next property, reduced buying power. | Full profit is used for the next purchase, allowing for a larger, better-performing asset. |

As you can see, the difference is staggering. The 1031 Exchange allows you to keep your entire war chest of capital working for you, compounding its growth over time. It’s a strategic move that turns a simple sale into a powerful leap up the property ladder.

When Repairs and Headaches Outweigh the Returns

Sometimes the spreadsheets and market reports don't tell the whole story. The most powerful reason to sell can be the property itself. Every rental has a lifecycle, and eventually, the balance can tip from a profitable asset to a money pit that eats up your time and energy.

Spotting this turning point is a critical skill. It’s not about giving up; it’s about making a shrewd business move before a property starts draining your bank account and your sanity. Many seasoned investors call this reaching a state of capital expenditure fatigue.

The Looming Threat of Capital Expenditures

Capital expenditures, or CapEx, are the big ones. These aren't your typical minor repairs; they are the major system replacements and upgrades that can define a decade of ownership. A leaky faucet is a minor operational headache. A new roof is a capital expenditure.

These expenses don't just temporarily halt your cash flow—they can vaporize years of accumulated profit with a single check. Knowing when these massive bills are coming is one of the most compelling reasons to sell.

The best defense is a good offense: forecasting these costs. Here’s a rough guide to the lifespan of major components that can help you look down the road.

Asphalt Shingle Roof: You can expect about 20-30 years out of one. A full replacement can be a gut punch, often costing $8,000 to $15,000.

HVAC System: The heart of the home, a furnace and AC unit combo, typically lasts 15-20 years. Replacing it will likely run you $7,000 to $12,000.

Water Heater: A standard tank heater will give you 8-12 years of service. It’s a less terrifying expense but still in the $1,000-$2,000 range.

Major Plumbing or Electrical Work: If you have an older property with galvanized pipes or knob-and-tube wiring, you could be looking at a full overhaul costing tens of thousands.

If you see that two or three of these are on their last legs, it might be the perfect time to sell. Cashing out your equity before the systems fail lets the next owner take on those projects, who might be planning a gut renovation anyway.

The Hidden Cost of Landlord Burnout

Beyond the checks you write, a high-maintenance property has a very real, but often ignored, human cost: landlord burnout. The constant pressure of managing a problem-plagued property can quickly turn a dream of passive income into a nightmare.

This isn’t about a one-off late-night call for a clogged toilet. It's the slow, grinding weight of chronic issues, the endless back-and-forth with contractors, and the constant tenant complaints about things you can't easily fix.

Landlord burnout is a legitimate business expense measured in your time, energy, and peace of mind. When the stress of ownership consistently outweighs the financial rewards, it's a clear signal that it may be time to sell.

If you find yourself dreading a call from your tenant or feeling perpetually overwhelmed by the property's to-do list, that’s a perfectly valid reason to sell. You can roll the proceeds into a newer, turn-key rental or move into a different kind of investment altogether—one that actually gives you your life back. Your well-being is a huge part of your total return.

Does This Property Still Fit Your Life?

The numbers can tell you how a property is performing, but they can't tell you what to do next. That final piece of the puzzle is all about you. A rental property is just one part of your bigger financial picture and your life story, so the decision to sell often comes down to how well that asset fits your vision for the future.

A property that was a perfect fit five years ago might now be holding you back from new opportunities. When that happens, selling isn’t just about one property’s performance—it’s a strategic move to reposition your capital and time to better serve where you're headed now.

When Life Signals It's Time to Sell

Life changes, and a smart investment strategy needs to be flexible enough to change right along with it. In fact, many seasoned investors sell not because a property is failing, but because their own priorities have shifted.

Here are a few common life events that make selling the logical next step:

You're Over-Concentrated: Your rental has appreciated so much that a huge chunk of your net worth is now tied up in one single address. Selling lets you cash out and spread that capital across different investments—stocks, bonds, or even real estate in another market—to lower your overall risk.

You Need to Fund the Next Chapter: The equity you've built can be the fuel for your next big adventure. Maybe that means cashing out to fund your retirement, freeing up money to start a business, or paying for your kid's college education.

You Just Want Your Time Back: Let's be honest, being a landlord is a job, even with a great property manager. For some investors, the goal eventually shifts from maximizing income to maximizing freedom. Selling can be your exit ramp from the day-to-day responsibilities, giving you back your weekends and your peace of mind.

Selling isn’t an admission of failure; it’s a strategic pivot. You're consciously deciding that your money and energy can work harder for you somewhere else.

Thinking Like a Portfolio Manager: Trading Up

The best investors think like portfolio managers, constantly evaluating every asset to make sure it’s the best player on their team. Sometimes, you have to trade a good player to get two great ones. This is a powerful reason to sell a perfectly good rental property.

Let’s say you own a single-family home in a stable, slow-growth market. The cash flow is decent, but you know it’s never going to see massive appreciation. You could sell that one property and use a 1031 exchange to roll the proceeds into two smaller properties in an up-and-coming neighborhood with new employers and development projects on the horizon.

Suddenly, you’ve accomplished several things at once:

Boosted Your Potential Returns: You've moved your capital from a low-growth asset into a high-growth environment.

Diversified Your Income: Owning two properties means a vacancy in one doesn't kill your entire rental income for the month. Your risk is now spread out.

Reset the Maintenance Clock: You can target newer or recently renovated properties, pushing those big-ticket repairs like a new roof or HVAC system much further down the road.

At the end of the day, deciding when to sell a rental is deeply personal. It means looking beyond the monthly rent check and asking a much bigger question: "Is this investment still serving the life I'm trying to build?" When the answer becomes "no," it's time to make your move.

Common Questions About Selling a Rental Property

Even with a solid game plan, you're bound to have questions as you get closer to pulling the trigger. Let's tackle some of the most frequent "what ifs" that pop up for landlords thinking about selling.

How Much Profit Should I Make Before Selling?

Every investor has a different number in their head, so there's no single right answer here. A good rule of thumb, though, is to aim for a net profit of at least 20-25% over what you originally put in, after you've paid off the mortgage, closing costs, and taxes.

Another great way to look at this is through your return on equity (ROE). Think about it: if your property's value has shot up but the rent hasn't budged, your ROE is actually shrinking. Selling lets you unlock that equity and put it to work somewhere else where it can generate a much better return.

Should I Sell When the Mortgage Is Paid Off?

Paying off the mortgage feels like crossing the finish line, and that pure cash flow is tough to beat. But here's the catch—at that point, your capital is sitting idle. That huge chunk of money tied up in one paid-off property could be the down payment on several new properties, dramatically multiplying your potential returns.

Selling a paid-off rental isn't a retreat. It's a strategic move to re-energize your capital. The real question is whether that equity could be a more powerful engine for your portfolio in a different market or a new investment.

Is It Better to Sell Vacant or with Tenants?

This really comes down to who you're trying to sell to.

If you’re selling to another investor, a property with a great, long-term tenant is a massive plus. It means instant income and zero work finding someone new. They can start making money from day one.

But if you want to attract buyers who are looking for a home to live in, an empty property is almost always the way to go. It's a blank canvas. An empty home is far easier to clean, stage, and show, letting potential buyers picture their own lives there without navigating an existing lease.

What Are the Biggest Mistakes to Avoid?

Knowing what not to do is half the battle. When you decide it's time to sell your rental, make sure you sidestep these common stumbles:

Ignoring the Tax Bill: One of the biggest shocks for sellers is underestimating capital gains and depreciation recapture taxes. This can take a huge bite out of your profit. Always run the numbers with a tax pro before you list.

Botching Tenant Communication: Whether you need the property vacant or just need tenants to cooperate for showings, poor communication is a recipe for disaster. Be clear, respectful, and give them plenty of notice.

Skipping the Prep Work: It's tempting to sell a rental "as-is" to save a few bucks, but that almost always costs you more in a lower sale price. Even small, smart updates can deliver a fantastic return and help the property sell faster.

Deciding when to sell your rental property has a lot of moving parts. At Keshman Property Management, we bring our 20 years of hands-on landlord experience to the table, helping you analyze your property's performance and make the best strategic move for your portfolio. We're here to make owning rental properties less daunting and more gratifying. Learn more by visiting our website at https://mypropertymanaged.com.

Comments