What is a Rent Ledger? A Practical Guide for Property Managers

- Sarah Porter

- Dec 12, 2025

- 13 min read

Updated: Dec 20, 2025

Think of a rent ledger as the complete financial story of a tenancy. It’s a detailed, running record that tracks every dollar—every rent payment, late fee, security deposit, or utility charge—associated with a specific rental unit. This document acts as the official, shared history for both the landlord and the tenant, showing exactly what was paid, when it was paid, and what, if anything, is still owed.

The Financial Heartbeat of Your Rental Property

A great way to understand a rent ledger is to compare it to a bank account statement. Your statement doesn't just show your final balance; it lists every single deposit, withdrawal, and fee in chronological order. A rent ledger does the same for a tenancy, itemizing each transaction and maintaining a running balance so you can see a tenant's financial status at any given moment.

This isn’t just a nice-to-have document; it's a cornerstone of professional property management. Across the United States, where rentals make up roughly 36% of all households, property owners rely on accurate ledgers to keep a close eye on their income and verify tenant payment habits. This simple tool turns a messy pile of payment receipts and bank alerts into a clear, actionable financial record. You can discover more insights about rent ledgers on Landlord Studio to see how widely they're used.

Why a Rent Ledger Is Non-Negotiable

Whether you’re a seasoned investor with a large portfolio or a first-time landlord renting out a single-family home, keeping a clean rent ledger is just smart business. Without one, you’re left trying to piece together a tenant's history from memory, bank deposits, or a shoebox full of notes—a recipe for confusion and disputes.

A well-maintained rent ledger moves beyond simple bookkeeping. It becomes your primary evidence in disputes, a crucial tool for financial planning, and the clearest indicator of your property’s performance.

This document is absolutely essential for a few critical reasons:

Financial Clarity: It gives you a crystal-clear picture of your rental income. You know exactly who has paid, what the payment was for (rent, pet fees, etc.), and the date it was received. No guesswork involved.

Legal Protection: If you ever face a payment dispute or need to proceed with an eviction, a detailed ledger is your most powerful piece of evidence. It’s hard to argue with a clear, chronological record of transactions.

Smarter Decisions: Are certain tenants consistently late? Is your cash flow predictable? The ledger helps you spot trends, identify great tenants you want to keep, and make informed decisions about renewing leases.

Ultimately, knowing what a rent ledger is and how to use it is a fundamental step in treating your rental property like a real business. It’s not just paperwork; it’s a foundational tool for protecting your investment and ensuring your success.

Deconstructing a Bulletproof Rent Ledger

A truly effective rent ledger is so much more than a list of numbers; it's the financial story of a tenancy, told one transaction at a time. To be a reliable tool for both accounting and legal protection, it needs to be built with specific, well-organized components. Each piece of information serves a real purpose, turning a simple payment log into an airtight record.

Think of it like building a house. You can't put up the walls and roof without a solid foundation. For a rent ledger, that foundation is the basic information that gives context to every dollar that comes in or goes out.

These core details make sure there's never any question about which tenant, property, or lease agreement the financial data belongs to. It’s the first and most important step toward creating clarity.

The Foundational Information

Before you even start logging payments, every rent ledger has to begin with clear identifying details. This information anchors every transaction to the right person and place, which is absolutely critical for preventing mix-ups, especially if you're managing more than one unit.

Tenant and Property Identifiers: You need the full name of every tenant on the lease, the complete property address, and the specific unit number (like "Apartment 4B"). This level of precision is non-negotiable for clear communication and legal accuracy.

Lease Term Details: Note the exact lease start and end dates. This simple step frames the entire financial history within a specific contract period.

Security Deposit Record: Always document the amount of the security deposit collected and the date you received it. While it's separate from rent, it’s a vital part of the tenancy's financial picture.

Once this foundation is set, you can get into the real meat of the ledger: the day-to-day transactions. This is where meticulous record-keeping truly pays off.

Tracking Every Transaction

The heart of any rent ledger is its chronological log of all financial events. Each entry needs to be a complete snapshot of a single transaction, leaving zero room for doubt or misinterpretation. It’s this granular detail that makes a rent ledger so powerful for preventing—and resolving—disputes.

A vague entry like "Rent Paid" is just asking for future conflict. On the other hand, an entry like "October 2024 Rent Payment - Check #1234" provides undeniable proof and protects both the landlord and the tenant.

The key is to treat each column of your ledger as a non-negotiable piece of the puzzle. A well-structured ledger makes it easy to see exactly what’s going on at a glance.

Here’s a look at the essential fields that every robust rent ledger should have.

Essential Components of a Rent Ledger

This table breaks down the key columns that form the backbone of a comprehensive rent ledger. Each one plays a critical role in creating a clear and defensible financial record.

Field/Column | Description & Purpose | Example Entry |

|---|---|---|

Transaction Date | The exact date a payment was made or a charge was incurred. This is essential for tracking timeliness. | 01/05/2025 |

Description | A clear, specific note on what the transaction is for. This prevents confusion between rent, fees, or other charges. | October Rent |

Charge/Debit (-) | The amount a tenant is billed for. This includes monthly rent, late fees, pet fees, or repair costs. | $1,500.00 |

Payment/Credit (+) | The amount a tenant actually pays. Recording this separately from the charge is vital for tracking partial payments. | $1,500.00 |

Payment Method | How the payment was made (e.g., online portal, check, bank transfer). This is useful for record-keeping and tracing funds. | Online Portal |

Running Balance | The tenant's current outstanding balance. This is the single most important column for an at-a-glance financial status. | $0.00 |

Building your ledger with this structure ensures every single financial interaction is captured accurately. It creates an unshakeable record of the tenancy's history and is the gold standard for professional property management.

Rent Ledger vs. Rent Roll: Understanding the Difference

In the world of property management, the terms "rent ledger" and "rent roll" get thrown around a lot, and it's easy to see why they get confused. But mixing them up is a classic rookie mistake that can leave you with serious blind spots in your financial picture.

Think of it like this: a rent ledger is the detailed financial story of a single tenant's lease. It’s a running diary that tracks every single charge, payment, fee, and credit from the moment they sign the lease until they move out.

A rent roll, on the other hand, is more like a quick snapshot of your entire property’s financial health at one specific moment. It’s the high-level summary, not the nitty-gritty story.

The Ledger for Detail, The Roll for Overview

When a tenant calls asking why they have a balance or you need to prove they paid rent late last March, the rent ledger is your best friend. It provides the granular, line-by-line evidence you need to manage that specific tenancy. It's the document you pull up to answer day-to-day questions and resolve individual account issues.

The rent roll serves a completely different, big-picture purpose. It's the document you show to a potential investor, a lender, or an appraiser to prove your property's value. It answers questions like, "What's the total monthly income?" or "Which units are vacant?" It’s all about a high-level, strategic view of the asset.

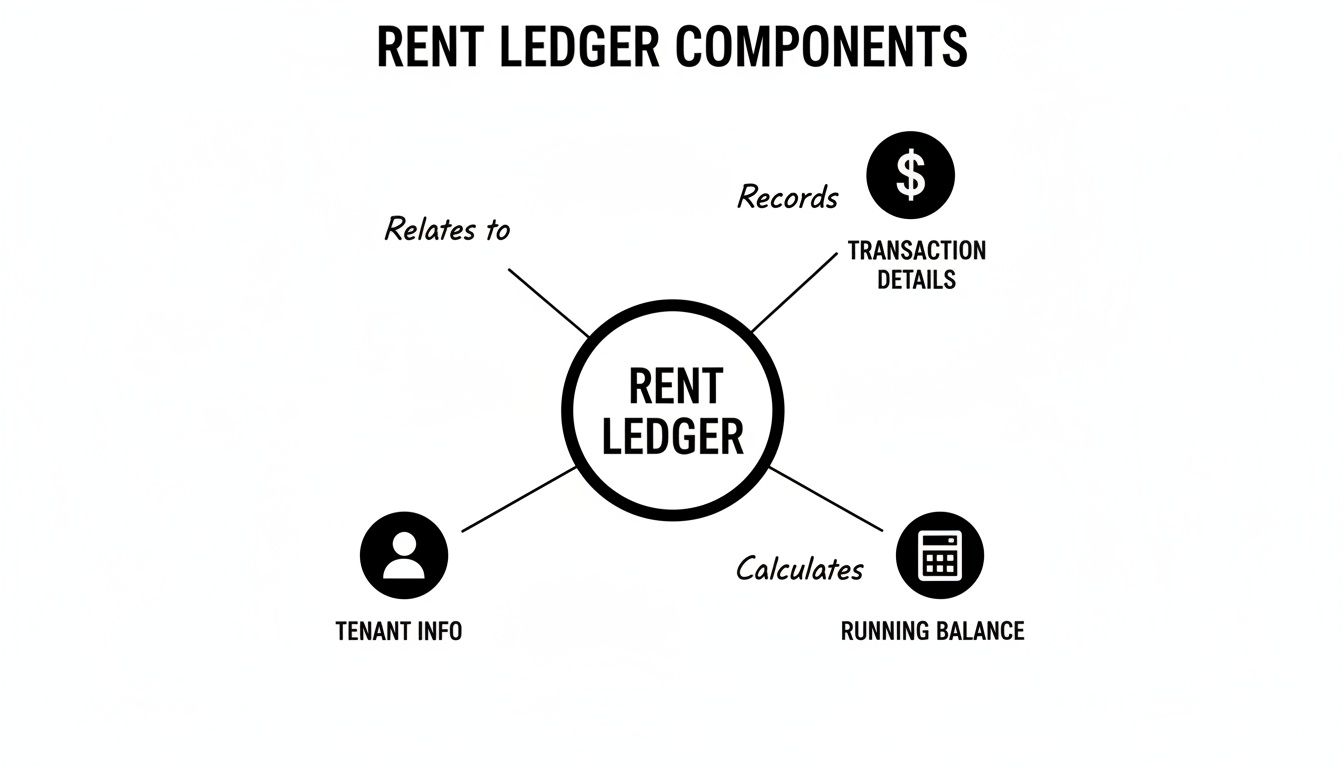

The diagram below really breaks down what gives the ledger its power—connecting individual tenant details with specific transactions to maintain a constantly updated balance.

As you can see, the ledger is where tenant information, money in, and money out all come together to tell a complete story for that one unit.

A Side-by-Side Comparison

Let's put them head-to-head to make the distinction perfectly clear. Knowing which document to grab for which task is a fundamental skill for any landlord or property manager.

Rent Ledger vs. Rent Roll Key Differences

Attribute | Rent Ledger | Rent Roll |

|---|---|---|

Scope | Focuses on a single tenant or rental unit. | Provides a summary of all units in a property or portfolio. |

Level of Detail | Highly detailed. Includes every transaction, payment method, and running balance. | High-level summary. Shows total rent due, lease terms, and occupancy status. |

Primary Use | Operational. Used for daily management, resolving disputes, and legal evidence. | Strategic. Used for property valuation, investor reporting, and financial analysis. |

Timeframe | Historical. Shows the complete financial history over the entire lease term. | Snapshot. Captures the property's financial status at a single point in time. |

At the end of the day, you use the rent ledger to manage a tenancy and the rent roll to evaluate your investment. Both are absolutely critical, but they are not interchangeable.

Getting this right means you always have the correct information ready, whether you're talking to a tenant about a late fee or to a bank about refinancing. You wouldn't use a single person's biography to take a national census, and you shouldn't use a rent roll to track an individual's payment history. Mastering both is what separates the pros from the amateurs.

The Legal Power of an Accurate Rent Ledger

A rent ledger is far more than just a simple spreadsheet for tracking payments; it's one of your most powerful assets as a landlord. When you maintain it correctly, this document becomes your best defense in a dispute and a critical tool for managing your property's finances. Its real value shines when disagreements pop up, especially when things get legal.

Think about it. What happens when a tenant insists they paid rent on time, but your bank account tells a different story? Or maybe they're arguing about a late fee you charged months ago. Without a detailed ledger, it quickly devolves into a messy "he said, she said" scenario. But with a clear, chronological record of every single charge, payment, and running balance, you can shut down the argument before it even starts.

Your Strongest Evidence in Court

If you ever find yourself in the unfortunate position of needing to evict a tenant for non-payment, the rent ledger will be the absolute foundation of your case. A judge isn’t interested in stories; they want to see a factual, easy-to-follow financial history of the tenancy. A well-kept ledger delivers exactly that, clearly showing a pattern of missed or partial payments that is incredibly difficult to argue against.

Take a market like New York City, for example, with its 2 million rental units and notoriously complex tenant laws. Property managers there live and die by their documentation. It's been shown that 15-20% of eviction cases in demanding markets get thrown out simply because of sloppy or incomplete paperwork. An accurate ledger isn't just a "nice-to-have"—it's often the single most important piece of evidence you'll present.

Beyond Disputes: Financial and Tax Implications

The benefits don't stop in the courtroom. The clarity a rent ledger provides is a massive advantage for your day-to-day financial operations, especially come tax time. Instead of digging through a year's worth of bank statements trying to separate rent deposits from other transactions, your ledger gives you a clean, organized summary of all your rental income. It makes tax reporting simple and far less stressful.

A detailed rent ledger not only proves what you've earned but also helps substantiate any deductions related to the property, such as repair costs billed to a tenant. It creates a complete financial narrative that supports your tax filings.

This kind of financial transparency has a ripple effect on the value of your investment. An accurate ledger can:

Secure Better Financing: When you're looking for a loan or want to refinance, lenders want solid proof of a consistent income stream. Your rent ledger provides it.

Increase Property Value: Thinking of selling? A documented history of timely rent payments makes your property much more attractive to potential buyers by proving it’s a reliable, income-generating asset.

At the end of the day, https://www.mypropertymanaged.com/meticulous-record-keeping turns your ledger from a tool you only use when there's a problem into a proactive strategy for building wealth. It’s also vital for staying compliant with tax laws. To understand more about this, it’s worth looking into the specifics of UK property rental income tax. It truly is a foundational piece of professional and profitable property management.

How to Build and Maintain Your Rent Ledger

Creating a rent ledger doesn't have to be complicated, but it absolutely requires a consistent process. Most landlords go one of two ways: a simple do-it-yourself (DIY) spreadsheet or dedicated property management software. The best path for you really just boils down to how many properties you manage and how comfortable you are with technology.

If you only have a handful of units, a well-structured spreadsheet in Google Sheets or Excel can work beautifully. This route costs you nothing but time and gives you total control over how you organize everything. The catch? As you add more properties, manual entry becomes a major time sink and opens the door to costly human errors. That’s when specialized software starts looking very attractive.

For any property manager juggling multiple tenants, adopting solid small business document management solutions is a non-negotiable part of building and maintaining clean, accurate rent ledgers.

Starting with a Spreadsheet

Going the DIY route is pretty straightforward. Just create a new worksheet for each tenant lease and set up columns for all the key details we’ve already covered. The real trick is to use basic formulas to handle the math for you—it’s a simple step that cuts down on mistakes and saves a ton of time.

At a minimum, your spreadsheet needs these columns:

Transaction Date: The day a payment was made or a charge was added.

Description: A quick, clear note, like "January 2025 Rent" or "Late Fee."

Charge/Debit: Any amount the tenant owes you.

Payment/Credit: Any amount the tenant has paid.

Running Balance: This is the most crucial column. The formula should be something like .

This simple setup transforms your spreadsheet from a static list of numbers into a living, breathing financial record for each tenant. For a deeper dive into organizing your finances, check out our complete guide to bookkeeping for rental property.

Upgrading to Property Management Software

When you find yourself spending more time updating spreadsheets than managing your properties, it’s a clear sign to look into software. Modern platforms are built to automate the entire rent ledger process. They link directly to online payment systems, so when a tenant pays rent, the ledger updates itself instantly. No more manual data entry.

Here's a powerful statistic: digital rent ledgers used in property management software have been shown to reduce manual errors by up to 90%. In fact, a report from the National Apartment Association revealed that 78% of property managers said these systems helped them boost their annual rent collection rates from 92% to 97%.

This automation is a game-changer. It not only frees up countless hours but also builds a far more professional and reliable system that tenants and owners can trust.

Ultimately, it doesn't matter which method you pick. The secret to a useful rent ledger is discipline. Log every single transaction the moment it happens. Do a quick check against your bank statements each month to spot any issues early. And always, always keep a secure backup. This simple routine creates a sustainable system that protects you, your tenant, and your investment.

Using Your Ledger for Smarter Management Decisions

Think of a rent ledger as more than just a historical record of who paid what and when. It’s actually a powerful tool that helps you look ahead and make smarter, more profitable decisions for your property. When you treat it as a source of real business intelligence, it stops being a passive document and becomes an active asset for managing your investment.

The real magic happens when you start spotting patterns. A quick look at your ledgers can instantly tell you which tenants are rock-solid with their payments and which ones consistently lag behind. This insight is gold when lease renewal season rolls around. It helps you decide who to prioritize keeping and how to approach conversations with tenants who might represent a higher financial risk.

From Data to Actionable Insights

By analyzing this data, you can shift from simply reacting to problems to proactively managing your property. Instead of just chasing down late payments after the fact, you can start to anticipate them. This allows you to put smarter strategies in place to improve your property’s overall cash flow.

For instance, a meticulously kept ledger gives you the black-and-white proof you need to apply late fees fairly and consistently. It also acts as concrete evidence if you need to make justified deductions from a security deposit for unpaid rent or other charges. This protects you from potential disputes and keeps your relationship with tenants transparent and professional.

Your rent ledger doesn't just tell you what happened; it provides the data you need to shape what happens next. It's the key to minimizing risk and maximizing your property's performance.

The Strategic Value of Your Ledger

Looking beyond just one tenant, your collection of ledgers gives you a bird's-eye view of your entire portfolio's financial health. For any serious investor, this data is absolutely critical. For example, ledgers can be used for advanced analytics like predicting vacancies. A Yardi Matrix analysis of 100,000 assets found that multi-family properties using them often see 96% occupancy versus 91% without. You can find more details on how ledgers support modern property management on TurboTenant.

It's clear that a well-maintained rent ledger is a cornerstone of modern, data-driven property management. By tapping into these insights, you can fine-tune everything from tenant screening to your overall rent collection methods, ultimately leading to a much healthier bottom line.

Here are a few of the most common questions we get from landlords about rent ledgers. Let's dig into some practical answers to help you get the most out of this essential tool.

What About Past Tenants? Can I Create a Ledger for Them?

Absolutely. In fact, it's a great idea. You can piece together a rent ledger for a past tenancy by pulling information from old bank statements, records from payment apps, and the original lease agreement.

Having this historical record can be a lifesaver. You might need it to amend a previous year's tax return, or it could be the key piece of evidence needed to settle a financial dispute that pops up long after a tenant has moved out.

How Often Should I Update My Rent Ledgers?

The best practice here is simple: update it the moment a transaction happens. As soon as that rent payment hits your account or you add a late fee, log it.

This habit of real-time updates keeps your records spotless and accurate. If you can't do it instantly, make it a non-negotiable weekly task to sit down and reconcile everything. You’ll thank yourself later.

Think of a constantly updated ledger not just as a historical document, but as a live dashboard showing the financial pulse of your property. This small habit prevents massive headaches and hours of backtracking down the road.

Is a Simple Spreadsheet Okay, or Do I Need Special Software?

For landlords with just one or two properties, a well-organized spreadsheet can work just fine. You can easily track payments and charges without needing a complex system.

However, once you start managing three, four, or more properties, you'll feel the growing pains. That's when dedicated property management software really starts to shine. It automates most of the work, cuts down on human error, and gives you a secure, scalable way to manage your finances that a spreadsheet just can't compete with.

Keeping meticulous financial records is non-negotiable, but it's also time-consuming. At Keshman Property Management, we handle the day-to-day details like rent ledgers so you can focus on the big picture. Learn how we can make your life easier.

Comments