What Is a Cash on Cash Return? A Landlord's Guide to Calculating It

- Sarah Porter

- Feb 7

- 14 min read

Updated: Feb 14

When you're investing in real estate, one of the most important questions you can ask is: "How hard is my money really working for me?" The cash-on-cash return metric gives you the straight answer.

Think of it this way: it’s the annual return you get based purely on the actual cash you pulled out of your pocket to buy the property. It cuts through the noise of appreciation and tax benefits to tell you what you're earning on your investment, right here, right now.

Decoding Your Investment Performance

While other metrics are useful, cash-on-cash return zeroes in on a single, vital relationship: the connection between the cash you put in and the cash you get out each year. It answers the fundamental question for any landlord: "For every dollar I invested, how many cents am I getting back annually?"

This directness makes it an indispensable tool, especially when you're using financing. It helps you see how efficiently your capital is performing. Since it focuses only on your personal cash contribution, it’s a brilliant way to compare different deals, even if you used different loan amounts for each.

The Core Components

Getting a handle on cash-on-cash return just means understanding two numbers, which we’ll break down in more detail soon:

Annual Pre-Tax Cash Flow: This is the profit you have left over after you’ve collected all the rent and paid all the bills for the year—including the mortgage.

Total Cash Invested: This is every single dollar you spent to get the property up and running. Think down payment, closing costs, and any immediate repairs or renovations.

The math itself is simple: just divide your annual cash flow by the total cash you invested. For example, if you put $60,000 of your own money into a deal and it generates $12,000 in positive cash flow for the year, your cash-on-cash return is a very healthy 20%.

Most experienced investors agree that a good target for a residential rental is somewhere in the 8% to 12% range. You can dig deeper into calculating this key real estate metric on offermarket.us to see how your own properties stack up.

Breaking Down the Cash-on-Cash Return Formula

To really get a feel for how your investment is performing, you need to get your hands dirty with the two main parts of the cash-on-cash return formula. The math itself is simple, but its power comes from plugging in the right numbers. Let's walk through exactly what you need for each piece.

The formula looks like this: (Annual Pre-Tax Cash Flow / Total Cash Invested) x 100%.

Think of it like a recipe. If you mess up the ingredients, the final dish just won't be right. In the same way, getting your cash flow or initial investment numbers wrong will give you a skewed return percentage, and that can lead to some bad decisions down the road.

Calculating Your Annual Pre-Tax Cash Flow

Your annual pre-tax cash flow is the engine driving your return. It's the actual profit your property spits out over a year before you give the tax man his cut. To find this number, you take all the income your property generates and subtract what it costs to run it, including your loan payments.

Start with your Gross Scheduled Income (that's the perfect-world rent you’d collect with zero vacancies). Then, start subtracting the real-world costs:

Vacancy Losses: Let's be real—no property stays rented 100% of the time. A good rule of thumb is to knock 5-10% off your gross income to account for the time it sits empty between tenants.

Operating Expenses: These are all the day-to-day costs that keep the lights on and the property in good shape. We're talking property taxes, insurance, maintenance, repairs, HOA dues, and any property management fees you pay.

Mortgage Payments: This is a big one. You need to subtract the entire mortgage payment for the year, which includes both the principal and the interest.

What's left over is your annual pre-tax cash flow. It's the money that actually hits your bank account over a 12-month period. This is different from Net Operating Income (NOI), which doesn't factor in your mortgage. If you want to dive deeper, you can explore our complete guide to understand what Net Operating Income is and see how the two metrics compare.

Identifying Your Total Cash Invested

The second key ingredient is tracking down every single dollar that came out of your own pocket to get the deal done. This isn’t just your down payment—it's the total cash you had to bring to the table to make the investment a reality.

When calculating your total cash invested, it's crucial to be honest with yourself and include everything. People often forget the smaller costs, which makes their return look better on paper than it is in reality.

Here’s a table to help you capture every expense.

Calculating Your Total Cash Invested

Expense Category | Description | Example Cost |

|---|---|---|

Down Payment | The largest chunk of cash paid upfront for the property. | $60,000 |

Closing Costs | Fees for appraisal, inspection, title, loan origination, etc. | $7,500 |

Initial Repairs | "Make-ready" costs like new paint, carpet, or appliances. | $5,000 |

Prepaid Expenses | Upfront payments for things like property taxes or insurance. | $1,500 |

Total Cash | The complete out-of-pocket investment. | $74,000 |

Adding all of these up gives you a true picture of your Total Cash Invested.

Your Total Cash Invested is the denominator in the cash-on-cash return formula. Underestimating this number is a common mistake that artificially inflates your perceived return, giving you a false sense of profitability.

By tracking these figures meticulously, you're setting yourself up for a calculation that reflects what’s really happening with your money.

How to Calculate Cash-on-Cash Return with Real Examples

Theory is one thing, but seeing the numbers in action is what makes the concept of cash-on-cash return really sink in. Let's walk through two realistic scenarios to show you exactly how the calculation works. By comparing a financed purchase with an all-cash deal, you'll see how your investment strategy directly shapes the return you see in your pocket each year.

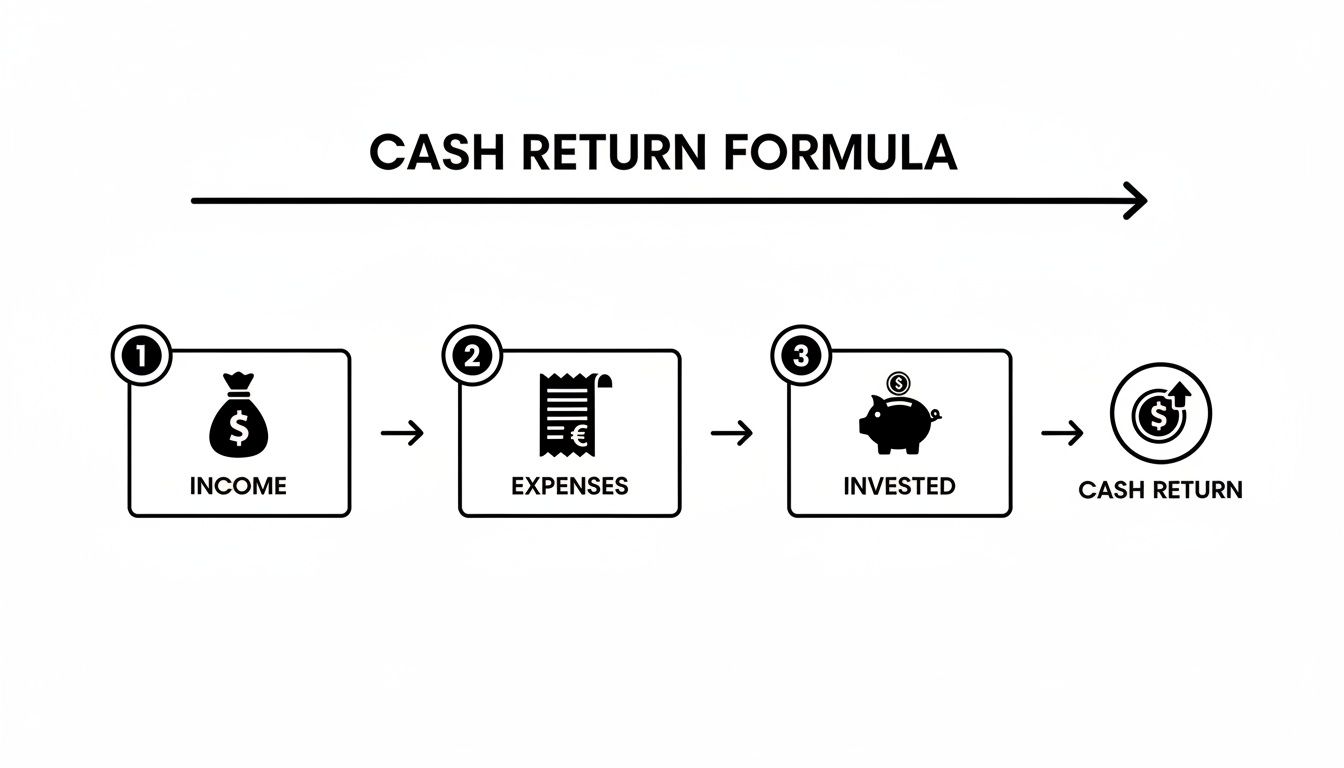

The formula itself is pretty straightforward. It just boils down to how much cash your property generates versus how much cash you put in to get it.

This visual breaks it down nicely: you start with your rental income, subtract all the expenses to find your actual cash flow, and then measure that against your initial cash investment.

Example 1: The Financed Single-Family Home

Imagine you buy a single-family home for $300,000. You're going the traditional route with a conventional loan, which requires a 20% down payment.

First, let's figure out your Total Cash Invested. This is every dollar you brought to the table.

Down Payment: $300,000 x 20% = $60,000

Closing Costs: Usually around 3% of the home price, so that's $9,000

Initial Repairs: Let's say it needs some paint and new fixtures, adding $5,000

Total Cash Invested: $60,000 + $9,000 + $5,000 = $74,000

Next up is your Annual Pre-Tax Cash Flow. If the property rents for $2,500 per month, that's $30,000 in gross income for the year. But we have to account for all the costs.

Gross Annual Income: $30,000

Less Vacancy (5%): -$1,500

Less Operating Expenses (Taxes, Insurance, Maintenance): -$7,500

Less Annual Mortgage Payments (Principal & Interest): -$15,600

Annual Pre-Tax Cash Flow: $5,400

Now for the easy part. Just plug those two numbers into the formula:

Cash-on-Cash Return = ($5,400 / $74,000) x 100 = 7.3%

A 7.3% return is a pretty solid starting point for a financed property. It’s important to remember this metric focuses purely on cash flow. If you want a bigger picture of your overall profit, you can use our rental property ROI calculator to maximize your investments for a more complete view.

Example 2: The All-Cash Condo Purchase

Now for a different approach. Let's say you buy a $200,000 condo with cash. This changes the math quite a bit, mainly because there's no mortgage eating into your monthly income.

Let’s calculate your Total Cash Invested:

Purchase Price: $200,000

Closing Costs: A bit lower for cash deals, around 2%, so $4,000

Initial Repairs: $3,000

Total Cash Invested: $200,000 + $4,000 + $3,000 = $207,000

Next, what’s the Annual Pre-Tax Cash Flow? Let's assume the condo rents for $1,800 a month, which is $21,600 annually.

Gross Annual Income: $21,600

Less Vacancy (5%): -$1,080

Less Operating Expenses (Taxes, Insurance, HOA Fees): -$6,000

Annual Pre-Tax Cash Flow: $14,520

Notice how much higher that cash flow is without a mortgage payment? It makes a huge difference.

Let's run the final calculation:

Cash-on-Cash Return = ($14,520 / $207,000) x 100 = 7.0%

Here's the interesting part. Even though the annual cash flow is much higher in the all-cash deal, the actual return percentage is slightly lower. Why? Because of the massive initial cash investment. This comparison is the perfect illustration of how using a loan (leverage) can actually boost the returns on the cash you personally put into a deal.

Using Leverage to Amplify Your Returns

If you've been following the examples, you’ve seen one of real estate's most powerful wealth-building tools in action: leverage. Put simply, leverage is just using borrowed money—in this case, a mortgage—to buy and control an asset that’s much more expensive than the cash you have on hand.

It’s the secret sauce that explains why a financed property, even with less cash flow after paying the mortgage, can deliver a much higher cash-on-cash return than buying the same property with all cash.

Think of it like using a long pry bar to move a giant boulder. With your bare hands (your cash), you can’t budge it. But with the right tool (the loan), you can move something immense. That’s what a mortgage does for your investment capital; it magnifies its power.

When you finance a property, you drastically reduce the "Total Cash Invested" figure in the cash-on-cash formula. Since that number is the denominator, making it smaller makes your final return percentage much, much bigger. It supercharges the return on every single dollar you put into the deal.

Leverage in Action: A Direct Comparison

Let's put this into perspective with a simple side-by-side.

Imagine two investors are looking at identical $400,000 properties. Let's say both properties generate $15,000 in net operating income (cash flow before any loan payments).

Investor A buys with all cash. They invest the full $400,000. Their cash-on-cash return is $15,000 / $400,000, which comes out to 3.75%. Not bad, but not amazing.

Investor B uses financing. They put down 20% ($80,000) and get a mortgage for the rest. After their mortgage payments, their annual cash flow is now only $7,000. But look at their return: $7,000 / $80,000 = 8.75%.

Investor B is actually putting less cash in their pocket each year, but their initial investment is working more than twice as hard. That’s the magic of leverage.

"The impact of leverage on cash-on-cash returns demonstrates why financing strategies are critical for residential property investors, as borrowing can significantly amplify returns on equity invested. For instance, a $1 million property generating $70,000 annually yields a 7.0% return with an all-cash purchase. However, adding a $500,000 loan at 5% interest raises the cash on cash return to 9.0% on the remaining equity, showcasing what experts call 'the effect of leverage.'" You can explore more expert insights on how leverage affects real estate returns at jpmorgan.com.

This is exactly how savvy investors build portfolios. Instead of tying up all their capital in one property, they can spread it across multiple deals, growing their asset base much faster.

Of course, leverage isn't without risk. You still have to make that mortgage payment every month, whether the property is rented or not. That’s why it’s so important to understand your financing options inside and out. If you're curious, we break down several approaches in our guide on how to finance a rental property with seven proven strategies.

When it comes down to it, using debt wisely is a true cornerstone of building wealth in real estate.

Why Cash on Cash Return Isn't the Whole Picture

Cash on cash return is a fantastic tool, no doubt. It tells you exactly how much cash your initial investment is spinning off each year. But relying on it alone is a bit like driving a car while only looking at the speedometer—you know your current speed, but you're missing the bigger picture of the road ahead, the fuel in your tank, and the overall health of your engine.

A truly successful real estate investment is about so much more than the cash it generates in a single year. While the cash on cash metric gives you a critical snapshot of your annual performance, it deliberately leaves several key wealth-building factors out of the frame.

To make smart, long-term decisions, you have to understand what this number isn't telling you.

What the Metric Misses

The laser-like focus of cash on cash return is both its greatest strength and its most significant weakness. By design, it ignores several other powerful ways your investment generates wealth over time.

Here are the three main components it doesn't capture:

Property Appreciation: This is the slow, steady increase in your property's market value. This "silent" return doesn’t hit your bank account annually, but it can represent a massive chunk of your total profit when you eventually decide to sell.

Equity Buildup: Every time you make a mortgage payment, a portion of it goes toward the principal. That directly reduces your loan balance and increases your ownership stake—your equity. Think of it as a forced savings account that cash on cash return simply doesn't track.

Tax Benefits: Real estate comes with some serious tax advantages, with depreciation being the headliner. This allows you to deduct a portion of the property's value from your taxable income each year, potentially saving you thousands of dollars without impacting your actual cash flow.

While an 8-12% cash on cash return is a solid target, context is everything. A property with a 4% return could be a phenomenal long-term investment if it's in a rapidly appreciating market. On the other hand, a property showing a 14% return in a stagnant area might end up being a disappointment down the road. This is because the metric only captures one year's cash flow, completely missing the bigger story of market growth and equity. To learn more about these nuances, you can find some great insights on evaluating real estate returns on innago.com.

A More Complete View

To get a true feel for an investment's potential, experienced investors always pair cash on cash return with other key metrics.

Cash on cash return tells you how hard your cash is working. Other metrics tell you how hard the asset itself is working.

Think of it like assembling a team of specialists. Each metric has a specific job, and together, they give you a complete diagnostic. By looking at metrics like Capitalization Rate (Cap Rate) and Total Return on Investment (ROI) alongside your cash on cash return, you build a much more robust and strategic view of your rental property’s performance.

This table gives a quick rundown of what each metric is best for.

Comparing Key Real Estate Investment Metrics

Metric | What It Measures | Best For |

|---|---|---|

Cash on Cash Return | The annual cash flow generated relative to the actual cash you invested. | Evaluating the performance of your cash investment in a single year, especially when using leverage (a loan). |

Cap Rate | The property's unleveraged annual return, assuming an all-cash purchase. | Quickly comparing the raw income potential of similar properties in a specific market, regardless of financing. |

Total ROI | The total profit (cash flow, appreciation, equity) over the entire holding period relative to the initial investment. | Getting the full picture of an investment's performance from purchase to sale, including all wealth-building factors. |

By using these metrics together, you move from just seeing your current speed to having a full dashboard that helps you navigate your entire investment journey.

Practical Ways to Boost Your Cash on Cash Return

Knowing your cash-on-cash return is just the starting line. The real magic happens when you start improving it. At its core, boosting this key metric is about one thing: increasing your annual cash flow. You get there by working both sides of the coin—bringing more money in and letting less money out.

Every little tweak can have a surprisingly big effect on your final percentage. Let's dig into some proven, real-world strategies that experienced landlords use to make their invested capital work harder for them.

Strategies for Increasing Rental Income

The most obvious path to a better return is to make your property generate more income. This is about more than just hiking the rent; it's about adding real value and keeping the property occupied.

A smart approach here can be a game-changer. Consider these tactics:

Strategic Rent Increases: Don't just pick a number out of thin air. Do your homework on local market rates to make sure your pricing is competitive yet fair. Small, consistent annual increases are usually much easier for tenants to swallow than a single massive jump.

Add New Revenue Streams: Get creative. Can you offer tenants something extra they'd be willing to pay for? Think about adding reserved parking spots, allowing pets for a monthly fee, or installing coin-operated laundry machines. These small additions can really add up.

Focus on Tenant Retention: Nothing destroys cash flow faster than a vacant unit. Happy tenants stay longer. By responding to maintenance requests promptly and offering renewal incentives, you can slash the expensive costs of tenant turnover, like marketing and cleaning fees.

A 5% increase in tenant retention can boost profitability by 25% to 95% in many industries. While that's not a real estate-specific stat, the principle is universal: keeping good tenants is one of the most profitable things you can do.

Methods for Reducing Operating Expenses

Now for the other side of the equation. Every dollar you trim from your operating expenses goes directly into your pocket, beefing up your pre-tax cash flow and your cash-on-cash return.

Proactive management is your best friend here. It’s all about cutting costs without cutting corners on quality. Here’s where to start:

Refinance Your Mortgage: This is one of the biggest levers you can pull. If interest rates have dropped since you secured your loan, refinancing could dramatically lower your monthly mortgage payment and give your cash flow an instant lift.

Appeal Your Property Taxes: Tax assessments aren't always set in stone. If you have good reason to believe your property's assessed value is too high, filing an appeal is well worth the effort and can lead to significant savings year after year.

Implement Proactive Maintenance: Waiting for the water heater to burst is a recipe for a budget disaster. A scheduled maintenance plan lets you spot and fix small problems before they become costly emergencies, saving you a fortune in the long run.

Your Top Questions Answered

Let's dive into a few of the most common questions investors ask about cash-on-cash return. Getting these details straight will help you use this metric like a seasoned pro.

What's a Good Cash on Cash Return, Really?

There’s no single magic number, but most experienced investors will tell you that a cash-on-cash return between 8% and 12% is a great target for a residential rental. Landing in that zone usually means you've found a healthy, cash-flowing property.

But here's the reality: what’s “good” completely depends on your market, your comfort with risk, and what you’re trying to achieve. In a hot market where prices are climbing fast, you might be perfectly happy with a lower return—say, 5-7%—because you're banking on making a big profit when you eventually sell. On the flip side, in a slower, more stable market, you’ll want to see a higher percentage to make the investment worth your while.

Your best move is always to measure your property's performance against similar investments in the same neighborhood. A 10% return could be a home run in one city and just average in another.

Does Cash on Cash Return Include Appreciation?

Nope. And this is a critical point to remember. The cash-on-cash return metric is designed with a laser focus on one thing: how hard your actual cash investment is working for you, based purely on the cash flow it kicks off each year.

It purposefully leaves out things like property appreciation, the equity you build as you pay down your loan, and tax advantages like depreciation. That’s actually its biggest strength—it gives you an unclouded view of your property's ability to generate cash right now. Just remember, it isn't the whole story of your investment's overall performance.

How Can a Property Manager Boost My Return?

A great property manager can have a direct and powerful impact on your cash-on-cash return because they are experts at pulling the two main levers in the formula: maximizing income and minimizing expenses. The result is a healthier annual pre-tax cash flow for you.

Here’s how a professional manager makes it happen:

Optimize Your Rental Income: They don't just guess at rental rates. They use hard market data to price your property at the sweet spot—high enough to maximize your revenue but attractive enough to land great tenants without delay.

Slash Vacancy Time: They keep your property filled and earning money through smart marketing, efficient tenant screening, and proactive retention strategies. Every day a unit sits empty is money out of your pocket.

Keep a Lid on Costs: With a network of trusted vendors and a system for proactive maintenance, they handle repairs and upkeep efficiently, preventing small issues from becoming expensive emergencies.

By expertly managing these moving parts, they drive up the "Annual Pre-Tax Cash Flow" number in the equation, which directly pushes your final percentage higher.

At Keshman Property Management, we treat your property like it's our own. With over 20 years of boots-on-the-ground experience, we know how to enhance cash flow and make ownership more profitable and less stressful. Our transparent pricing is designed to ensure you see the maximum benefit from your investment. Learn more about our residential property management services.

Comments