How to Become a Landlord A Realistic Guide

- Sarah Porter

- Aug 31, 2025

- 17 min read

So you're thinking about becoming a landlord. It's a big move, transforming you from a simple property owner into a business operator. This isn't just about collecting rent; it's a hands-on venture that demands sharp financial planning, a solid grasp of the law, and some real people skills. Success starts by treating this like a business from the get-go.

Laying the Groundwork to Become a Landlord

Jumping into real estate investing is an exciting prospect. Done right, it can be a powerful engine for building long-term wealth and generating passive income. But let's be clear: it's not as simple as buying a place and waiting for the checks to roll in. The real pros know that success is built on a bedrock of careful preparation and a deep understanding of what this job really involves.

I always tell new investors to think of it like building a house. You wouldn't pour the concrete without a detailed blueprint, right? The same logic applies here. Your entire rental business will stand on four critical pillars:

Financial Readiness: This is more than just scraping together a down payment. You need to get comfortable with investment loans, learn how to accurately calculate cash flow, and, most importantly, have a healthy cash reserve for those inevitable surprise expenses.

Market Knowledge: You have to become the local expert. That means diving deep into neighborhood trends, knowing the going rate for rent in your target area, and figuring out what kind of property attracts the best tenants.

Legal Compliance: Landlord-tenant law is a minefield. It's complex and varies wildly from state to state, and sometimes even from one city to the next. One small mistake can land you in a world of legal and financial pain.

Property Management Systems: From day one, you need a plan. How will you collect rent? How will you handle repair requests? How will you communicate with your tenants? Winging it is a recipe for disaster; solid processes are what allow you to run efficiently and scale up later.

Before we dive deeper, it helps to see the big picture. This table breaks down the entire process into manageable phases, from your initial idea to the day-to-day realities of being a landlord.

The Landlord Journey at a Glance

Phase | Key Objective | Critical Tasks |

|---|---|---|

Phase 1: Planning & Preparation | Build a solid foundation for your investment. | Define goals, assess finances, research markets, build a team. |

Phase 2: Property Acquisition | Find and purchase a profitable rental property. | Secure financing, analyze deals, make offers, conduct due diligence. |

Phase 3: Tenant Placement | Find and screen high-quality tenants. | Market the property, screen applicants, sign a strong lease agreement. |

Phase 4: Ongoing Management | Operate the property efficiently and legally. | Collect rent, handle maintenance, manage tenant relations, maintain records. |

Think of this table as your roadmap. Each phase builds on the last, and skipping steps is where many new landlords run into trouble.

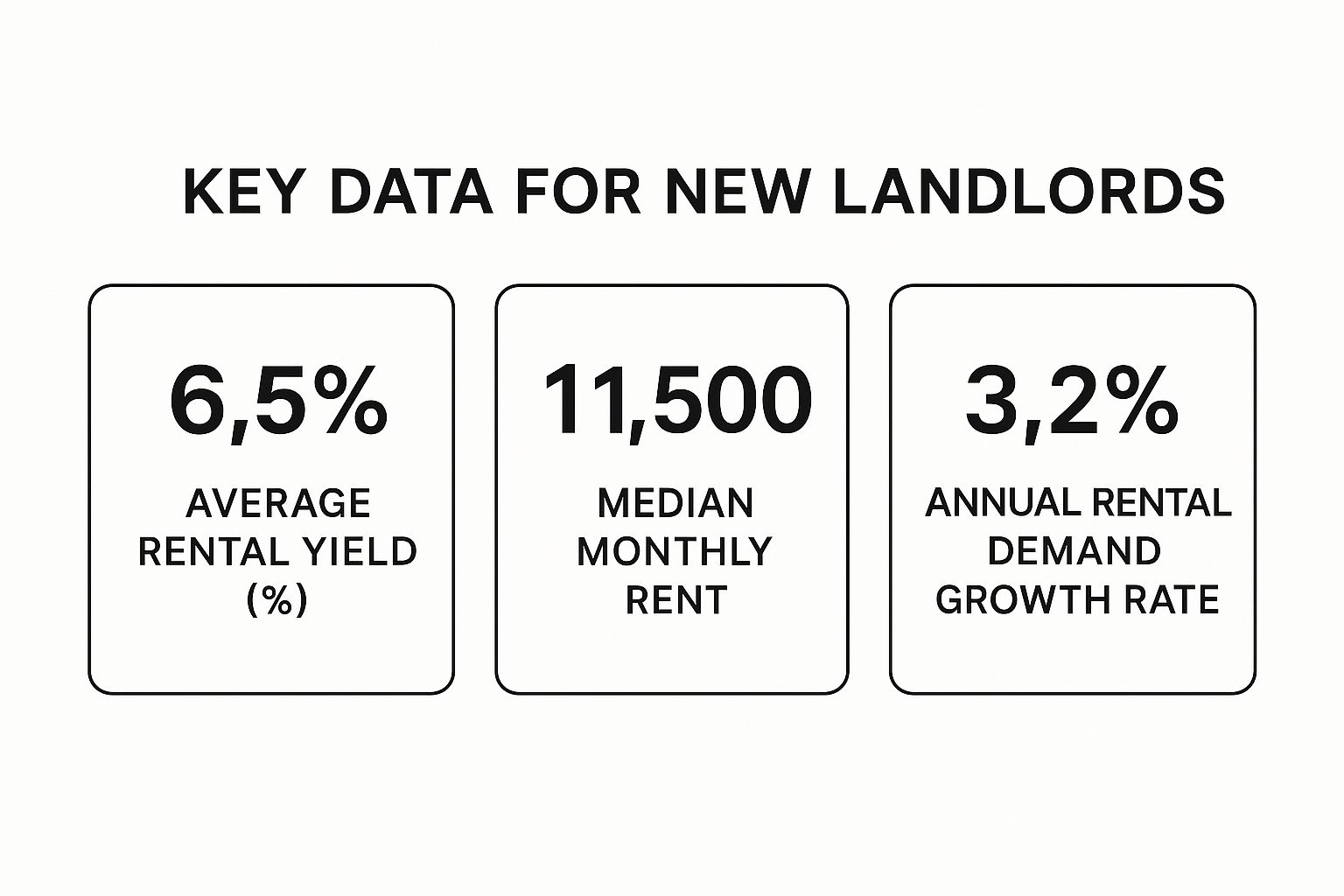

This kind of data is crucial. It shows why you can't just look at the potential rent. You have to balance that income potential (yield and price) with market stability (demand growth) before you ever sign on the dotted line.

Why Become a Landlord Now

Real estate has always been a compelling investment, but the current climate makes it especially interesting. The global housing rental market is already massive, valued at around $1.56 trillion, and it's on track to hit $2.56 trillion by 2032.

What's driving this? A combination of things—more people moving to cities and a big cultural shift where renting offers a flexibility that homeownership doesn't. You can get more details on this rental market expansion from DataIntelo. This isn't a short-term trend; it's a fundamental change in how people live.

At its core, being a landlord is about providing a safe, quality home for someone while building your own financial future. The key is to approach it with diligence, professionalism, and a commitment to continuous learning.

This guide is designed to be your step-by-step playbook, cutting through the noise and confusion. We'll cover everything from how to analyze a deal and get financing to mastering tenant relations and managing your property like a seasoned pro. By focusing on these fundamentals, you can build a rental business that's not just profitable, but resilient.

Getting Your Finances in Order for a Rental Property

Before you fall in love with a property, you need to get your financial house in order. This is, without a doubt, the most critical step. Buying an investment property isn't like buying your own home—lenders see it as a higher-risk venture, and they treat it that way. The bar is set much higher.

Your first move is a deep dive into your own finances. We're talking about polishing your credit score until it shines, whittling down your debt-to-income (DTI) ratio, and building a serious cash cushion. A great credit score isn't just about getting a "yes" from the bank; it directly affects the interest rate you'll be locked into for the next 15 to 30 years. A small difference there can mean thousands of dollars over the life of the loan.

What to Expect From an Investment Property Loan

When you're applying for a loan on a rental, get ready for some serious scrutiny. The two biggest differences you'll notice right away are the down payment requirements and the interest rates. Forget the 3% down you might get on a primary residence.

For a conventional investment property loan, you should expect to bring a down payment of at least 20-25% to the table. Lenders need to see you have significant skin in the game. On top of that, the interest rates on these loans are almost always 0.50% to 0.875% higher than what you'd see for a standard mortgage.

Your financial stability is the foundation of your rental business. Lenders want to see that you can comfortably cover the new mortgage payment in addition to your existing obligations, even without rental income.

This is exactly why having a hefty cash reserve is non-negotiable. Many lenders will want to see proof that you have at least six months' worth of mortgage payments—principal, interest, taxes, and insurance—in the bank for each property you own.

Exploring Your Financing Options

A conventional loan is the most well-trodden path, but it’s far from the only one. Many successful investors I know got their start using creative financing strategies. Knowing your options can open up possibilities you might have dismissed.

Here are a few popular ways to finance your first rental:

"House Hacking" with an FHA Loan: This is a brilliant way for new investors to get started. An FHA loan lets you buy a multi-family property (from two to four units) with as little as 3.5% down, on one condition: you have to live in one of the units for at least a year. The rent from the other units can then cover a huge chunk, if not all, of your mortgage.

Tapping into a HELOC: If you've built up a good amount of equity in your own home, a Home Equity Line of Credit (HELOC) can be a fantastic tool. It works like a credit card that’s secured by your house, giving you access to cash you can use for a down payment on a rental.

Trying Seller Financing: This one is less common, but it's a gem when you can find it. Sometimes, a seller is willing to act as the bank and finance the purchase for you. This allows you to negotiate terms directly and potentially sidestep the rigid underwriting process of a traditional bank.

Calculating the Real Cost of Ownership

Getting approved for the loan is just the start. One of the biggest mistakes I see new landlords make is underestimating all the other costs that come with owning a rental. The mortgage is just the baseline; your actual profit lives or dies by how well you forecast all your expenses.

Let’s run some quick numbers. Say you're looking at a duplex for $400,000. You put 25% down ($100,000), and your mortgage payment (PITI) comes out to $2,200 per month. You can rent each unit for $1,600, bringing in a total of $3,200 a month. That looks like a $1,000 monthly profit, right?

Not so fast. Now we have to factor in the real-world costs:

Vacancy (5-10%): You have to assume the property won't be rented 100% of the time. Let's budget 8%, which is $256/month.

Repairs & Maintenance (5-10%): Things break. A leaky faucet, a broken dishwasher—it all adds up. Budget another 8%, or $256/month.

Capital Expenditures (CapEx) (5-10%): These are the big-ticket items: a new roof in five years, an HVAC system in ten. You have to save for them. Let's set aside another $256/month.

Property Management (8-12%): Even if you manage it yourself, your time has value. It’s smart to budget for this cost regardless. At 10%, that's $320/month.

Suddenly, those "hidden" costs add up to $1,088 a month, wiping out your entire $1,000 profit and putting you slightly in the red. This is why you must learn to analyze a deal properly. When you master these numbers, you stop gambling and start investing with confidence.

How to Find and Analyze Your First Investment Property

This is where the rubber meets the road. All the planning in the world means nothing until you find an actual property. It can feel like a treasure hunt, but I promise you, success isn't about luck. It's about having a disciplined, repeatable strategy. Forget about mindlessly scrolling through real estate apps for hours. The pros know exactly what they're looking for before they even start the search.

Nail Down Your "Buy Box" First

Your first move? Create an investment "buy box." This is simply a non-negotiable set of criteria that defines your perfect property. Think of it as a personal filter that keeps you laser-focused and stops you from getting sidetracked by a "deal" that's completely wrong for your goals.

A solid buy box should include:

Property Type: Are you after a single-family home in a quiet suburb? Or maybe a duplex near a university? Each has its own playbook.

Location: Get specific. Don't just say "a good neighborhood." Define what that means to you. Is it about certain school districts, being close to major employers, or having verifiable low crime rates?

Price Range: Based on your financing, what's your absolute ceiling? More importantly, what's the sweet spot where you believe you can find the best cash flow?

Tenant Profile: Who are you renting to? Young families? College students? Working professionals? The property you buy has to appeal directly to that crowd.

Once your buy box is clearly defined, you can sift through dozens of listings in minutes. It makes it easy to instantly discard the ones that don't fit and focus only on the real contenders.

Uncovering Deals Beyond the Obvious

Let's be honest: the best deals are rarely the ones everyone else is looking at. While online listing services are a decent starting point, if that's all you're using, you're competing with every other buyer in town. To get an edge, you have to look where others aren't.

This really boils down to building a network. The single best thing you can do is find a real estate agent who is investor-savvy. I’m not talking about the agent who helps people buy their dream homes; you need someone who understands cash flow, knows how to spot a good rental, and often hears about off-market deals before they ever hit the public sites.

And don't be afraid to get your hands dirty. The old-school method of "driving for dollars" still works wonders. You literally drive through your target neighborhoods looking for properties that look neglected—think overgrown lawns, boarded-up windows, or mail piling up. A little detective work can help you find the owner, and you might just get to make an offer before anyone else even knows it's for sale.

Analyzing a property is a numbers game, but finding one is a people game. The more connections you make with agents, wholesalers, and other investors, the more deal flow you'll create for yourself.

Remember, market conditions are always shifting. The U.S. national median rent recently hovered around $1,373, which is a slight dip of 0.6% year-over-year but still $225 higher than it was in early 2021. This tells us that while things might be rebalancing, the demand for housing remains strong—a crucial factor for any new landlord. You can dive deeper into the latest rental market trends from Resimpli to see how your local area stacks up.

Your Essential Due Diligence Checklist

So you've found a promising property and the seller accepted your offer. Great! But the real work is just beginning. This is the due diligence period, and it’s your last chance to uncover any hidden nightmares before you're legally on the hook. Rushing this step is a classic rookie mistake that can cost you tens of thousands of dollars down the road.

Your due diligence checklist needs to be thorough. Here are the absolute must-dos:

Professional Home Inspection: This is completely non-negotiable. A qualified inspector will crawl through every inch of that property, checking the roof, foundation, HVAC, electrical, and plumbing, and give you a detailed report.

Review All Documents: Scrutinize every single piece of paper. This means the seller's disclosures, any existing leases if the property is already tenanted, and the HOA documents if there is one. Look for weird rules, restrictions, or upcoming special assessments.

Verify Zoning and Local Ordinances: Head down to the city planning department or check their website. You need to be 100% sure the property is legally zoned for rental use and learn about any local rules that could derail your plans, like restrictions on short-term rentals.

Get Insurance Quotes: Don't just guess what your landlord insurance will cost. Get actual quotes from a few different providers so you can plug a real number into your final cash flow calculations.

Estimate Repair Costs: Using that inspection report, get quotes from a couple of contractors for any necessary repairs. This gives you powerful leverage to go back to the seller and renegotiate the price or ask for credits at closing.

Navigating this part of the process carefully is what separates successful investors from the ones with horror stories. Take your time here. It protects your investment and truly sets you up for long-term success.

Finding and Screening High-Quality Tenants

You can have the most beautiful property on the block, but its success as an investment comes down to one thing: the person who lives in it. Landing a high-quality tenant is, without a doubt, the most critical job you have as a landlord.

A great tenant pays on time, treats your property like their own, and generally makes your life easier. A bad one? They can single-handedly turn your asset into a nightmare of missed payments, damaged walls, and stressful legal battles.

This isn't about crossing your fingers and hoping for the best. It's about building a solid, fair, and legally sound system that attracts the right people and filters out the wrong ones. Let's walk through how to build that system.

Crafting a Rental Listing That Works for You

Think of your rental ad as your first line of defense. A lazy ad with dark, blurry phone pictures tends to attract applicants who are just as careless. A professional, detailed listing, however, sends a clear message: you're a serious landlord who expects a responsible tenant.

Start with great photos. Open the blinds, shoot during the day, and show off the best features of the space.

Your listing itself needs to include a few key things:

A Catchy, Descriptive Headline: Don't just say "2 Bed/1 Bath for Rent." Try something like, "Bright & Spacious 2-Bedroom with Private Balcony Near Downtown." It paints a picture.

A Detailed Description: Go beyond the basics. Talk about the "stainless steel appliances," the "newly renovated bathroom with subway tile," or the "fenced-in backyard perfect for a small dog." These details help potential tenants imagine themselves living there.

Clear Rental Terms: Be upfront about the monthly rent, security deposit, lease length, and your rules on pets or smoking. Transparency saves everyone a ton of time.

To get the most eyeballs on your listing, post it everywhere. Zillow, Apartments.com, and even Facebook Marketplace are the big players you can't afford to ignore.

Establishing Your Standardized Screening Process

When it comes to screening tenants, consistency is your best friend. To stay on the right side of the Fair Housing Act, you must apply the exact same screening criteria to every single applicant, no exceptions. This protects you from claims of discrimination and forces you to make a sound business decision, not an emotional one.

Your screening criteria should be written down before you even post your ad. This isn't just a good idea—it's your legal shield. It proves you have a consistent, non-discriminatory process for evaluating every application that comes your way.

Your standards need to be objective and measurable. Here’s a common and effective set of criteria:

Income Verification: The gold standard is that an applicant's gross monthly income should be at least 3x the monthly rent. You'll want to verify this with recent pay stubs or an official offer letter.

Credit Score Minimum: Set a reasonable floor for a credit score, like 650 or higher. This is a quick way to gauge an applicant's history of financial responsibility.

Clean Background Check: This report will flag any relevant criminal history or, crucially, past evictions. A prior eviction is one of the biggest red flags you can find.

Positive Landlord References: This is where the real story comes out. Talking to past landlords is arguably the most insightful part of the entire process.

How to Conduct Reference Checks That Actually Tell You Something

Never, ever skip the reference check. A credit report shows you how someone handles their bills, but a former landlord can tell you how they'll actually treat your property. When you call, you aren't just confirming dates; you're digging for the truth.

Here are the questions I always ask to get beyond a simple "they were fine":

"Can you confirm they lived at Address] from Start Date] to End Date]?"

"Did they consistently pay their rent on time?"

"Did they provide proper notice before they moved out?"

"How did they maintain the unit? Was there any damage beyond normal wear and tear?"

"Were there ever any complaints from neighbors about noise or other issues?"

And the million-dollar question: "Would you rent to them again?"

That last answer tells you everything. A moment's hesitation is as telling as a direct "no."

By combining a great ad with a rigorous, fair, and consistent screening process, you stack the deck in your favor. You dramatically increase your odds of finding a fantastic tenant who will protect your investment and make your journey as a landlord a profitable—and positive—one.

Managing Your Property and Lease Agreements

Finding a great tenant is a huge milestone, but this is where the real work begins. Now, the game shifts from finding and marketing a property to the day-to-day operations that make or break your investment. This is all about having solid systems, clear communication, and, above all else, a rock-solid lease agreement.

Think of your lease as the constitution for your rental. It's the single most important document you have, laying out the rules, responsibilities, and expectations for both you and your tenant. One of the biggest mistakes I see new landlords make is grabbing a generic template from the internet. That's a huge risk. Landlord-tenant laws are incredibly specific to your state and even your city, and a flimsy lease will leave you completely exposed.

Crafting a Bulletproof Lease Agreement

Your lease absolutely must be state-specific. Better yet, have it reviewed by a local real estate attorney. That small upfront investment is nothing compared to the nightmare of a legal dispute down the road. An attorney ensures your agreement is not just thorough but fully enforceable in court.

A strong lease has to nail down a few key areas:

Security Deposit Clause: Be crystal clear on the exact amount, where it will be held (some states have specific rules for this), and the precise conditions for its return. You need to outline what you consider "normal wear and tear" versus actual damage—this is one of the most common points of conflict.

Rent Collection Policy: Detail the rent amount, the due date, and how you'll accept payments. It’s also crucial to spell out your late fee policy, including any grace period and the exact penalty, making sure it complies with state law.

Maintenance and Repair Procedures: Who fixes what? The lease should explain how tenants submit maintenance requests and what they can expect from you in terms of response time for both emergency and non-emergency issues.

Rules and Regulations: This is where you cover the nitty-gritty: pets, smoking, long-term guests, and any property alterations. Don't be vague. A pet policy, for instance, should detail the type, size, and breed of animal allowed, plus any associated pet rent or deposit.

Systems for Smooth Day-to-Day Management

Once the lease is signed, your success boils down to efficiency. You want to automate whatever you can to free up your time and make life easier for your tenants. Clunky, manual processes just create frustration for everyone.

Think about it: collecting rent via check is a relic of the past. It’s slow and inefficient. Today, smart landlords use online payment portals. These platforms let tenants set up automatic payments, which dramatically cuts down on late or missed rent. Plus, it gives you a clean digital record of every transaction for your books.

Apply that same thinking to maintenance. Instead of a jumbled mess of texts and phone calls, create a dedicated system. A simple online form or a specific email address for maintenance requests ensures everything is documented with a timestamp. Nothing falls through the cracks, and it creates a professional process that good tenants really appreciate.

Your goal as a landlord isn't just to manage a building; it's to run a business. Putting clear, consistent systems in place for rent, maintenance, and communication is what separates professional investors from overwhelmed amateurs.

Finally, make a point to schedule periodic inspections, as allowed by your lease and local laws. This isn’t about being nosy. A semi-annual check-in to replace smoke detector batteries and look for slow leaks under sinks shows you're a proactive owner. It’s your chance to catch small issues before they snowball into expensive disasters.

Knowing When to Hire a Property Manager

As your portfolio grows, the question of hiring a property manager will eventually pop up. It’s not an admission of failure—for many successful investors, it's a strategic move that allows them to scale without getting buried in the daily grind.

A property manager typically handles it all: marketing vacancies, screening applicants, handling leases, collecting rent, and coordinating every last repair. They become the primary contact for your tenants, freeing you up to focus on finding the next deal. This service, of course, comes at a cost, usually 8-12% of the monthly rent plus a fee for placing a new tenant.

The decision really boils down to a trade-off: your time versus your money. If you have a demanding day job or live hours away from your rental, a manager might be a necessity from the start. But if you only have one or two local properties and don't mind the hands-on work, self-management can definitely maximize your cash flow.

The property management industry is huge and growing for a reason. The U.S. market is projected to expand from $81.52 billion to nearly $99 billion by 2029, with over 720,000 people working in residential management alone. This shows that as landlords scale, professional management often becomes a crucial part of their strategy. For a deeper dive, check out these insightful property management statistics on DoorLoop.com. The trend is clear: managing a portfolio is a specialized skill, and knowing when to delegate is just as important as knowing how to do it yourself.

Common Questions About Becoming a Landlord

Jumping into property investment always brings up a handful of big, practical questions. Once you get past the initial excitement, the real-world "what ifs" start to surface. Let's tackle some of the most common ones I hear from first-time landlords.

How Much Profit Can I Realistically Make from One Rental Property?

This is the million-dollar question, isn't it? The answer really depends on your market, the property itself, and how you financed the deal. A good rule of thumb many investors aim for is a monthly cash flow of $200 to $500 per door after every single expense is paid. That means after the mortgage, taxes, insurance, and setting aside money for repairs and vacancies.

But cash flow is only part of the story. Your real return on investment comes from a few different places:

Loan Paydown: Your tenant is essentially paying down your mortgage for you every month, building your equity without you lifting a finger.

Long-Term Appreciation: Real estate is a classic long-term game. Over time, property values generally climb, boosting your net worth.

To really understand if a property is a good investment, you need to calculate its Cash-on-Cash Return. This simple metric tells you how much annual cash you’re making compared to the total cash you put in. It's the truest measure of how hard your initial investment is working for you.

What Are the Biggest Legal Mistakes New Landlords Make?

Hands down, the costliest mistakes I see new landlords make are in tenant screening and their lease agreements. It's so easy to accidentally violate the Fair Housing Act. This can be as simple as asking one applicant different questions than another, which can be interpreted as discrimination and lead to massive fines.

The other huge pitfall is grabbing a generic lease template from the internet. Landlord-tenant laws are incredibly specific to your state and even your city. A weak lease will leave you exposed when it comes to security deposit disputes, evictions, or a tenant causing major damage.

A cheap lease template is one of the most expensive mistakes you can make. Always invest in an attorney-reviewed, state-specific lease agreement. It’s the foundation of your legal protection.

How Much Time Does It Actually Take to Manage a Rental Property?

The time you'll spend managing a property can swing wildly. Getting it off the ground—finding, screening, and moving in a new tenant—is the most intense part. Expect that to take 10 to 20 hours over a couple of weeks.

But once you have a solid tenant in place? The ongoing management can be surprisingly light, often settling into just 2 to 5 hours per month. This is mostly for collecting rent and handling minor maintenance calls.

The catch is that one big problem, like an eviction or a burst pipe in the middle of the night, can instantly suck up dozens of hours. The key to keeping your time commitment low is having solid systems. That means streamlined communication, online rent collection, and a go-to list of contractors you trust. Being organized and proactive is your best defense against time-sucking emergencies.

Navigating the complexities of property ownership can be a lot to handle, but you don't have to go it alone. At Keshman Property Management, we use our 20 years of hands-on experience as landlords to make your investment journey less daunting and more profitable. Learn how our transparent, results-driven approach can maximize your earnings by visiting https://mypropertymanaged.com.

Comments