Bookkeeping for Rental Properties Made Simple

- Sarah Porter

- Aug 29, 2025

- 17 min read

Before you log a single rent payment or expense, we need to talk about your financial setup. Getting this right from the start is the single most important thing you can do for your rental business. It's not just about being organized; it's about protecting yourself and creating a clear picture of your investment's health.

Setting Up Your Financial Foundation

Many new landlords skip these first steps, and I can tell you from experience, it always creates headaches later. The goal here isn't to build a complex accounting machine. It's to create a simple, clean system that makes tax time a breeze and shows you exactly how profitable your property really is.

The biggest rookie mistake? Mixing personal and business funds. If you have an LLC, this can actually "pierce the corporate veil," putting your personal assets at risk. A dedicated bank account is your first and best line of defense.

Open a Dedicated Business Bank Account

Seriously, do this before anything else. Open a separate checking account that is used exclusively for your rental property. Every dollar of rent goes in, and every single property-related expense comes out. That's it.

This one simple move brings immediate clarity. When you or your accountant look at that bank statement, there's no question about what's what. You won't be digging through your personal grocery and gas receipts trying to find that one trip to the hardware store from six months ago.

This isn't just for big-time investors. Whether you own one condo or a dozen apartment buildings, this is non-negotiable. The U.S. property management industry is valued at over $81.52 billion and is projected to hit nearly $98.88 billion by 2029. With over 300,000 property management businesses out there, adopting professional habits like this from day one is how you compete and succeed. You can find more industry context in DoorLoop's 2023 property management statistics.

Choose Your Accounting Method

Next, you need to decide how you're going to record your financial activity. This choice affects when you recognize income and expenses, which has a direct impact on your taxes and how you analyze your performance. There are two main flavors: cash and accrual.

Cash Method: This is the most straightforward and the one I recommend for most landlords starting out. You record income when the money physically hits your bank account. You record an expense when the money actually leaves your account. Simple.

Accrual Method: This method is a bit more advanced. You record income when it's earned, not when you're paid. So, January's rent is logged as income on January 1st, even if your tenant pays on the 15th. Likewise, you record expenses when you incur them, not when you pay the bill.

For most independent landlords, the cash method is the way to go. It's intuitive and aligns directly with your bank statement. Accrual can paint a more precise long-term picture, but it adds a layer of complexity that's usually only necessary for larger, more sophisticated operations.

Thinking about which one is right for you? This table breaks down the core differences.

Cash vs. Accrual Accounting for Landlords

Feature | Cash Method | Accrual Method |

|---|---|---|

Income Recognition | Recorded when cash is received | Recorded when rent is earned (due date) |

Expense Recognition | Recorded when cash is paid | Recorded when the expense is incurred |

Simplicity | High. Easy to manage and aligns with bank statements. | Lower. Requires more tracking of receivables/payables. |

Financial Picture | Shows actual cash flow at a specific moment. | Provides a more accurate view of long-term profitability. |

Best For | Independent landlords, small portfolios, simplicity. | Larger property management companies, complex portfolios. |

Tax Implications | Taxes are based on actual cash received/spent in a year. | Taxes may be due on income you haven't received yet. |

Ultimately, the cash method is the practical choice for the vast majority of landlords. It keeps things simple and gives you a real-time pulse on the money moving through your business.

Establish a Chart of Accounts

Don't let the formal name intimidate you. A Chart of Accounts (COA) is just your master list of categories for all your income and expenses. Think of it as the digital filing cabinet for your money. A well-structured COA lets you see exactly where your money is coming from and where it's all going with just a quick glance.

You don't need hundreds of categories. Start with the basics:

Income: Rental Income, Late Fees, Pet Fees, Application Fees

Expenses: Mortgage Interest, Property Taxes, Insurance, Repairs, Maintenance, Utilities, Management Fees

Assets: Business Checking, Security Deposit Account

Liabilities: Mortgage Loan, Tenant Security Deposits

By setting up these "buckets" from day one, you ensure that every transaction has a proper home. This simple framework is the key to generating accurate financial reports and making tax prep painless.

Mastering Income and Expense Tracking

Now that you've got your financial accounts set up, it's time to get into the day-to-day work of rental bookkeeping. This is where the rubber meets the road—turning a shoebox of receipts and a list of rent payments into a clear story of your property's financial health.

Accurate tracking is the absolute backbone of a successful rental business. It shows you what’s really going on with your profitability and makes tax season a breeze instead of a nightmare. This isn't just about noting when the rent hits your account; it’s about capturing every single dollar that flows in and out of your business, from late fees down to a tiny bag of screws from the hardware store.

Logging Every Stream of Income

Rent is the obvious one, but if that’s all you’re tracking, you're leaving money—and valuable data—on the table. Smart landlords know that other revenue streams add up and give a much more accurate picture of a property's true performance.

Make it a habit to log all income the moment it comes in. This includes more than just the basics:

Monthly Rent Payments: The main event. Always note the date, tenant, and property.

Late Fees: If a tenant pays late and your lease has a fee, that's taxable income. Don't forget it.

Pet Fees or Pet Rent: Whether it’s a one-time charge or a monthly add-on, it’s all income.

Application Fees: The money you collect to screen potential tenants counts, too.

Other Income: Think about coin-op laundry, paid parking spots, or even reimbursed utility bills.

Keeping a close eye on your income is crucial right now. The national median rent in the U.S. is sitting at $1,373, and tenant demands are shifting. We're seeing a 20% jump in demand for energy-efficient units and 40% of renters specifically looking for pet-friendly places. These trends directly affect your income and expenses, and solid bookkeeping is how you stay on top of it. You can learn more about what's happening in the rental market on Resimpli.com.

Categorizing Every Deductible Expense

Now for the other side of the coin: your expenses. This is where meticulous bookkeeping really pays off, because every dollar you properly document can lower your taxable income. The goal is simple: capture everything.

Pro Tip: I can't stress this enough—use your dedicated business bank account and credit card for all property-related purchases. It creates an automatic digital paper trail that makes it nearly impossible to miss a deduction when it's time to reconcile your books.

Here are some of the most common expense categories you should have set up:

Mortgage Interest: Usually one of your biggest write-offs.

Property Taxes: Another significant and fully deductible expense.

Insurance: Your landlord, flood, and liability insurance premiums.

Repairs & Maintenance: From fixing a running toilet to patching drywall.

Management Fees: If you use a company to manage your property, their fees are deductible.

Utilities: Any water, gas, or electric bills you pay for the property.

Travel Costs: Don't forget to track the mileage for trips to the property, the bank, or the hardware store. It adds up!

The Critical Difference Between Repairs and Improvements

If you only learn one technical bookkeeping concept, make it this one. Understanding the difference between a repair and an improvement is absolutely essential for any landlord. Getting it wrong is a recipe for expensive tax mistakes.

A repair is something you do to keep the property in its current working order. It’s all about maintenance and fixing things that are broken.

Examples of Repairs: * Replacing a single broken window. * Fixing a leaky faucet. * Repainting a room between tenants. * Getting an appliance fixed.

Repairs are great because they are fully deductible in the year you pay for them. They are considered a standard operating expense.

An improvement, on the other hand, is an expense that adds significant value to your property, extends its life, or adapts it for a new use. It's a betterment, not just a patch-up job.

Examples of Improvements: * Replacing all the old windows with new energy-efficient ones. * Adding a deck. * A full kitchen remodel. * Installing a brand-new HVAC system.

Improvements are handled differently for tax purposes. You don't deduct the full cost upfront. Instead, you capitalize and depreciate the expense. This means you write off a portion of the cost over the asset's useful life—which for a residential rental property is 27.5 years.

Let's walk through a quick scenario. Your tenant calls to say the water heater is on the fritz.

Repair Scenario: You hire a plumber who replaces a broken heating element for $250. That’s a repair. You can deduct the entire $250 from your income this year.

Improvement Scenario: You decide the 15-year-old water heater has had a good run. You replace the whole thing with a modern, high-efficiency tankless model for $2,500. This is an improvement. You can't deduct the $2,500 this year; you'll start depreciating that cost over 27.5 years.

Mastering this distinction is a powerful tool. It allows you to maximize your immediate deductions while keeping you firmly on the right side of tax law.

Choosing Your Bookkeeping System

Picking the right bookkeeping tool for your rentals can feel like a huge decision, but it really just comes down to one thing: What's going to give you the most clarity with the least amount of headache? The perfect system for a landlord with one condo is complete overkill for someone managing 50 units, and vice versa.

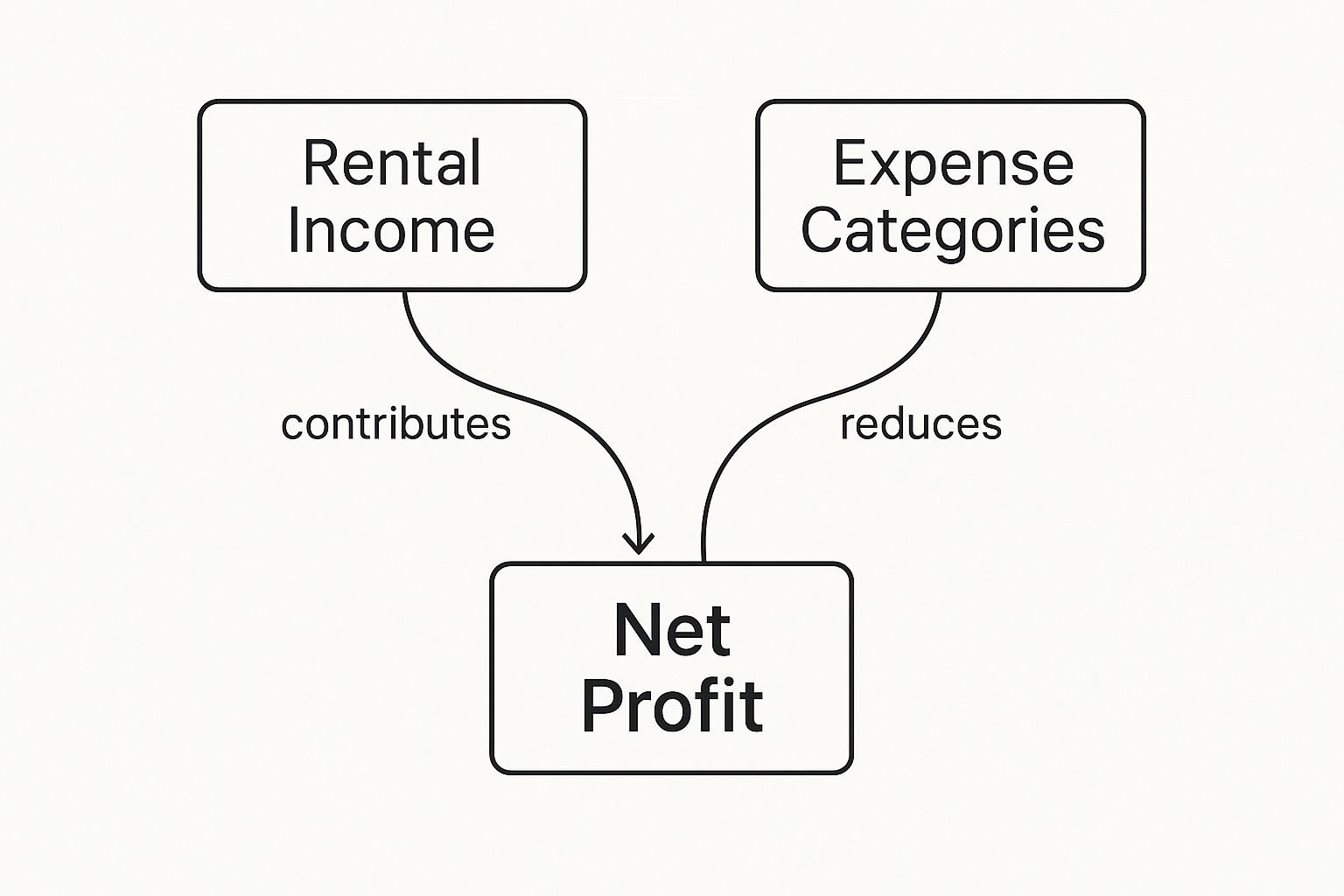

Let's walk through the real-world options you'll encounter.

This simple diagram shows how all the pieces fit together. Every dollar you track—whether it's coming in or going out—flows toward calculating your actual net profit.

No matter what tool you use, this is the core job: giving you a quick, clear snapshot of your rental's financial health.

The Spreadsheet Starter Pack

For landlords just getting their feet wet with a single property, a well-organized spreadsheet is a totally fine place to start. You can set up simple columns for the date, property, category (like rent or repairs), income, and expenses. It’s free, everyone knows how to use it, and it gives you a basic grip on your cash flow.

But this DIY approach has a very hard ceiling. The moment you add a second or third property, that trusty spreadsheet starts to become a liability. Manual data entry is a recipe for typos, pulling reports is a clunky, manual process, and there's no way to automate anything. It quickly becomes a time-suck that leads to missed deductions and a full-blown panic come tax season.

Spreadsheets are a great training ground for learning the fundamentals of tracking income and expenses. But they are a tool you are meant to outgrow. Relying on them for too long is one of the most common mistakes that keeps landlords from scaling their portfolios efficiently.

Dedicated Accounting Software

Once you're ready to graduate from spreadsheets, dedicated accounting software like QuickBooks is the natural next step. Millions of small businesses use these platforms for a reason—they bring a level of automation and professionalism that spreadsheets just can't touch.

With a tool like this, your life gets easier. You can:

Sync Bank Accounts: Automatically pull in transactions from your business bank and credit card accounts, which nearly eliminates manual data entry.

Generate Real Reports: Create professional Profit & Loss statements, balance sheets, and other key financial reports with just a few clicks.

Categorize with Rules: You can set up rules to automatically categorize recurring expenses, like the monthly mortgage payment or insurance bill.

Collaborate with Your CPA: Giving your accountant direct access streamlines everything when it's time to file taxes.

These tools aren't built specifically for landlords, but they can be adapted. For example, you can set up each property as a "class" or "location" to track its individual performance. The main drawback? They don't handle landlord-specific tasks like tracking leases or collecting rent. You'll still be juggling separate processes for those duties.

All-In-One Property Management Platforms

For landlords who want one system to rule them all, an all-in-one property management platform is the final destination. Software like DoorLoop, TenantCloud, or Buildium combines a full-fledged accounting suite with every other tool you need to run your rental business.

This is where rental property bookkeeping becomes truly seamless because these systems were designed from day one for a landlord's workflow. Everything is connected.

The real power of an integrated system comes from its ability to automate the entire tenant lifecycle:

Automated Rent Collection: Tenants pay you online, and the software automatically records the income, applies it to the correct lease, and logs any late fees without you lifting a finger.

Built-in Landlord Reporting: Financial reports are already tailored for real estate, with things like rent rolls and property-specific P&L statements ready to go.

Maintenance & Expense Tracking: You can log a maintenance request from a tenant, assign it to your plumber, and track the associated invoice all in one place.

Lease and Tenant Management: All your tenant data, lease documents, and communication logs are stored right alongside the financial records.

This approach creates a single source of truth for your entire portfolio. While the upfront cost is higher than a simple accounting program, the time you save and the efficiencies you gain often deliver a massive return on investment, especially as you add more doors.

Feature Comparison of Bookkeeping Systems

Deciding which tool is right for you depends heavily on your portfolio size, your budget, and how much time you're willing to spend on administrative tasks. This table breaks down the core differences between the three main approaches.

Feature | Spreadsheets (DIY) | Accounting Software (QuickBooks) | Property Management Software (DoorLoop) |

|---|---|---|---|

Best For | 1-2 properties, new landlords | 2-10 properties, DIY landlords | 3+ properties, growing portfolios |

Cost | Free (or cost of software) | $30 - $90 per month | $59 - $159+ per month |

Automation | None; completely manual entry | High (bank sync, reporting, rules) | Very High (rent collection, late fees) |

Reporting | Manual and basic | Professional financial reports | Landlord-specific reports (rent roll, etc.) |

Tenant Management | Not included | Not included | Fully integrated (leasing, communication) |

Learning Curve | Low | Medium | Medium to High |

Scalability | Poor; becomes unwieldy fast | Good; handles many businesses | Excellent; designed for portfolio growth |

Ultimately, choosing the right system isn't just about solving today's problems—it's about anticipating your future needs and setting yourself up for growth.

Making Sense of Your Financial Reports

This is where all your hard work tracking income and expenses really pays off. Financial reports are what turn all those numbers and receipts into actual business intelligence. They give you the real story of your investment, moving you beyond just a "gut feeling" and into a clear, data-backed view of how your property is truly performing.

Think of these reports as the dashboard for your rental business. They're the difference between glancing at your bank balance and actually understanding your profitability, financial health, and cash movements. Getting comfortable with these documents is a core skill for any serious landlord.

The Income Statement: Your Profitability Scorecard

You'll probably hear this called a Profit and Loss (P&L) statement, and it’s the report you'll likely look at most often. Its job is incredibly simple: to tell you if you're making or losing money over a specific period—be it a month, a quarter, or the full year.

The formula behind it is just as straightforward: Income - Expenses = Net Profit (or Loss).

This report takes all the income you've logged (rent, late fees, you name it) and subtracts every single expense you've tracked (mortgage interest, repairs, insurance, property taxes). The final number at the bottom is the unfiltered truth about your profitability.

So, a monthly P&L for your property at 123 Main Street might look something like this:

Total Income: $2,250 (from rent and pet fees)

Total Expenses: $1,700 (covering the mortgage, insurance, and a minor plumbing fix)

Net Profit: $550

Seeing this one number is incredibly powerful. Is your profit shrinking month over month? Maybe it's time to dig into those rising utility costs or start planning for a strategic rent adjustment next year.

The Balance Sheet: A Snapshot of Your Financial Health

While the P&L shows performance over time, the Balance Sheet gives you a snapshot of your finances at a single moment. It’s a clear-eyed look at what you own and what you owe, painting a picture of your net worth as it relates to the property.

It all boils down to one fundamental accounting equation: Assets = Liabilities + Equity.

Assets: This is the good stuff—what you own. For a landlord, this is the value of the property itself, the cash sitting in your business bank account, and even the security deposits you're holding (for now).

Liabilities: This is what you owe to others. The big one is almost always your mortgage. It also includes things like those security deposits, which you owe back to your tenants.

Equity: This is the magic number representing your actual ownership stake in the property—the difference between your assets and liabilities. As you pay down that mortgage and the property (hopefully) appreciates, your equity grows.

Checking your Balance Sheet quarterly or annually is the best way to see how your investment is maturing and building long-term wealth.

A classic rookie mistake is seeing a healthy bank balance and thinking it's all profit. The Balance Sheet keeps you honest by showing that the cash (an asset) is offset by liabilities like security deposits, which isn't your money to spend.

The Statement of Cash Flows: Following the Money

Honestly, for a landlord's day-to-day survival, the Statement of Cash Flows might be the most important report of all. Profit on paper is meaningless if you don't have enough actual cash to pay the mortgage on the 1st. This report shows you exactly where your cash came from and where it went.

It breaks down your cash movements into three key areas:

Operating Activities: This is the cash flow from your core business. Think rent collected minus real cash expenses paid, like repairs and utilities.

Investing Activities: This bucket includes cash spent on big-ticket items, like buying a new property or a major capital improvement like an HVAC system. It also includes cash you’d receive from selling an asset.

Financing Activities: This section is all about your loans. It tracks the cash you get from the bank when you take out a loan and the principal payments you make on your mortgage.

A healthy rental property has a consistently positive cash flow from operations. That means your day-to-day business is bringing in more cash than it's spending. This report is your early warning system for cash crunches, giving you the foresight needed to keep your rental business afloat and thriving.

Bookkeeping for Short-Term and Vacation Rentals

Managing the books for a short-term or vacation rental is a completely different world than handling a standard long-term lease. The whole rhythm is different. With platforms like Airbnb and Vrbo, you're dealing with a constant, high-turnover flow of guests, and that creates some unique financial wrinkles that your bookkeeping has to be ready for.

Instead of one predictable rent check a month, you've got a steady stream of payouts coming in. The tricky part is that each of those deposits has host service fees, cleaning fees, and other little adjustments already taken out. This makes it surprisingly difficult to see your actual top-line revenue at a glance unless your system is set up to handle this kind of fluctuating income.

The opportunity is huge, no doubt. The global vacation rental market is on a tear, with revenue projected to hit $97.85 billion as the user base expands by over 215 million people by 2029. And while the average revenue per user worldwide is around $117, it jumps to a much healthier $316 here in the United States. You can dig into more of these numbers in these vacation rental statistics on StayFi.com. That kind of money on the table means sharp financial tracking isn't just a good idea—it's essential.

Navigating Platform Fees and Payouts

One of the first things you'll run into is trying to match the gross booking amount with the net payment that actually shows up in your bank account. It's a classic scenario: a guest pays $500 for a weekend stay, but after Airbnb takes its percentage, you only see a deposit for $485.

Your bookkeeping has to account for that difference properly. The right way to do it is to record the full $500 as your gross rental income. Then, you log the $15 platform fee as a separate, and very importantly, a deductible business expense. This two-step process gives you a true picture of your revenue and makes sure you’re claiming every single tax write-off you're entitled to.

Tackling Lodging and Sales Taxes

Here's where things can get complicated. Unlike long-term rentals, short-term stays are often hit with a whole mess of local and state taxes—think transient occupancy taxes (TOT), lodging taxes, or even standard sales taxes. The rules for these can change dramatically from one city to the next, which can be a real headache for hosts.

Some of the big platforms, like Airbnb, might collect and remit these taxes for you in certain areas, but you can’t count on it being universal.

It is your responsibility as the property owner to know the rules for your specific location. Never assume the platform is handling it. Your bookkeeping process must include a clear system for tracking, setting aside, and remitting these tax payments to the correct authorities on time.

Budgeting for Hospitality Expenses

The types of expenses you'll be tracking also look quite different. You’ll have the usual suspects like the mortgage and insurance, of course. But you'll also have a whole new list of recurring costs tied directly to the guest experience, and you need to track these meticulously to understand if you're actually making money on each stay.

Make sure your Chart of Accounts has specific categories for these unique costs:

Cleaning Services: This is a big one. Professional cleaning between every single guest is non-negotiable and will likely be one of your largest operating costs.

Guest Supplies: Think of all the little things that make a stay pleasant—toiletries like soap and shampoo, coffee, and maybe some items for a welcome basket.

Linens and Towels: You have to budget for the inevitable. Linens get worn, towels get stained, and they all need to be replaced regularly to maintain a high standard.

Restocking Amenities: Paper towels, toilet paper, and cleaning supplies seem to disappear into thin air. They need constant replenishment.

By carefully tracking these hospitality-focused expenses, you can get a crystal-clear calculation of your profit margin per booking. That data is gold—it empowers you to make smarter decisions about your pricing strategy in what's often a very competitive market.

Answering Your Top Rental Property Bookkeeping Questions

Even the most organized landlords have questions. When you're managing the books for your rental properties, things pop up, and getting a straight answer can save you a world of headaches, especially when tax time rolls around.

Let's cut through the jargon and get to the practical stuff that helps you run your business better.

How Often Should I Be Doing My Books?

This is a big one. The sweet spot for most landlords is sitting down weekly or bi-weekly. This cadence keeps the task manageable—it’s a small chore, not a massive project. It also means you always have a real-time pulse on your property's financial health, and you won’t be scratching your head trying to remember what that random hardware store charge was for.

If you can't manage weekly, you absolutely must reconcile all your accounts every single month. This is non-negotiable. It means matching up your bank and credit card statements with what you've logged. Believe me, finding a mistake from three weeks ago is simple. Finding it ten months later is a nightmare.

Should I DIY My Bookkeeping or Hire a Pro?

This really boils down to a classic trade-off: your time versus your money, and how confident you feel with the numbers.

If you only have one or two properties and you're comfortable with some basic software, doing it yourself is totally realistic. It's actually a fantastic way to stay deeply connected to how your investment is performing and helps keep costs down when you're starting out.

But once your portfolio starts growing, bringing in a professional bookkeeper—especially one who knows real estate—can be one of the smartest moves you make. They do more than just data entry.

A sharp bookkeeper often pays for themselves, not just by freeing up your time to find the next deal, but by catching deductions you would have missed. If your properties are held in an LLC or a partnership, professional help is pretty much essential to stay compliant.

What Are the Biggest Bookkeeping Blunders Landlords Make?

I’ve seen the same painful (and expensive) mistakes pop up time and time again. Steering clear of these is crucial for protecting your investment and your sanity.

Mixing Money: The cardinal sin is commingling personal and business funds. Using one bank account for everything creates an accounting disaster and can pierce the corporate veil of your LLC, putting your personal assets on the line.

Confusing Repairs vs. Improvements: This is a huge one for taxes. Mistaking a repair (which you can deduct this year) for a capital improvement (which you have to depreciate over many years) can lead to serious trouble with the IRS.

Sloppy Record-Keeping: You have to be able to back up every single deduction you claim. No receipt? No deduction. An auditor will have a field day with undocumented expenses.

Ignoring the Small Stuff: All those trips to Home Depot, the mileage to show a unit, or the coffee you bought for a potential tenant—it all adds up. Forgetting to track these small cash expenses is literally leaving money on the table.

What Paperwork Do I Really Need to Keep?

For your own peace of mind and for audit-proofing your business, organized records are everything. Think of it as building a digital filing cabinet with anything you or your accountant might ever need to see.

Here's your must-have document checklist:

Bank and credit card statements for all dedicated business accounts.

Digital copies of every single receipt and invoice.

Closing statements from your property purchase.

All receipts and records for capital improvements.

Copies of every lease agreement, past and present.

A clear ledger of all rent payments and security deposits received.

The best practice here is to store everything securely in the cloud. This protects you from fires, floods, or a dead hard drive and makes sharing files with your accountant a breeze.

Feeling like you're drowning in the details of bookkeeping and day-to-day management? With over 20 years of experience, Keshman Property Management helps owners make their rentals less stressful and more profitable. We sweat the small stuff so you can focus on the big picture. Find out more about our transparent, owner-focused approach at https://mypropertymanaged.com.

Comments