What Is Effective Gross Income in Real Estate?

- Sarah Porter

- Dec 4, 2025

- 17 min read

Updated: Dec 7, 2025

When you're looking at a rental property, it's easy to get excited by the maximum possible rent you could collect. But as any seasoned investor knows, reality is a bit different. That's where Effective Gross Income (EGI) comes in—it's the figure that truly matters.

Think of EGI as the realistic annual income you can expect from a property after accounting for the inevitable bumps in the road, like empty units and tenants who don't pay. It’s not the pie-in-the-sky number; it’s the property's actual earning power and the starting point for almost every other financial calculation you'll make.

What Is Effective Gross Income in Real Estate?

Let's use an analogy. Imagine you own a small apartment building. If every single unit was rented out for all 12 months of the year with every tenant paying on time, the total rent collected would be your Potential Gross Income (PGI). It's the absolute best-case scenario.

But life happens. A tenant moves out, and it takes a month to find a new one—that's a vacancy loss. Another tenant might fall behind on payments—that's a collection loss. The income you actually collect after these events is what’s effective.

Effective Gross Income bridges that gap. It starts with the property's maximum potential rent and then subtracts the predictable, real-world losses, giving you a much more grounded picture of the revenue you can bank on.

The Core Components of EGI

Getting to EGI is a simple journey from the ideal to the actual. You start with the maximum, subtract the realities, and then add back any extra cash flow.

Starting Point (PGI): This is your 100% occupancy, 100% collection dream number. It’s the total rent you'd get if everything went perfectly.

Realistic Deductions: Here, you account for the fact that units won't always be full and not everyone pays on time. This is your vacancy and credit loss.

Added Revenue Streams: Finally, you account for other ways the property makes money, like laundry machines, parking fees, or pet fees.

EGI is the crucial bridge between a property's theoretical potential and its actual performance. It answers the question, "After accounting for empty units and unpaid rent, how much money is actually coming in?"

This quick table breaks down how each piece fits into the EGI puzzle.

EGI at a Glance

A quick summary of the components used to calculate Effective Gross Income, helping you understand the inputs and their effect on the final number.

Component | What It Means | Effect on EGI |

|---|---|---|

Potential Gross Income (PGI) | The maximum rental income at 100% occupancy. | Starting point; the highest possible value. |

Vacancy Loss | Income lost from unoccupied units. | Decreases the total. |

Collection/Credit Loss | Income lost from tenants who don't pay rent. | Decreases the total. |

Other Income | Revenue from sources like parking, laundry, or fees. | Increases the total. |

Understanding these inputs helps you see exactly where your revenue is coming from—and where it's leaking away.

Why EGI Is a Fundamental Metric

Without a firm grip on EGI, you're flying blind. An investor might see a building with a high potential income and jump at the opportunity, only to find out later that it has a chronic history of vacancies or tenant defaults. The on-paper numbers look great, but the actual performance tells a different, less profitable story.

EGI is so important because it reflects the real-world performance of an asset. For instance, a commercial property with a Gross Potential Rent of $5 million a year might operate in a market with a typical vacancy and credit loss rate of 16%. That translates to a whopping $800,000 in lost income right off the top, bringing the EGI down to $4.2 million before even considering other income sources.

For anyone serious about property ownership, mastering key financial metrics like EGI is one of the most critical real estate investing tips you can learn. If you'd like to explore this concept further, SyndicationPro.com offers additional insights into this core real estate metric.

How to Calculate Effective Gross Income

Figuring out a property’s Effective Gross Income (EGI) isn’t something you need a fancy finance degree for. It's a simple, logical process that takes a property's pie-in-the-sky potential and grounds it in reality. Once you get the hang of the components, you'll be able to quickly size up the real income potential of any rental property.

At its heart, the formula is just common sense:

EGI = Potential Gross Income - Vacancy & Collection Losses + Other Income

Think of this as your financial reality check. You start with the absolute best-case scenario, then subtract the predictable hiccups, and finally add in any extra cash the property brings in. Let's walk through it step-by-step.

Step 1: Start with Potential Gross Income

First things first, you need a starting point. That’s your Potential Gross Income (PGI). This number is the total rent you’d collect if every single unit was occupied at full market value for all 12 months of the year. No vacancies, no discounts, no problems—just pure, maximum earning power.

The math is simple. For a property with identical units, just multiply the number of units by the monthly rent, then multiply that by 12.

PGI = (Number of Units x Monthly Market Rent per Unit) x 12 Months

Let's use a 20-unit apartment building as an example. If the market rent for each apartment is $1,500 a month, the PGI is a cool $360,000 per year (20 units x $1,500 x 12). This is your 100% perfect-world income.

Step 2: Subtract Vacancy and Collection Losses

Now for the reality check. No property is ever 100% full with 100% paying tenants all the time. That’s where Vacancy and Collection Losses come in, and it's the most critical adjustment you'll make.

Vacancy Loss: This is the money you lose when a unit sits empty while you’re trying to find a new tenant.

Collection Loss (or Credit Loss): This is the rent you budgeted for but never received because a tenant defaulted on their payments.

We usually estimate these two combined as a single percentage of the PGI. You can pull this percentage from your own property's history or, if it's a new purchase, look at the average for similar properties in your market. A standard estimate is often in the 5% to 10% range, but this can swing quite a bit depending on the location and how well the property is managed.

For our 20-unit building, let's apply an 8% rate for vacancy and collection loss. That means we need to subtract $28,800 from our PGI ($360,000 x 0.08).

Step 3: Add Other Income Sources

Last but not least, you have to account for all the other ways the property makes money besides rent. This Other Income is often forgotten but can give your bottom line a nice little boost. It’s the cash generated from all the extra services and amenities you offer.

Common sources of other income include:

Parking Fees: Charging for those coveted covered or assigned spots.

Laundry Facilities: The quarters collected from your coin-op washers and dryers.

Pet Fees: That monthly "pet rent" or one-time non-refundable fees.

Storage Unit Rentals: Renting out small storage cages or closets in the basement.

Vending Machines: Your cut from the snack and soda machines in common areas.

Late Fees: The fees collected when tenants pay their rent after the due date.

Let’s say our 20-unit building brings in an extra $7,500 a year from its laundry room, various pet fees, and the occasional late fee. We add this amount back in to get a complete picture of the property's income.

Now that we have all the pieces, we can plug them into the formula and calculate the final EGI for our example building.

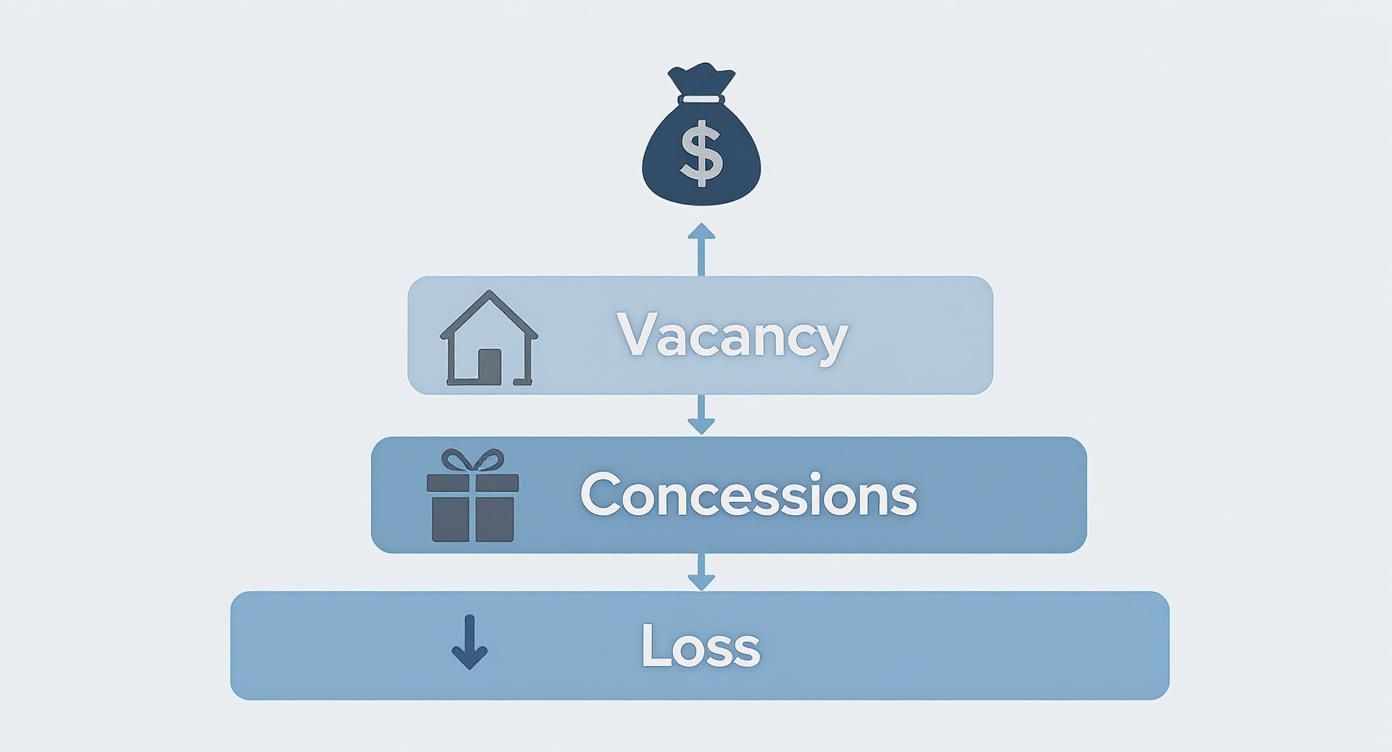

Getting Real About Vacancy Loss and Rent Concessions

The journey from a property's on-paper potential to its actual, in-the-bank income is all about making realistic adjustments. Two of the biggest hurdles you'll account for are vacancy loss and rent concessions. Learning to forecast and manage these is the key to calculating an accurate effective gross income.

Think of your rental property like a hotel. The maximum possible revenue you could earn if every single room was booked every single night of the year is your Potential Gross Income. But in the real world, that rarely happens. Some rooms will be empty between guests (vacancy), and you might offer a special weekend rate to get more bookings (concessions). Both of these realities cut into your maximum profit.

The Inevitable Reality of Empty Units

At its heart, vacancy loss is simply the income you don't earn because a unit is sitting empty. This happens in the gaps between tenants, during a turnover and renovation period, or when the rental market in your area is just plain slow.

A close cousin to vacancy is collection loss (sometimes called credit loss). This is the money you should have received from a tenant, but didn't, because they defaulted on their rent.

For calculation purposes, most investors and property managers lump these two together. We estimate them as a percentage of the property's PGI. This isn't just a random guess, though. It's an educated estimate based on hard data:

Your Property's Track Record: What has your actual vacancy rate been over the past few years?

The Local Market: How do you stack up against the competition? What’s the average vacancy rate for similar properties nearby? You can dig deeper into this by understanding what is occupancy rate and how to track it.

The Building's Condition: Let's be honest—well-maintained, appealing units rent faster and stay occupied longer.

Don't underestimate the impact here. In the U.S. multifamily market, for example, average vacancy rates often fall between 5% and 10%. On a 100-unit building with a $1,200 monthly rent, the PGI is $1.44 million. A 7% vacancy and collection loss wipes $100,800 right off the top. That one line item has a massive effect on your bottom line.

Sweetening the Deal with Rent Concessions

Sometimes, you have to give a little to get a lot, especially when the market is flooded with "For Rent" signs. These incentives are known as rent concessions, and they are a direct reduction of your potential income.

A rent concession is any discount or compromise a landlord offers a tenant to sign or renew a lease. It’s a tool to secure occupancy, but it must be subtracted from your potential income.

You’ve probably seen these in action. Common concessions include:

"One Month Free Rent": The classic offer to get new tenants in the door for a 12-month lease.

Reduced Security Deposits: This lowers the move-in cost, making a unit more accessible.

Waived Amenity Fees: Offering free parking, gym access, or pool use for a few months can be a powerful perk.

Let's say your local market is soft, and you're struggling to fill a unit. You offer one month free on a $1,600/month apartment to a qualified applicant. Great! You landed a tenant. But you absolutely must subtract that $1,600 from your income for the year. If you don't, you're working with an inflated EGI that doesn't reflect reality.

Keeping your units filled is the name of the game. For property owners looking to minimize these losses, it's worth exploring different strategies to market rental properties and fill vacancies fast. By mastering vacancy forecasting and the smart use of concessions, you ensure your effective gross income is a true, reliable measure of how your property is really performing.

EGI vs. PGI vs. NOI: Unlocking Your Property's True Financial Picture

To get a real handle on your property's financial health, you can't just look at one number. You need to understand how the key metrics fit together. Think of it like a financial funnel—each layer filters the numbers, stripping away the "what-ifs" to give you a clearer and more realistic view of your actual profitability.

The three most important layers in this funnel are Potential Gross Income (PGI), Effective Gross Income (EGI), and Net Operating Income (NOI). Getting these mixed up is a classic mistake, one that can seriously skew your analysis of an investment property. Let's break them down.

PGI: The "Perfect World" Scenario

Right at the top of the funnel sits Potential Gross Income (PGI). This is the absolute best-case-scenario number. It's the total income your property could generate if every single unit was rented out for the entire year at the full market rate, with zero vacancies and no one ever missing a payment.

PGI is your optimistic starting point. It’s handy for a quick, high-level comparison between properties, but it tells you nothing about how they actually perform in the real world. Relying only on PGI is like planning your personal budget based on a potential lottery win—it’s a nice dream, but it's not reality.

EGI: Where Reality Kicks In

Next up is Effective Gross Income (EGI), the metric that injects a healthy dose of reality into the numbers. EGI takes that perfect-world PGI and subtracts the inevitable costs of doing business, like vacancy and collection losses. It then adds back any extra cash your property brings in, such as fees from parking spots, laundry machines, or pet rent.

EGI answers the most practical question: "How much income can I actually expect to collect?" It's the critical link between your property's theoretical potential and its real-world ability to generate cash before you start paying the bills.

As this shows, the money you hope to make is always chipped away by practical realities like empty units and the discounts you have to offer to fill them.

NOI: The Bottom Line on Profitability

Finally, at the bottom of our funnel, we have Net Operating Income (NOI). This is what's left after you pay all the necessary operating expenses—the bills that keep the lights on and the property running smoothly. To find your NOI, you just subtract all operating costs (think property taxes, insurance, maintenance, and management fees) from your EGI.

NOI is the single best measure of a property's ability to generate profit from its day-to-day operations. It shows you the cash flow you have before paying your mortgage (debt service) or income taxes.

Investors, lenders, and appraisers all focus heavily on NOI because it reveals the core profitability of the asset itself, separate from how it's financed. Want to go deeper on this final, crucial metric? Check out our complete guide to Net Operating Income.

Comparing Real Estate Income Metrics

To help you keep these straight, here's a side-by-side look at PGI, EGI, and NOI. Seeing them together clarifies how each one tells a different part of your property's financial story.

Metric | Formula Breakdown | What It Measures | Key Use Case |

|---|---|---|---|

PGI | (Total Units × Market Rent) × 12 | The maximum, ideal income at 100% occupancy. | Quickly comparing the theoretical potential of multiple properties. |

EGI | PGI − Vacancy/Collection Loss + Other Income | The realistic revenue you can actually expect to collect. | Creating accurate financial projections and budgeting for the year. |

NOI | EGI − Operating Expenses | The property's profitability from its operations alone. | Valuing a property and determining its cash flow before debt service. |

Each metric builds on the last, taking you from a high-level "what if" to a granular "what is." Mastering all three is fundamental to making smart, profitable real estate decisions.

Actionable Strategies to Increase Your EGI

Knowing how to run the numbers on your Effective Gross Income (EGI) is a great start. But the real magic happens when you start making that number grow. That's where smart property owners separate themselves from the pack.

Boosting your EGI isn’t just about hiking up the rent. Think of it as a two-front battle: you need to plug the leaks that drain your income while simultaneously opening up new channels for revenue to flow in.

This boils down to two key areas of focus: minimizing your vacancy and collection losses and maximizing other income. Nail both of these, and you’ll see a direct, positive impact on your property's performance. Let's dig into how you can actually do it.

Minimize Your Losses and Keep Units Full

Every single dollar you lose to an empty apartment or an unpaid rent check is a direct hit to your EGI. It's a hole in your financial bucket. The best way to patch that hole is through proactive management and building solid tenant relationships.

A stable, occupied property is a profitable one. Simple as that. The game is to find great tenants and keep them happy and paying for as long as possible. This cuts down on your turnover costs—all the cleaning, painting, and marketing that eats up time and money—and erases the vacancy loss that bleeds you dry between residents.

Here are a few tactics that have worked time and time again:

Refine Your Tenant Screening: Your screening process is your first and best defense against future collection problems. Don't just glance at a credit score. You need to verify employment, call their references, and look for a solid history of paying on time. A reliable tenant is worth their weight in gold.

Implement Proactive Maintenance: Nothing sours a good tenant faster than feeling ignored. A dripping faucet or a broken appliance can become a reason to leave. A regular maintenance schedule not only protects your investment but also shows tenants you're on top of things, making them much more likely to stick around.

Offer Smart Renewal Incentives: Don't just wait around for a lease to end and hope for the best. Be proactive. A few months before renewal, offer a small but meaningful incentive—like a gift card, a professional carpet cleaning, or even a smart thermostat upgrade—for signing a new lease early. It's a small price to pay to avoid a costly vacancy.

Maximize Other Income Streams

Once you've tightened up operations and minimized your losses, it's time for the fun part: getting creative. Your property is more than just a collection of apartments; it’s a small ecosystem with untapped revenue potential.

These "other income" sources might seem small individually, but they can add up to a significant amount, giving your EGI a healthy boost. The key is to think about what services or amenities would make life better for your tenants—and what they’d be willing to pay a little extra for.

Maximizing other income is about transforming your property from just a collection of rental units into a service-oriented community. Each new amenity is a new revenue opportunity.

Here are a few popular ideas to get you started:

Laundry Facilities: If you own a multi-family building and don't have on-site laundry, you're leaving money on the table. Clean, reliable, and convenient machines can become a wonderfully consistent source of extra cash flow.

Premium Parking and Storage: Got any extra space? A dusty basement can be converted into secure storage lockers. Those coveted covered parking spots or the ones right by the entrance? Those are premium spots. Charge a monthly fee for them.

Fee-Based Services: Today's renters crave convenience. You can partner with a package locker company, offer pet-friendly units with a monthly "pet rent," or even provide furnished rentals for a higher price point. Each of these services solves a problem for your tenants and adds directly to your bottom line.

By pairing diligent loss prevention with a little creative income generation, you gain real control over your property's financial destiny. These strategies are the key to not just understanding what is effective gross income but actively making it grow. For more on setting the right financial foundation, check out our guide on how to price a rental property for maximum profit.

Common EGI Calculation Mistakes to Avoid

Getting your Effective Gross Income right is the cornerstone of a solid real estate investment. Think of it as the foundation of your financial house—a small crack here can lead to big problems down the line, throwing off your entire forecast and leading to bad decisions.

It’s easy to make a simple mistake that inflates this number, giving you a false sense of security about a property’s performance. Let's walk through some of the most common traps investors fall into and, more importantly, how you can sidestep them.

Relying on Overly Optimistic Vacancy Rates

This is, by far, the most common pitfall. It's so tempting to look at a great property in a hot market and pencil in a tiny vacancy rate like 2% or 3%. But hope isn't a strategy, and this kind of wishful thinking will almost always come back to bite you by overstating your real income.

The Mistake: Pulling a vacancy rate out of thin air or using a "best-case scenario" number instead of one grounded in reality.

How to Fix It: Stop guessing. The first thing you should do is look at the property’s actual vacancy history from the past 2-3 years. Then, validate that data by checking local market reports from property management groups or real estate analytics firms. You need a number that's realistic and defensible, not just optimistic.

Forgetting to Account for Rent Concessions

When you offer "one month free rent" to land a new tenant, that's a direct hit to your bottom line. A classic blunder is to calculate your Potential Gross Income based on the full monthly rent but then conveniently forget to subtract the value of the concession you gave away.

It's simple math, but it's often overlooked. If you give a $1,500 concession for an apartment that rents for $1,500 a month, your total income from that tenant for the year is $16,500—not the $18,000 you might have on your spreadsheet. You have to account for it.

Misclassifying Security Deposits as Income

Let’s be crystal clear: security deposits are not your money. They are a liability you hold in trust for the tenant, meant to cover damages or unpaid rent. Tossing them into the "Other Income" bucket is a serious accounting foul that makes a property look more profitable than it actually is.

Security deposits belong on the balance sheet, not the income statement. The only time a portion of a deposit becomes income is when you legally claim it to cover a specific, documented expense.

It’s always best practice to keep security deposits in a separate account, untouched. In many jurisdictions, this isn't just a good idea—it's the law.

Using Outdated Market Rents

Your entire EGI calculation begins with Potential Gross Income, which is built on what you could be charging for rent. If you're using old numbers, your PGI is wrong from the start, and that error trickles down through every other calculation. Rental markets can shift fast, and last year’s rent roll might as well be ancient history.

The Mistake: Relying on old rent data or a quick Zillow search without digging into what's happening on the ground right now.

How to Fix It: Before any serious financial analysis, run a fresh comparative market analysis (CMA). Find out what similar units in the immediate neighborhood are actually leasing for today. This ensures your PGI is a true reflection of the property's current potential, which in turn makes your EGI far more reliable.

Frequently Asked Questions About EGI

Once you start getting the hang of effective gross income, you'll naturally run into some real-world questions. It's one thing to understand the formula, but it's another to apply it smartly when analyzing a deal or managing your own property.

Let's walk through some of the most common questions that pop up.

What Is a Good Vacancy Rate to Use for EGI?

This is the big one. Your vacancy rate assumption can make or break your financial projections, so getting it right is crucial. But the honest answer is, there's no single "good" rate. The right number depends entirely on the specific property—its location, age, condition, and the local market dynamics.

As a general rule of thumb for a quick, back-of-the-napkin analysis, most investors pencil in something between 5% and 10%. A brand-new, high-end apartment building in a hot neighborhood might realistically hover around 5%. On the other hand, an older building with deferred maintenance in a less competitive area might demand a more cautious estimate of 10% or even higher.

To nail down a number you can actually trust, you need to do a little homework:

Look at the Past: Dig into the property's real performance over the last two or three years. Nothing predicts the future quite like actual history.

Talk to the Pros: Call a few local property managers or commercial real estate brokers. They live and breathe this stuff and can give you a solid feel for the current market average.

Check Market Reports: Big real estate data firms often publish reports on local rental markets. This data can back up what you're hearing on the street.

Remember, using a rosy, overly optimistic vacancy rate is the fastest way to make a bad deal look good. It’s always smarter to be conservative and let the data guide you.

How Often Should I Recalculate EGI?

Your property’s financial picture changes over time, and your EGI calculation should, too. For most rental properties, running the numbers annually is the best practice. This usually lines up perfectly with your year-end accounting and tax prep anyway.

Think of an annual EGI review as a financial check-up for your property. It helps you see how you performed compared to last year, identify trends, and fine-tune your strategy for the year ahead.

That said, there are times you might want to recalculate more often. A major event—like a big local employer shutting down, a massive new apartment complex opening up down the street, or a sudden spike in your own tenant turnover—should trigger a fresh look at your EGI. Staying on top of these shifts lets you react before small problems become big ones.

Can EGI Ever Be Negative?

In theory, yes. In reality, it's incredibly rare and a sign that a property is in deep, deep trouble. For your EGI to dip into negative territory, your total losses from vacancy, non-payment, and concessions would have to be greater than all the rent you could possibly collect.

This scenario is almost unheard of. It would mean the property is sitting nearly empty, the few tenants you have aren't paying, and you're offering massive, unsustainable deals just to get a warm body in a unit. A negative EGI is a five-alarm fire—a clear signal that the asset is failing and needs a massive, immediate turnaround to avoid a complete financial collapse.

At Keshman Property Management, we help property owners navigate these complexities every day. Our goal is to maximize your earnings by minimizing losses and optimizing your property's performance. Learn more about how our expert services can make your investment more profitable and less stressful at https://mypropertymanaged.com.

Comments