How to Check Tenant Credit Score: A Landlord's Guide

- Sarah Porter

- Feb 8

- 13 min read

Updated: Feb 14

When you're looking at a rental application, you're essentially trying to predict the future. Will this person pay on time? Will they take care of the place? The single best tool you have for making that prediction is a tenant credit check. It all starts with getting the applicant's written consent, choosing a solid tenant screening service, and then knowing what to look for in the report.

Why a Tenant Credit Score Is Your First Line of Defense

Let's be honest: your rental property is a major financial asset. Protecting that investment is priority number one, and that protection begins the moment you receive an application. While you'll definitely want to verify their income and check references, a credit report gives you something unique: an unbiased, numbers-based look at how they handle their financial obligations.

It's not about judging someone's past mistakes. It's about risk assessment for your business.

This one step can save you from a world of headaches down the road. A comprehensive screening can instantly show you a history of late payments, an overwhelming amount of debt that could make paying rent difficult, or even collections from past landlords or utility providers. Seeing these things upfront helps you dodge a bullet before it's even fired.

A tenant credit report gives you a clear, objective snapshot of an applicant's financial behavior. I've found it's the most reliable predictor of whether they'll consistently meet their rent obligations, which is crucial for protecting your cash flow.

The data backs this up in a big way. One study found that tenants with credit scores below 600 are 3.5 times more likely to fall behind on rent. The delinquency rate for that group was around 4.14%, a stark contrast to the 1.89% for tenants with scores over 740. For more details on this, you can check out the credit research outlook from State Street Global Advisors. That gap tells a powerful story about the connection between credit history and paying rent on time.

In short, knowing how to properly run a credit check helps you:

Avoid Late or Missed Rent: A track record of on-time payments is the best sign you'll get your rent on time, every time.

Lower Your Eviction Risk: Financially stable tenants are far less likely to end up in a costly and stressful eviction process.

Protect Your Property: I’ve found that people who are responsible with their finances are often just as responsible with someone else's property.

Making a thorough credit check a non-negotiable part of your screening process lays the groundwork for a stable, profitable, and much less stressful experience as a landlord.

Setting the Stage for a Legal and Fair Credit Check

Before you even think about pulling a credit report, your first move—always—is to get the applicant's permission. This isn't just good manners; it's the law. The Fair Credit Reporting Act (FCRA) is very clear on this: you need explicit, written consent from every applicant before you can peek into their credit history.

Trying to skip this step is a surefire way to land in legal hot water. Think of the consent form as your most important document in this whole process. It protects you legally and shows the applicant you're running a professional, by-the-book operation.

Securing Written Consent

A quick verbal "sure, go ahead" won't cut it in court. You need a signature on a piece of paper. This can be a specific section of your rental application or a completely separate form, but it has to be crystal clear.

To be legally compliant, your consent form needs a few key things:

Applicant’s Full Name: Make sure it's an exact match to their photo ID.

Property Address: List the specific unit they're applying for.

Explicit Authorization: Use straightforward language, like "I authorize [Your Name/Company Name] to obtain my consumer credit report for the purpose of tenant screening."

Applicant’s Signature and Date: This is the non-negotiable proof that they agreed.

This simple document is your hall pass. Without it, you're stopped at the door.

Gathering the Right Documents

Along with that signed consent, you'll need to collect a couple of other crucial items. This isn't just about ticking boxes; it's about making sure the screening service pulls the right report for the right person. A simple typo in a name or a wrong birthdate can bring back a report for a completely different individual or, worse, no report at all.

To get it right and stay fair, make sure you ask for:

A Completed Rental Application: This is where you'll find the applicant's full name, address history, job info, and other details needed for the check.

A Government-Issued Photo ID: A driver’s license or passport is perfect. Use it to confirm the person standing in front of you is who they claim to be on the application.

I once had an applicant with an incredibly common name. The only thing that saved us from pulling the wrong file was double-checking the birthdate from his driver's license. It allowed the screening service to pinpoint his exact report, which prevented a major mix-up with someone else who had a terrible credit score.

Key Takeaway: Your process for gathering consent and documents has to be the same for everyone. Consistency is your best friend and your strongest defense against any accusations of discrimination. Apply your rules to every single applicant, every single time. No exceptions.

Nailing this initial stage of gathering consent and verifying identity is absolutely non-negotiable. It creates the legal and ethical foundation for everything that follows, protecting both you and your potential tenant down the line.

Choosing Your Method: Credit Bureaus vs. Tenant Screening Services

Okay, you've got the signed consent form in hand. Now comes the critical decision: how will you actually run the credit check? You have two main paths, but from my experience, one is a whole lot smoother for landlords.

You could try going straight to one of the big three credit bureaus—Experian, Equifax, or TransUnion. But be warned, this route is often a bureaucratic nightmare for an independent landlord. It usually involves a mountain of paperwork, a rigorous credentialing process, and sometimes even a physical inspection of your "office" (which might just be your kitchen table).

The much saner and more practical option? Use a service built specifically for landlords.

The Clear Advantage of Specialized Screening Services

Platforms like SmartMove (from TransUnion), MyRental, or RentPrep are designed with our needs in mind. They don't just spit out a credit score; they deliver a complete picture of your applicant.

Here’s what you typically get in one tidy package:

Full Credit Reports: A detailed look at an applicant's financial history, not just a three-digit number.

Nationwide Criminal Background Checks: A search that goes beyond just the local courthouse.

Eviction History: The ultimate red flag. This report shows if they have a history of being removed from a property.

One of the best parts is how they handle the inquiry. Most of these services use a tenant-initiated process, which results in a soft credit pull. This is a huge plus because it doesn't ding the applicant's credit score—a real selling point for those highly qualified tenants who are likely applying for a few different places.

Using a dedicated service makes it so much easier to legally and efficiently check a tenant's credit without all the red tape. If you want to explore the top platforms out there, we've broken down the 12 best tenant screening services for landlords in 2025.

To help you visualize the difference, here’s a quick comparison of your two main options.

Tenant Screening Methods Compared

Feature | Direct Credit Bureau | Tenant Screening Service |

|---|---|---|

Process Complexity | High (credentialing, inspections) | Low (simple online setup) |

Report Type | Credit report only | Comprehensive (credit, criminal, eviction) |

Credit Inquiry | Often a hard inquiry (can lower score) | Usually a soft inquiry (no impact on score) |

Cost | Varies, can have setup fees | Typically $25 - $55 per applicant, often paid by the tenant |

Turnaround Time | Can take days or weeks for setup | Usually instant or within a few hours |

Ultimately, a tenant screening service is almost always the more efficient, comprehensive, and applicant-friendly choice for landlords.

Making the Right Choice for Your Property

As you compare services, think about your budget and how much information you really need. The process is straightforward: you get the applicant's FCRA-compliant authorization, choose your service, and then review the results. The cost often lands around $40 per report.

Keep this in mind: historical data from TransUnion shows that tenants with credit scores above 650 are linked to 95% on-time rent payments. A solid screening process can drastically cut down on vacancy losses, which have historically averaged 7.2% for landlords.

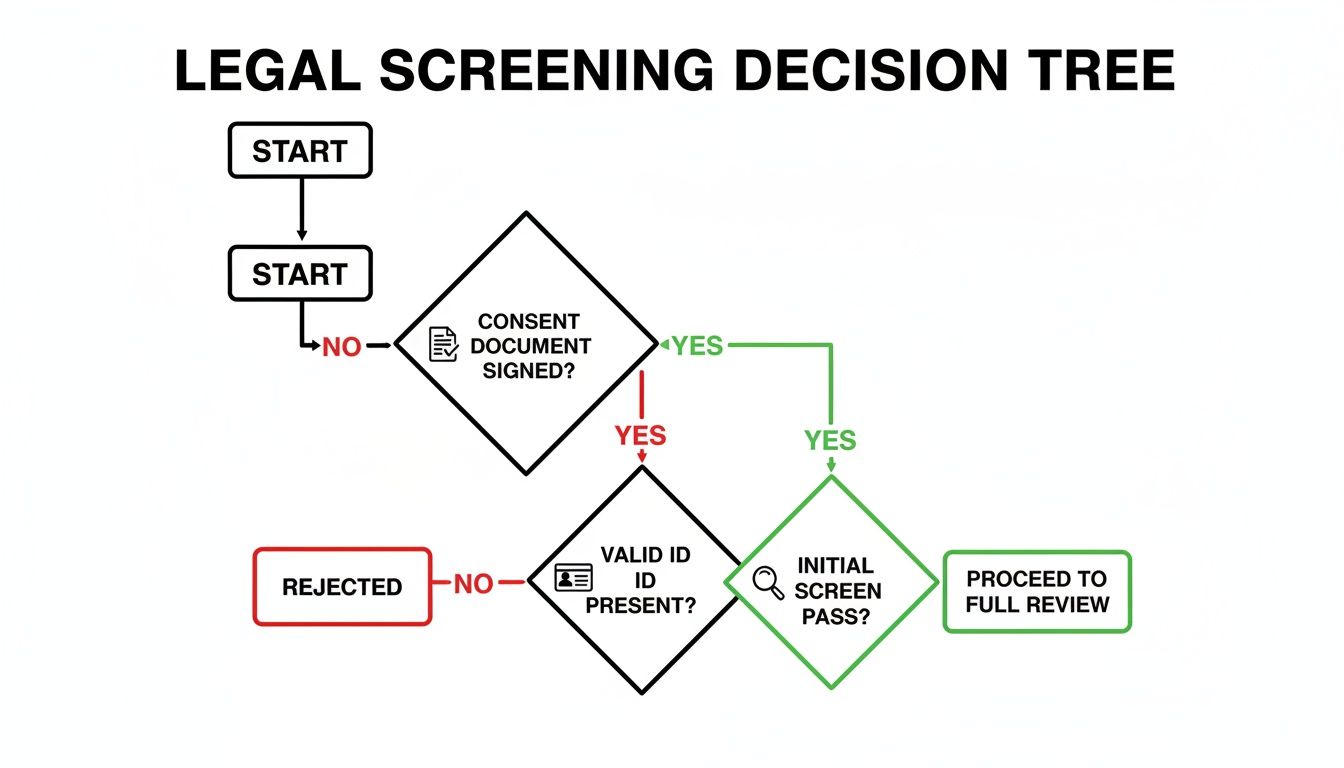

This simple decision tree lays out the legally-compliant path to a great tenant.

As the flowchart shows, it starts with getting permission, moves to verifying their identity, and finishes with a thorough screening. It’s a process that protects both you and the applicant.

Pro Tip: My favorite strategy is to use a service that has the applicant pay for their own screening report. This not only saves you money but also acts as a great filter. If someone isn't serious enough to pay a small fee, they probably aren't the right tenant for you. This one small tweak can save you a ton of time and weed out casual inquiries.

How to Read a Tenant Credit Report Like a Pro

The screening service has sent over the report. So, what’s next? A tenant credit report is so much more than just a three-digit number. Think of it as a financial story. Learning to read it properly is one of the most important skills you can develop as a landlord. It lets you see past a simple pass/fail score and really understand the applicant's financial habits.

Don't just glance at the score and call it a day. You have to dig into the details. A high score doesn't automatically mean you’ve found a great tenant, and a lower score doesn't always spell disaster. The real, valuable insights that protect your investment are hiding in the context of the full report.

Beyond the Score: Analyzing Payment History

This is it—arguably the most critical section for any landlord. The payment history reveals how consistently an applicant has paid their bills over time. A pattern of late payments is a huge red flag, even if they always seem to catch up eventually.

What you're looking for is consistency. Was there one late car payment two years ago? That’s probably not a deal-breaker. But if you see multiple 30-day or 60-day late payments across several accounts in the last year, that suggests a real problem with managing monthly bills. And rent is just another monthly bill.

Checking Credit Utilization and Debt Load

Credit utilization tells you how much of their available credit a person is using. It’s a powerful indicator of financial strain. If an applicant has maxed-out credit cards, they likely have very little wiggle room in their budget for an unexpected expense, which could put your rent payment in jeopardy.

This is a big deal. Utilization makes up about 30% of a credit score's weight. Anything over 30% is often considered a risk. In fact, a recent analysis showed a 12% jump in delinquency for renters with high credit card usage. While the global credit outlook notes some economic resilience, risks are still out there, making these checks vital. You can discover more insights about global credit metrics on Inside Housing. For less than 1% of the annual rent, routine screening can save you from a costly turnover.

Interpreting Collections and Public Records

This is where the most serious financial problems show up. Scroll down to look for any accounts in collections or public records like bankruptcies or civil judgments. When you see something here, pay close attention to the type of debt.

Medical Debt: I tend to view this more leniently. Medical issues can pop up out of nowhere and create a crisis for anyone.

Utility or Phone Bills: Unpaid utility bills are a different story. If they didn't pay their electric or water bill, they might not prioritize paying your rent, either.

Previous Landlord Debt: This is the ultimate deal-breaker for me and most other property managers. If they already owe money to another landlord, the risk of it happening again is just too high.

I once reviewed an application from someone with a decent credit score, but a closer look revealed an account in collections from a different property management company. This detail, which wasn’t obvious from the score alone, saved me from a likely eviction down the line. Verifying rental history is just as important as the credit check itself.

If you find something concerning, it's a good idea to cross-reference it with what you learned during the application process. For a deeper dive, check out our guide on how to verify rental history effectively.

Finally, take a look at recent credit inquiries. A flurry of applications in a short period could mean the applicant is about to take on a lot of new debt, which could easily impact their ability to pay rent. Reading a credit report is all about connecting these dots to see the complete financial picture. It ensures you make a decision based on solid evidence, not just a number.

Making the Final Decision and Communicating Professionally

Alright, you've done the deep dive into the credit report. Now comes the moment of truth: making a clear, confident decision. This is where your professionalism and by-the-book approach matter most. The key to keeping this whole process smooth and, most importantly, fair is to measure every single applicant against the exact same yardstick—your pre-defined rental criteria.

Think of your rental criteria as a written checklist. It's not just a nice-to-have; it's your single best defense against accusations of discrimination. By setting objective standards before you even start accepting applications—things like a minimum credit score, a specific income-to-rent ratio, and a clean eviction history—you take all the guesswork and personal bias out of the equation. Everyone is treated equally.

Approving the Applicant

If an applicant ticks all your boxes and their credit check lines up with your standards, that's great news! The next move is to formally offer them the lease.

Don't drag your feet on this. Extend the offer quickly and give them a clear deadline for signing the lease and paying the security deposit. A verbal "you're approved" means nothing until you have their signature on that lease agreement. Acting promptly shows you're serious and stops a great tenant from getting snapped up by another landlord.

Pro Tip: I always have a qualified backup applicant in mind. You just never know—even the most enthusiastic candidate can have a sudden change of plans. Keeping your second-choice applicant in the loop (letting them know they are next in line) can save you the headache of starting the entire screening process from scratch if your top pick falls through.

How to Decline an Applicant Gracefully and Legally

This is the part of the job nobody enjoys, but it’s a necessary one. If you have to deny an application because of something you found in their credit or background check, you have a legal obligation under the Fair Credit Reporting Act (FCRA). You must send them an adverse action notice.

This isn't just a quick "sorry" email. It's a formal communication that has to include some very specific information.

Your adverse action notice must contain:

The reason for the denial: You need to state clearly that the decision was based, at least in part, on information from their consumer report.

The screening company’s details: Include the name, address, and phone number of the credit reporting or tenant screening service you used.

A statement of their rights: You must inform the applicant that they have the right to dispute anything inaccurate in the report and can request a free copy from that agency within 60 days.

Getting this step right isn't optional. It's the law. For a complete rundown of this process, check out our guide on how to screen potential tenants the right way.

Secure Record-Keeping Is a Must

Once you've made your decision, your last task is to handle all the application paperwork securely. For the tenant you approve, their application, credit report, and background check become part of their official tenant file.

But what about the applicants you turn down? You can't just toss their information in the trash. You must either securely store or dispose of their sensitive personal data. That means shredding any paper documents and securely deleting digital files after a reasonable time. The standard is typically one to two years, but check your local regulations. This protects their privacy, minimizes your liability, and is the final, professional step in a well-run screening process.

Answering Your Top Questions About Tenant Credit Checks

Let's wrap up by tackling some of the most common questions I hear from landlords about checking a tenant's credit. Getting these details right is crucial for keeping your screening process smooth, legal, and effective. After all, making smart, informed decisions from the get-go is the foundation of a profitable rental business.

Even if you've been a landlord for years, new situations always pop up. Having solid answers to these questions helps you stay consistent and fair with every single applicant.

What’s a Good Credit Score for a Tenant?

This is the million-dollar question, and honestly, there's no single magic number. The "right" score really depends on your local market and the type of property you're renting out.

As a general rule of thumb, a FICO score of 670 or higher (on the 300-850 scale) is widely considered a good indicator of financial responsibility. It suggests a lower risk.

However, in a really competitive rental market or for a luxury property, you might see landlords looking for scores closer to 700 or even 740. On the flip side, in other areas, a score in the low-to-mid 600s might be perfectly fine, especially if the applicant has other strengths, like a high income or glowing references from previous landlords.

Can I Run a Credit Check Without a Social Security Number?

While an SSN is the gold standard for accurately pulling someone's credit file, it is technically possible to run a check without one. Some of the newer tenant screening platforms can try to locate a file using just the applicant's full name and address history.

But a word of caution: this approach is far more prone to error. You could easily pull the wrong report, especially if the applicant has a common name. For the most accurate and reliable results, you should always make collecting an SSN part of your standard procedure.

Key Takeaway: Before you even list your property, decide on your minimum credit score and put it in your written rental criteria. This simple step ensures you apply the same standard to every applicant, protecting you from potential discrimination claims.

Does a Tenant Credit Check Hurt Their Score?

This is a huge concern for applicants, and it's a great question. The answer depends entirely on how the check is performed.

When you use a modern tenant screening service (which is what I always recommend), the applicant is the one who initiates the request. This triggers a soft inquiry, which is completely invisible to lenders and has zero impact on their credit score.

If you were to go directly to a credit bureau yourself—a far more complicated and old-school process—it would likely result in a hard inquiry. These can cause a small, temporary dip in their score.

Letting applicants know that your process uses a "soft pull" can be a real plus, especially for those highly-qualified tenants who are protective of their excellent credit.

At Keshman Property Management, we meticulously handle every part of the screening process, from ensuring legal compliance to digging deep into the report analysis. With over 20 years of experience, we know how to protect your investment and find the reliable tenants you deserve. Discover more about our transparent, owner-focused services at https://mypropertymanaged.com.

Comments